Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaChina

11 Chapter Tax law

-

-

1 Chapter Introduction

1.1 The history of Japanese companies entering the world

1.2 New business model in China

1.3 Advance scheme through Hong Kong

2 Chapter Basic knowledge

3 Chapter Investment Environment

3.2 Province and region of China

3.5 Investment incentives and regulations

4 Chapter Economic Environment

5 Chapter Establishment

5.3 Establishment of business base

5.4 Procedure after incorporation

6 Chapter Withdraw

7 Chapter Foreign exchange

7.1 Foreign exchange management system in China

7.2 Foreign currency management system of ordinary items

7.3 Foreign exchange control system of capital items

7.4 Foreign exchange control system in bonded area · Hong Kong

7.5 Individual foreign currency control system

8 Chapter M&A

8.2 Laws and regulations concerning M & A

8.5 Challenges after corporate acquisition

9 Chapter Corporate Laws

10 Chapter Accounting

11 Chapter Tax law

11.2 Representative Office Taxation

11.4 Individual Issues in China Domestic Tax Law

12 Chapter International taxation strategy

12.1 International tax relating to entering China

12.2 International taxation strategy

12.3 Individual Issues in International Taxation

12.4 Tax issues related to withdrawal

13 Chapter Transfer Price Taxation

13.2 Individual provision pertaining to transfer pricing taxation

13.3 Transfer price taxation and documentation

13.4 Transfer price survey in China

14 Chapter Labor

14.4 Points to remember when bringing Japanese

15 Chapter International Human Resources Management

15.1 Human Resources Labor Management

15.3 Personnel evaluation system

-

-

-

Latest News & Updates

* Reform of single value increase tax of business tax in China

In case

According to the financial tax [2016] No. 36 (36th issue) jointly issued by the Ministry of Finance and the State Administration of Taxation, from May 1, 2016, the business tax completely shifted to the VAT. Based on the 36th issue, all service provision including construction, real estate, financial services and living services are subject to tax on value added tax as well as goods sale, taxpayers are deducted from purchase taxes It will become available.

The real estate industry, building industry, financial services industry and living service industry are trial ranges, and the change in the tax rate due to reform of sales tax single value increase tax is as follows.

1. Real estate industry and building industry

Because the definition of building industry and real estate industry generally coincides with the provision of business tax, the value added tax is applied to the work at the stage of construction, sale, leasing etc. of real estate.

2. Financial services industry

According to the provisions of issue No. 36, financial services refer to business activities dealing with finance and insurance, including loan services and financial services, insurance services, and transfer of financial products. It is necessary to note that the definition of financial services will be updated in accordance with the deployment situation in practice.

3. Lifestyle services

Lifestyle services in the 36th sentence refers to various service activities provided to satisfy the daily living needs of urban residents and includes cultural physical education services and educational medical services, travel entertainment services, food and drink accommodation services, residence Includes people's daily service.

Details will be updated soon.

-

Taxation in China

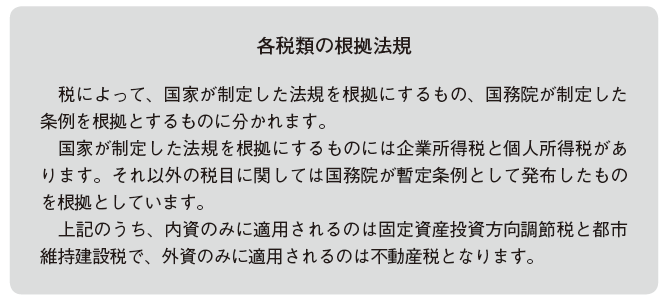

History of tax lawSince the opening-up policy in the 1980s, China classified internal and internal capital taxes for each tax item and categorized it into the internal taxation system for Chinese companies and Chinese and foreign taxation system for foreign-owned companies and foreigners. However, due to the revision of the Chinese tax system in 1994, the integration of the differentiated taxation system was aimed at, and the basic skeleton of the present Chinese tax system was formed. As a big change in the tax system after that, the People 's Republic of China' s corporate income tax law was enacted in 2007, and the personal income tax law was revised. In addition, in 2008 the revision of the Personal Income Tax Law Implementation Ordinance was made. Furthermore, in 2016, the value added tax (incremental tax and business tax), which was divided into two according to the transaction contents, was unified into incremental taxes. The main purpose of these changes in the Chinese tax system is as follows.

