Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaChina

13 Chapter Transfer Price Taxation

-

-

Fiscal year related intercompany transaction report

Companies engaged in transactions with related persons from the corporate income tax annual reporting deadline (May 31st) in fiscal year 2008 are included in the annual corporate income tax filing declaration form, which is the corporate income tax return, attached to the enterprise intercompany transaction report I needed it(Article 43 of the Corporate Income Tax Law, Article 11 of the Implementation Valve Act). Detailed information disclosure on transactions between companies and related parties to the tax authorities is required. This is equivalent to disclosure of the transaction price calculation method with overseas related persons in Appended Table 17 (3) "Detailed Statement of Foreign Affiliated Persons" in Japanese Income Tax Return Form.The items and necessary information are as follows.

■ Relationship table (Table 1)· Related party name· Taxpayer identification number· Country of origin (region)· Street address· Legal representative· Types of relationships (capital relationship, etc.)

■ Related Transaction Summary Table (Table 2)· Total transaction amount (aggregated by nature of transaction)· Amount and percentage of related party transactions· Amount and percentage of transactions among overseas related persons· Amount and ratio of transactions among domestic related parties· Presence or absence of a cost sharing contract· Whether preparation of simultaneous documents of transfer pricing is required (whether the document is prepared or not, if required)

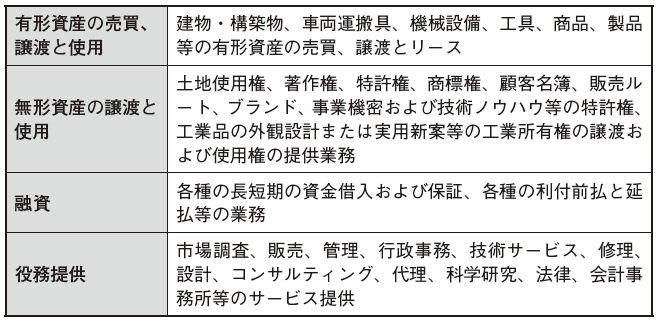

■ Purchasing and sales table (Table 3)· Purchase and sale from affiliates in Japan and overseas or third parties· Amount of related persons and non-related person transactions by trade method· Name of counterparty with overseas related persons and non-related persons when occupying 10% or more of total import / export total· The country of its location (region)· Transaction amount· Rationale for pricing

■ Service Table (Table 4)· Amount of service provided by affiliates in Japan and overseas or from third parties and expenditure· Revenues related to service provision and names of counterparties of overseas related persons and non-related persons, which account for 10% or more of expenditure amount· The country of its location (region)· Transaction amount· Rationale for pricing

■ Intangible asset table (Table 5)· Amount of transfer and amount transferred for intangible asset transactions (by type) with relevant parties and third parties in Japan and overseas

■ Fixed asset table (Table 6)· Transfer amount and transfer amount etc. of fixed asset transactions (by type) with relevant parties and third parties in Japan and overseas

■ Loan Funding Table (Table 7)· Ratio of credit investment (borrowing) and interest-earning investment (capital) acquired from finance-related persons with related persons in Japan and overseas· Name of affiliated people in Japan and overseas and their country of origin (region)· Currency· Interest rate· Loan term· Interest income expenditure· Name of guarantor· Guarantee fee and guarantee rate

The ratio of credit investment and equity investment acquired from this related person will be questioned from the viewpoint of under capital taxation. The tiny capital tax system is a tax system that prevents tax evasion by intentionally increasing the borrowing of related parties by generating interest payment.

■ Foreign investment situation table (Table 8)· Basic information of foreign company to be invested· Shareholding information· Income tax burden status of investee's foreign company· Status of dividends· Financial data· Whether the investee's foreign company is located in a non-low-tax country (region) enumerated by the State Taxation Bureau· Whether the annual profit of the investee's foreign company is less than 5 million Yuan

The information on the external investment situation table will be used to judge whether the investee's foreign company falls under the controlled foreign company.

■ External payment situation table (Table 9)· Payment amount to overseas related persons· Withholding collected income tax amount and tax concession benefit or not

Many of the above report tables are data that can be extracted from the day-to-day accounting practices, such as the counterparties and amounts of affiliate transactions.The purchase / sales table (Table 3) and the service table (Table 4) require filling in price policy to be applied for each important affiliate transaction, so the administrative burden for handling transfer pricing taxation is simply It will increase. It is necessary to ensure that there is no discrepancy between the Chinese side report and the Japanese side tax return for the same affiliate transaction. The check column for asking whether or not a simultaneous document relating to transfer pricing was created in the related transaction summary table in Table 2 is because it is necessary to prepare a tax return form and a simultaneous document (transfer pricing analysis material) according to the provisions It means. Contents of concurrent documents are widespread, and considerable administrative burden will increase as Table 3 and Table 4 of the report table.