· Resolution of income tax burden disparity problem among domestic and foreign companies· Unification of tax burden between Chinese and foreigners (for individuals residing in China)· Appropriate allocation of resources by market function, enhancement of central government's control and management function by correcting system gaps

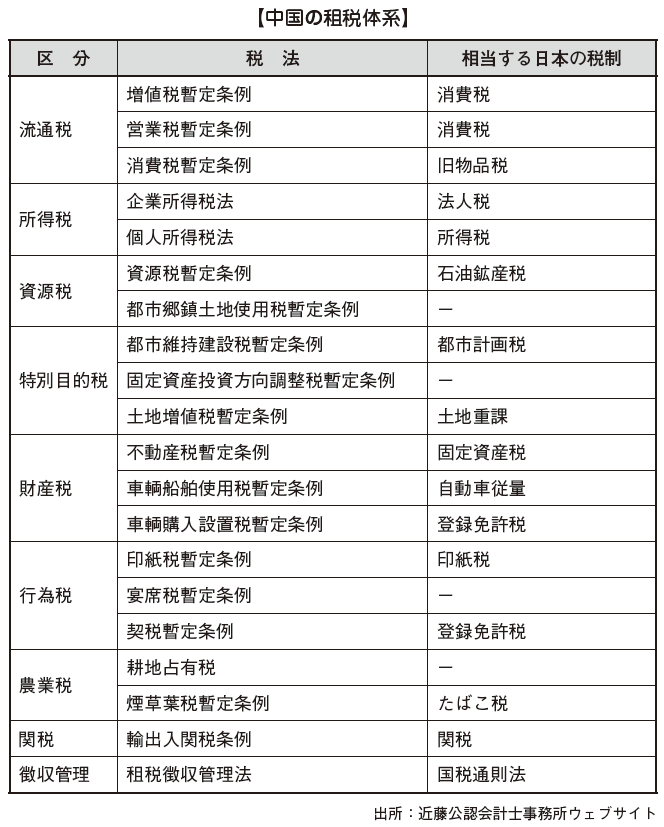

■ Tax System The taxation of China can be categorized mainly into eight categories: distribution tax, income tax, resource tax, special purpose tax, property tax, act tax, agricultural tax, and customs duty.

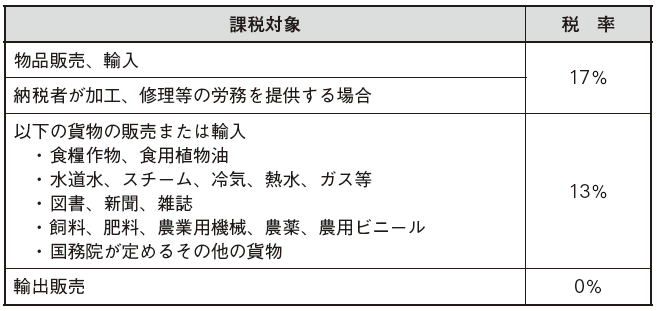

[Distribution tax type]Distribution taxes are taxes including value-added tax, business tax, and consumption tax. VAT is a tax applicable to Japanese consumption tax. It is necessary to pay attention to the provision of Japanese consumption tax service because the subject of taxation is different. Consumption tax in China is different from Japanese consumption tax, and luxury goods (luxury goods), luxury goods are subject to taxation. Distribution tax including these value tax, business tax, consumption tax accounts for about 50% of the tax revenue in China.VAT reformAs a Japanese consumption tax, there have been upsell taxes and business taxes in China so far. Basically, the Value Added Tax is subject to tax only for the sale of goods, and the business tax was for the provision of services. In addition, there was a systematic difference in that it was not possible to deduct purchase by business tax, while the value added tax could deduct purchase increment tax from sales increment tax. As a result, the problem of double taxation has occurred, and tax system reform was being promoted to solve the problem. This reform began pilotly in some areas from January 2012 and on May 1, 2016 transactions that were subject to business taxation throughout China have become subject to value taxation . The value-added tax rate is also being developed, and the value-added tax rate table is as follows.

【Latest value added tax rate table after incremental tax reform】【増値税改革後の最新増値税税率表】Taxpayer classification

Taxable activities

Specific taxable activity

VAT rate

Remarks

Small taxpayer

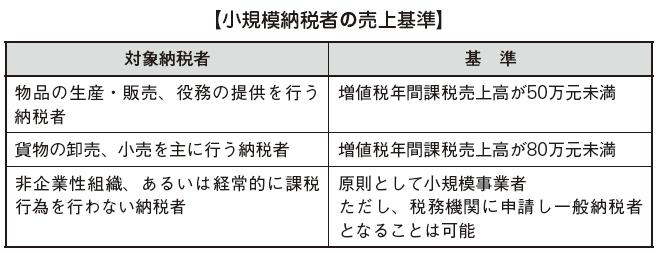

Goods sales, processing, repair, various labor services etc.