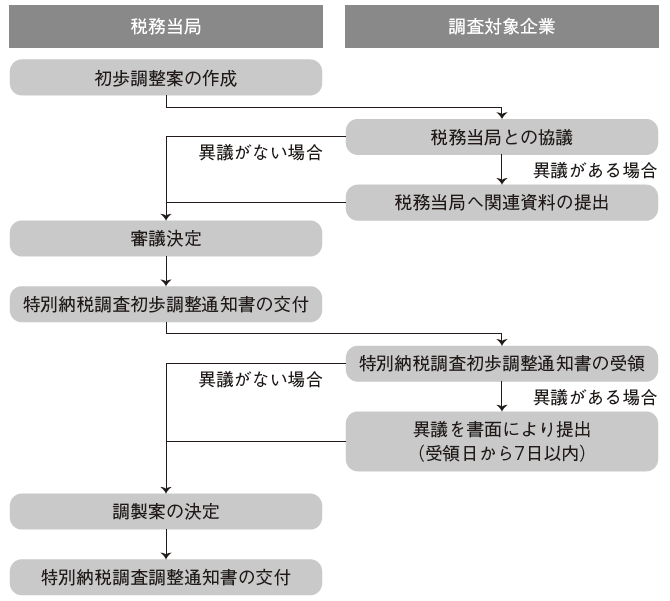

If you do not submit company-related intercompany transaction reports and concurrent documents to the tax authorities, direct penalties will only be a fine of not more than 10,000 RMB (Tax Collection Administration Act 60, 62). However, the risk above the penalty is the latent risk that companies not submitting related party transactions according to the provisions or companies not submitting concurrent documents will likely be selected for the transfer pricing survey. From another point of view, it can be said that problems in terms of internal control are revealed. -

Simultaneous document (transfer pricing analysis material)

■ Defining concurrent documents"Simultaneous" meaning simultaneous documents means to create a tax return form and transfer pricing document at the same time. However, although the company creates concurrent documents at the same time as the tax return, it is not required to submit both to the tax authorities at the same time. The transfer pricing document is to be submitted within 20 days after receiving the submission request from the tax authorities (Act on Investment Act 16).

The responsibility to prove the adequacy of pricing related to inter-related transactions in the transfer pricing survey is not on the relevant person but on the company side. Those that taxpayers (companies) create to fulfill their burden of responsibility will be concurrent documents.

However, companies falling under any of the following are exempted from the preparation of simultaneous documents (Article 15 of the same law).

· Annual purchase of related persons · Sales amount (calculated on the basis of import and export customs clearance price for material processing in terms of material processing) is less than 200 million RMB and other inter-related transaction amount (inter-related loan transaction is received and Calculated based on the amount of interest payment) is less than 40 million RMB (40 million RMB does not include the amount of related party transactions related to cost sharing or prior confirmation by companies within the year)· When related party transactions are subject to prior confirmation· When foreign ownership interest is less than 50% and only related persons in China are involved in transactions between related parties

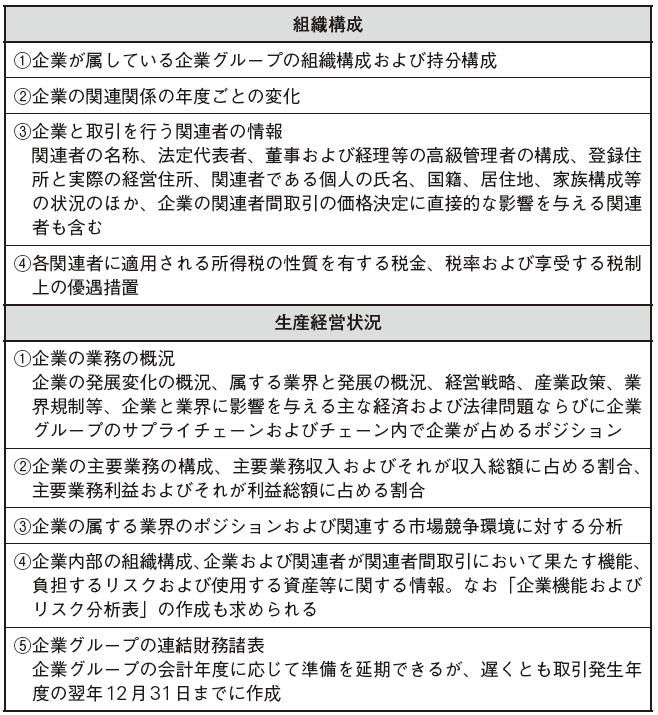

■ Contents of concurrent documentsCompanies must prepare concurrent documents relating to inter-related transactions for each tax year and submit it as requested by the tax authorities (Implementation Valve Act 13). Contents of simultaneous documents consist of 5 major items and 26 small items (Article 14 of the same law). In order not to point out deficiencies, in principle it is desirable to list all the following items.

If companies are to undergo a transfer pricing survey, they will develop discussions with tax authorities on the basis of concurrent documents (transfer pricing analysis data). Therefore, simultaneous documents share the contents of related business transactions described in the simultaneous document between the company and the tax authorities, which has the effect of greatly reducing the time and cost required to recognize the facts prior to the discussion development. Companies should therefore create concurrent documents with recognition of the first step of the transfer pricing survey. However, it is not practical from the viewpoint of cost and quality to prepare concurrent documents within a company because the content of the concurrent documents required by the Investment Law Act is broad and the special analysis is required . From the present situation like this, in practice, there are many cases where external experts specializing in transfer pricing analysis, such as searching for comparative companies / transactions and benchmarking analysis, are asked.

■ Other points to keep in mindPoints to keep in mind about the creation, storage and submission of concurrent documents prescribed by the Implementation Valve Act are as follows (Article 17 to 20 of the Implementation Valve Act).

· A simultaneous document to be submitted pursuant to the request of the taxing authority shall be affixed with a seal and a signatory or seal must be signed by a legal representative or a representative authorized by a legal representative· When quoting information in the creation of simultaneous documents, the source must be specified· When a company changes or deletes a tax registration due to merger, division, etc., companies after merger / division must preserve simultaneous documents· Chinese are used for simultaneous documents, and Chinese copies must be attached when the source material is a foreign language· Simultaneous documents must be kept for 10 years from June 1st the following year of the year when the enterprise related party transaction occurred

-