3%

No purchase deduction

General taxpayer

Goods sale / import cargo (excluding those specified below), processing, repair services, etc.

17%

1. Cereals, vegetable oils, milk.

13%

2. Tap water, heating, cooling, hot water, gas, liquefied petroleum gas, natural gas, biogas, household coal products.

3. Books, newspapers, magazines.

4. Feed, fertilizer, pesticide, agricultural machine (machine), agricultural film

5. Other cargo regulated by the State Council

6. Agricultural products (various animals, plants), music video products, electronic publications, dimethyl ether, salt

Export cargo

0%

General taxpayer after incremental tax reform

Sales service

Transportation and transportation services

Land Transport Service

Railway transport service

11%

Other land transportation services

Waterway transportation service

A cruise ship

Voyage Charter. Primarily a ship that carriers (shippers / shipping operators etc.) negotiate freight rates and other conditions with shipowners for one voyage or number of voyages between two specific ports.

Regular ship

Time Charter. A ship that the ship operator prescribes a specific period such as 6 months, 1 year in advance

Airport Transportation Service

Wet lease of air transport

Pipeline transportation service

Freight forwarder business

Transportation equipment / transportation service without transportation → refers to a supplier who does not have a means of transportation and entrusts cargo to another air carrier. (Confirmation required)

Postal service

Postal service ordinary service

letter

11%

parcel

Postal special service

Postal special service

Other postal service

Other postal services, sales of postage stamps etc, postal services such as postal representation.

Telegraph service

Basic Telecommunication Service

Basic Telecommunication Service

11%

Value added telegraph service

Value added telegraph service

6%

Building service

engineering service

engineering service

11%

Installation service

Installation service

Repair service

Repair service

Decoration service

Decoration service Other construction services

Other construction services

Financial services

Loan service

Loan

6%

Sale and lease back finance

Direct income financial services

Direct income financial services Insurance service

Personal insurance service

Property insurance service

Transfer of financial instruments

Transfer of financial instruments

Transfer of other financial products

Modern service

R & D and technical services

Research and development services

6%

Joint resource management service※

※In English, EPC - Energy Performance Contracting. Refers to a business model in which an energy-saving business operator collects from the owner an amount corresponding to the expenses incurred by energy conservation business operators on behalf of the owner instead of the owner of the owner and the expenses that can be reduced by energy conservation during a certain period of time .

Engineering survey and exploration service

Professional technical service

Information technology services

Software service

6%

Circuit design and test service

Information system service

Business process management service

Information system value added service

Culture creative service

Design service

6%

Intellectual property services

Advertisement service

Conference Exhibition Service

Logistics assistance clothing

Aviation service

Airborne ground service

6%

General aviation services

Port and Pier service

Freight passenger terminal service

Rescue service

Loading and unloading transport service

Goods receipt service

Collection and delivery service

Receiving service

Separation service

Delivery service

Lease service

Finance lease service

Finance lease service of tangible movables

17%

Real Estate Finance Leasing Service

11%

Operating lease service

Tangible movable property operating lease service

17%

Real estate operating lease service

11%

Warranty consulting service

Authentication service

6%

Verification 咨 idence Clothing → Warranty Guarantee service

Consulting Services

Radio and TV service

Radio / TV service program (work) production work

6%

Radio / TV service program (work) distribution service

Radio / TV service program (work) broadcasting service

Business assistance business

Corporate management service

6%

Business agency service

Cargo Transport Agency Service

Proxy Customs Clearance Service

Personnel service

Security service

Other modern services

Other modern services

6%

Living service

Culture & Sports Service

Cultural services

6%

Physical education service

Educational medical service

Education service

Medical service

Tourism · entertainment service

Tourist services

Entertainment service

Restaurant · Accommodation service

Restaurant service

Accommodation service

Resident's daily service

Other living services

Intangible fixed asset sale and purchase

Technology

Professional technical service

6%

Non-technical service

trademark

Copyright

Goodwill

Other profitability Intangible assets

Natural resource use right

Sea area usage right, exploration rights and digging rights, water rights, other right to use natural resources

Land use right

11%

Real estate buying and selling

Building

11%

Construct

* Supplemental Note: The tax rate on partial real estate sales and leasing is 5%. The tax rate for specific acts of other small taxpayers and general taxpayers is 3%.[Income Tax Type]Income taxes are taxes including corporate income tax and personal income tax. The income of companies and individuals is subject to taxation. Corporate income tax is Japanese corporate tax, and personal income tax is tax equivalent to income tax in Japan. Income taxes are said to account for about 2.5% of the tax revenue of the Chinese government.[Resource tax type]Resource taxes are taxes including resource tax, city town hometown use tax.[Special purpose tax class]Specific purpose tax classes are taxes including urban maintenance construction tax, arable land occupancy tax, fixed asset investment direction adjustment tax (domestic companies only, not for foreign-owned enterprises), land increment tax.

[Property Tax Type]Property taxes are taxes including real estate tax, vehicle ship use tax, vehicle purchase installation tax, etc. Acquisition or possession of property etc. is subject to taxation.

[Act taxes]Act taxes are taxes that include stamp duties, taxes, etc.

[Agricultural taxes] Agricultural taxes are taxes including tobacco leaf tax. Tobacco leaf tax subjects tobacco purchase taxation. It corresponds to tobacco tax in Japan.

[Customs duty]Tariffs are taxes that include import and export duties. We import and export goods when importing and exporting are subject to taxation. It is equivalent to Japan's customs duty.

■ National tax, local tax, common taxPrior to 1993, we adopted a method of collecting national taxes and local taxes at the local tax bureau, but due to the revision of the Chinese tax system in 1994, various taxes are classified as national tax, local tax, common tax, classification of collecting agencies The national tax is the national tax bureau, the local tax is the local tax bureau, the common tax is to be collected at both stations (consumption tax collected with customs duties, VAT is collected by customs). Before introducing the tax system, more than half of tax revenue was distributed to local governments. However, with the change of the tax collection type due to the major amendment, the National Taxation Bureau was newly established in each region, and the central government was able to collect taxes directly. As a result, the tax revenue directly collected by the central government is about 60%, the local government's tax revenue is about 40%, and more than half of tax revenue has been distributed to the central government.The biggest revision of the tax system reform in 1994 is to correct disparities and strengthen control and control.

【Tax classification and tax items in China】Tax classification

Tax item

National tax

Tariff

Consumption tax and value-added tax collected by customs

consumption tax

Regional bank, foreign capital bank, non-back corporate income tax

Revenue intensively paid by the railway department, each bank head office, each insurance company, etc.

(Including business tax, income tax, profit and urban maintenance construction tax)

Local tax

personal income tax

Urban maintenance construction tax

Fixed asset investment direction adjustment tax

Urban Land Use Tax

Land Building Property Tax

personal income tax

Vehicle ship usage tax

Stamp duty

Taxation tax

Land Value Increase Tax

Tobacco leaf tax

Arable occupancy tax

Common tax

Increase value tax (75% in the country, 25% in the region)

Resource tax (allocated according to resource type, most resource tax is local

Revenue, marine oil resource tax will be the central income)

Corporate income tax

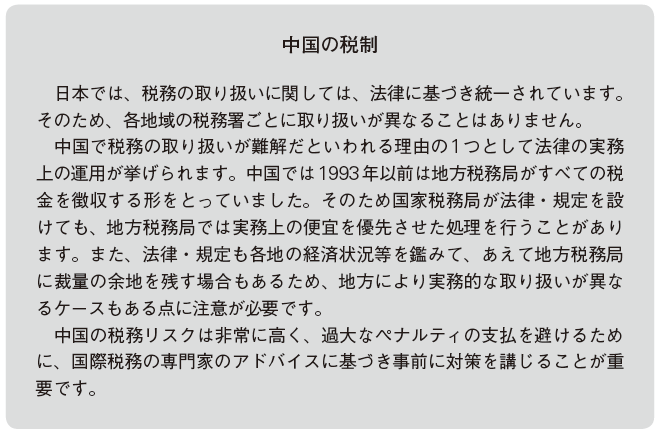

In China, tax collection was done mainly by local governments. Therefore, local governments do not take a collecting method based on the nationwide unified tax policy and tax interpretation, and the actual situation is that tax collection is done by the tax collection method that gives priority to the circumstances of each local government. Currently, there are the National Taxation Bureau and the Local Taxation Bureau in all regions, and in principle the national tax is to be collected by the National Taxation Bureau and the local tax is to be collected by the local tax bureau (foreign enterprises, corporate income tax is to the State tax office, personal income tax and business tax About taxation to the local tax bureau).

■ Direct tax and indirect tax"Direct tax" refers to the tax that "taxpayers" that pay taxes are the same as those who actually pay taxes. Income tax (corporate income tax, personal income tax) applies to China's direct tax. In addition, customs duties, fixed asset investment direction adjustment tax, etc. are also applicable.Indirect tax, on the other hand, unlike direct tax, refers to different taxes for those who pay and those who actually pay. Distribution taxes (incremental taxes, consumption taxes) are the main indirect taxes in China. This distribution tax accounts for about 50% of the tax revenue in China.【China Tax Revenue Ratio】Classification

Tax classification

Tax item

Tax revenue (%)

Indirect tax

Distribution tax

Domestic Value Added Tax

28

58

VAT

17

Domestic consumption tax

8

Import and export cargo value increase tax, international consumption tax

5

Direct tax

Income tax

Corporate income tax

21

27

personal income tax

6

Special purpose taxes

Urban maintenance construction tax

2

7

Arable occupancy tax

2

Land Value Increase Tax

3

Act tax

Taxation tax

3

6

Tariff

3

Other taxes

2

2

total

100

100

-

Characteristics of tax

The Chinese tax system has the following characteristics.

· All corporations are settled in December· Monthly tax return, monthly closing (foreign currency conversion, etc.)· Monthly personal income tax return· The deduction for personal income tax is based on basic deduction only· The presence or absence of votes (receipts) is important (because tax processing can not be done without a vote)

There is a unique tax risk in China as one of the major characteristics of the Chinese tax system. Below, I will describe the tax risk which should be noted in doing business in China.

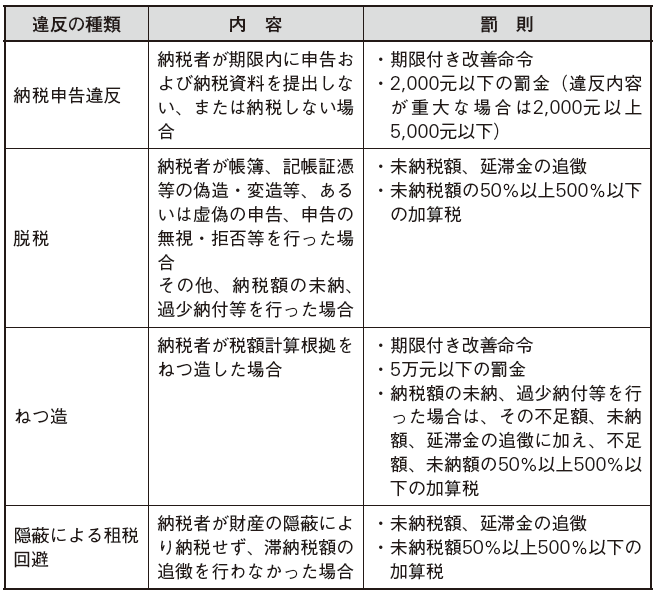

■ Penal ProvisionsEven in China, taxpayers must file declarations based on the contents of the truth within the time limit. If you do not submit a declaration within the deadline, or if you make a false declaration by overworking, concealment, etc., the following penalties will be imposed.

Currently, the additional tax is 50% or more and 500% or less, and the delinquent tax is 18.25% (0.05% per day). However, the overdue tax on violation before April 30, 2001 is 0.2% per day (73% per annum). Please note that the amount of money is considerably larger than in Japan.

■Responsibility for burdenIn Japan, tax refunds will bear the responsibility for the evidence while the reason for the revision is attached to the notice when the correction is required by the tax return. On the other hand, taxpayers assume the burden of proof in China. In other words, taxpayers themselves must prove their validity. Proof material is necessary for proof of validity. For example, based on oral guidance from the tax authorities, despite the fact that the tax treatment was revised, it was found later that the processing was wrong, and as a result of force majeure himself was unable to submit the correct evidence material Even you may be forced to pay a fine. Also, due to mistakes in recognition of predecessors of tax authorities, even if an error is found along with changes in personnel, there are cases where a fine is imposed.

■ Encouragement of accusationsThe Chinese government has established a system that encourages accusations against illegal acts and gives incentives to whistle-blowers to prevent illegal acts related to tax (encouraging taxpayers to accuse taxpayers illegal acts) Temporary method, National Taxation Bureau, Ministry of Finance Ordinance [2007] No. 18).Under this provision, the amount of reward will change according to the amount collected, but a maximum of 100,000 RMB or less will be paid. For counterfeiting, alteration, etc. for exclusive value tax etc., the reward will be changed depending on the number of copies of counterfeit issuance, and this will also be paid a maximum of 100,000 yuan or less.

-

-

-

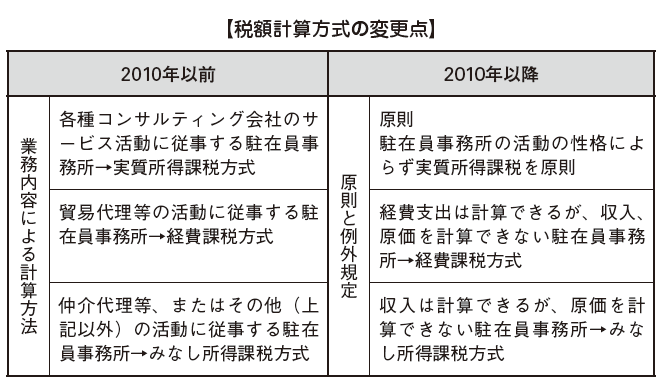

Representative Office Taxation

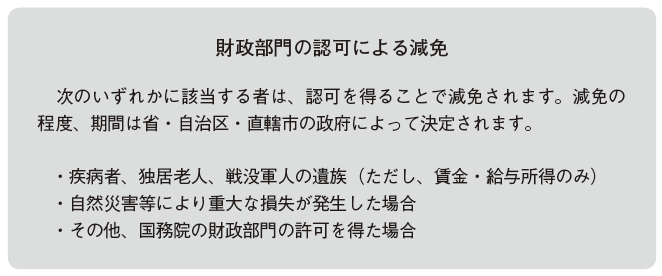

Taxation of a representative office means to treat certain expatriate office activities as being in business in China, accounting for taxation, imposing corporate income tax and business tax . The purpose of establishing a representative office in China is to conduct ancillary / preparatory work for contacting or investing in the headquarters. Since it is said that it is not possible to conduct direct sales activities in principle, income as a business does not occur as a rule and therefore it is considered not to be subject to taxation. In addition, the activities conducted by these representative offices under the Japan-China Treaty fall under the exclusion requirement of "permanent establishment", which is not taxable.Therefore, the taxation of the representative office so far has been (1) after opening the representative office, apply for tax exemption, approve the tax authorities and adopt a method to make declaration unnecessary, or (2) take a declaration method by income taxation In principle, the method of exempting taxation (the business income targeted for taxation becomes zero in principle = the representative office does not conduct direct sales activities in principle) was taken.Prior to 2005, due to reasons such as restrictions on the establishment of subsidiaries and branches, the representative office was carrying out semi-marketing activities similar to branches, in addition to the original activities. In this case, you are deemed to have earned profits from semi-sales activities and taxed. In order to clarify the judgment criteria for the tax relations of the representative office, the Chinese tax office promulgated a provisional regulation on tax collection and management of the representative office of a foreign company on February 20, 2010, Management, taxation method, revision of estimated profit margin, etc. This provision is to be retroacted until January 1, 2010. Currently, in practice, most representative offices are subject to taxation.

The problem in considering the representative office taxation is that treatment will change depending on whether or not it is certified as a permanent establishment (PE). In principle, the representative office is taxed on its income, but it applies to the tax bureau to the effect that it is not a permanent facility prescribed in the Japan-China Dial Treaty. (See the item "Taxpayer"). There are clarification criteria for supplementary and preparatory work as a change by provisional regulations concerning tax collection and management of a representative office of a foreign company. The contents are as follows.

· If the target of the activities of the representative office is a third party, it is subject to taxation because it is not supplementary · preparatory work.· When the activities of the representative office are the same as those of the head office, they are subject to taxation because they are not supplementary or preparatory work· When the activities of the representative office are important elements of the head office work, they are subject to taxation as they are not supplementary or preparatory work

Based on the above, after submitting the relevant certificate to the tax authorities, the tax authorities will apply for tax exemption after judging.

Also, tax calculation method has changed. Traditionally, methods of tax calculation were prescribed according to the content of business, respectively, but in principle the real income taxation method is to be applied based on this ordinance (refer to the item "Calculation method") .

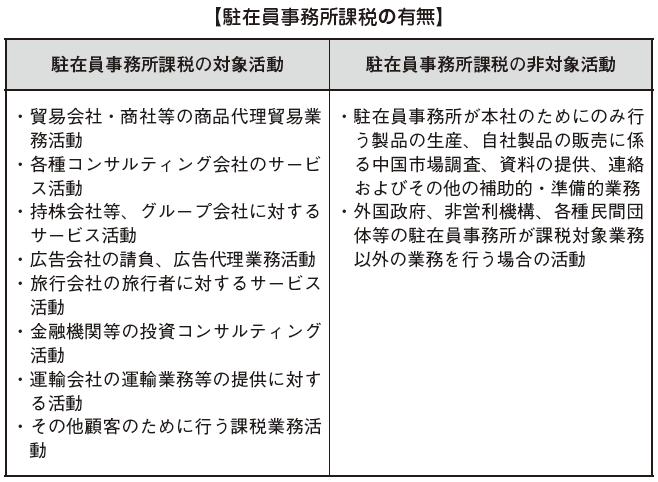

■ Taxable activitiesThe purpose of establishing a representative office in China is basically to store goods for the headquarters, gather information, and do other secondary or preparatory character work. Therefore, although it should not be subject to taxation, the tax authorities will pay attention to the work of the substantial representative office and judge whether it is subject to taxation. Targeted activities of taxation and non-target activities of taxation are as follows.

■ Calculation method[Real Income Taxation System]It is a method to calculate taxable income by deducting office expenses etc. from income. Based on the calculated taxable income, business tax and corporate income tax are imposed. The real income tax method is a principle calculation method after 2010 and it is necessary to calculate taxable income based on this method. In order to apply this method, the representative office must prepare the exact book and prepare it, but it may be that it has not been created in practice. Therefore, in exceptional cases, it may be calculated by the following two methods.

[Expense taxation method]It is an exceptional way to calculate deemed income from expense expenses and calculate taxable income by adding a certain percentage adjustment to its deemed income. Based on the calculated taxable income, business tax and corporate income tax are imposed.Even though expense expenditure can be accurately calculated, this method is applied when revenue and cost can not be accurately calculated.

[Deemed income taxation method]Business taxRevenue amount = current expenditure expenditure ÷ (1 - deemed profit ratio - business tax rate) Business tax amount = revenue amount × operating tax amount

Corporate income taxTaxable income amount = income amount × deemed profit rate enterprise income tax amount = taxable income amount amount × corporate income tax rate

The deemed purchase rate will change according to the actual situation of the company, but it is said that it can not be less than 15%, and in practice it is often 15%. Prior to the 2010 regulation system, the deemed purchase rate was 10%, but since then it is 15%, so be careful.Also, if the annual conversion revenue does not exceed 5 million yuan, the expatriate office treats it as a small taxpayer, so the value-added tax rate will be 3%. On the other hand, if it exceeds 5 million RMB, it will be treated as a general taxpayer, so the value-added tax rate will be 6%. Since there are cases where handling differs depending on the region, we recommend that you check with the tax department separately.

-

-

-

Permanent establishment

Permanent Establishment (PE) is a fixed place where foreign companies established in China, doing business. It is said that PE includes management place of business, branch office, office, factory etc. A facility etc. that has a function to conduct a business, established by a foreign company in China. Treatment of taxation relations will differ depending on whether a foreign company has some sort of base in China depending on whether it falls under PE or not. -

Taxpayer

Whether or not it falls under PE taxation obligations is determined by whether the facility is PE or not. According to the Japan - China Tax Convention, even a facility that has a function to do business in China may not fall under PE in the following cases.

· When using the facility only for storage, exhibition, delivery of goods, etc.· When stocks of goods, etc. are held only for storage, exhibition, delivery· When stocks of goods etc. are held only for processing by another company (other than the owner of the facility)· To hold business only for the purpose of purchasing goods etc. or collecting information only· Other supplementary · When holding for business only for the purpose of conducting preparatory work

In the case of a facility that exclusively carries out goods storage for the head office, information gathering, and other auxiliary or preparatory character work, it does not fall under PE. However, whether or not it falls under PE will be submitted to the tax authorities and judged by the tax authorities. In that case, materials will be submitted to each region and each tax office, but care must be exercised as PE interpretation criteria are different in each case.

■ Practical problems concerning PE judgmentIt is hard to think in Japan, but not only in each region but also between the National Taxation Bureau and the Regional Taxation Bureau in China, handling on taxation may be different (PE's decision is the same).One of the reasons why this happens is the structure of tax authorities in China. In China there are two mechanisms, the National Taxation Bureau and the Local Taxation Bureau, but these are not in an up and down relationship and there is no obligation to exchange information. Therefore, depending on the tax treatment at the local tax bureaus, the National Taxation Bureau will not decide on tax treatment but decide based on their own judgment. Therefore, because the two tax bureaus are not cooperating, inconsistent tax treatment will be done.Whether companies are certified as PEs or not will have a significant tax impact on companies, so it is important to consult with experts in advance in order to avoid unforeseen circumstances and take appropriate countermeasures . -

Taxation relationship

If PE is not accredited, business tax will be levied but corporate income tax will not be taxed. Even for personal income taxes, tax is not imposed if it applies to short-term residents tax exemption provisions.In addition to business tax imposed not by PE, it is not only imposing business tax, but also income in China and income attributable to PE out of income outside China are also subject to corporate income tax I will be taxed. In regard to personal income tax, short-term residents tax exemption provision is not applied and tax is imposed on income paid from PE according to the number of working days in China.In this way, tax approval will increase if PE is certified, and the total tax payment also increases, which is a burden for companies.【Difference in taxation by PE certification】When it does not correspond to PE

In case of PE

・ Value increase tax

・ Personal income tax when short-term residents tax exemption provision is not applied

Taxable

・Value increase tax

· Income in China, enterprise income tax on income attributable to PE out of China's foreign income

· Personal income tax on income from PE

Taxable

· Corporate income tax

No tax

■ Short-term residents tax exemption provision The provision that short-term residents exempt tax provisions are exempted from personal income tax payment obligations for residents who meet certain requirements under the Japan-China Tax Treaty. There are three requirements as below, and it is necessary to satisfy all.

Staying days are less than 6 months (183 days)For staying days, it is necessary that the period of stay in China in calendar year (January 1 to December 31) is 183 days or less. Even if it crosses the year and exceeds six months, if it does not exceed 183 days in the calendar year, it will be regarded as staying less than 6 months.

Remuneration paid by nonresidentRemuneration paid to China residents is required to be paid by non resident (non-resident) in China.

It is a non-burden of PERemuneration paid to Chinese residents is required not due to PE's burden. -

Points on practical PE certification

■ Dispatch of 6 months (183 days) or lessIn the opinion on the handling of some problems concerning the implementation of the medium- and medium-term tax treaties established by the Ministry of Finance and the State Taxation Bureau in 1985, the period of activities for supervision and consultant service provision is as follows.

Supervision activityBased on whether or not the period from the date on which the first personnel started work on the construction site to the date of completion of the handover exceeds six months and whether or not it is PE or not for the construction project . Even when crossing the year, this period is judged in six months (even for projects from October 1 to May 31 of the following year, it is judged to be a project of 6 months or more.) October 1 - December 31, 1 January - 31 May not be divided).The point to be noticed in practice is not whether the dispatched worker's stay in China is less than 6 months or not, but to judge whether or not the service contract is over 6 months in total. If it falls under the supervision activity, it is judged by the construction project, not considering the requirement of the six-month standard of the short-term stay exemption provision.When multiple work is performed by the same construction project, it is judged by not considering the work for each work, and considering the plural work as one construction project.

Consultant service offeringRegarding service provision of consultants, judgment is made not based on the staying time of the dispatched person, but based on whether the service provision contract exceeds six months or not. Just like overseer activities, the period is judged in six months even if it crosses the year. As a matter of practical consideration, even if the dispatch period of the dispatched person is 6 months or less, there are facilities in China, where the business is conducted (manufactured in China, for the guidance of its production Etc.), the facility itself may be PE. In other words, if Japan buys a product manufactured at the facility and sells it in Japan and makes profit, it is regarded as a business and considered to be PE.

Disadvantages of PE certificationIf approved by PE, you will pay corporate income tax in China, but you can apply foreign tax credit in Japan for that amount. That is the difference between paying taxes in China or paying taxes in Japan and it seems like there are not much disadvantages.However, there is a point that personal income tax is additionally imposed by becoming certified by PE, there is a deductible limit in foreign tax credit (In some companies, corporate income tax paid in China can not be deducted in Japan) As for the Chinese tax system, many tax reforms (major revision of value added tax etc. in 2011) are being carried out in recent years, so it is necessary to pay attention to the point that it is difficult to predict tax risk.

-

-

-

Latest News & Updates

* Tax system of transboundary EC

In case

With regard to transboundary EC, from April 8, 2016, it changed significantly from the existing system.

The Ministry of Finance, the Customs General Administration, and the National Taxation Bureau issued "Notice on Tax Revenue Policy on Transboundary Electronic Commercial Retail" on 24th March 2016 (hereinafter referred to as "Notice"). Furthermore, "cross-border e-commerce retail import product list" (hereinafter referred to as "list") was promulgated on April 6. By "notification" and "list", a new tax revenue policy on transboundary e-commerce retailing in China has been established. It will be applied from April 8, 2016.

According to the new tax revenue policy, it is as follows.

1) 1142 items were listed, and the negative list which was applied conventionally was abolished. The gray zone due to the negative list management disappeared, and importable commodity items and tax codes were clarified.

2) As the tax type changes, the "row tax" applied so far will be abolished, customs duty, value added tax, consumption tax will be imposed.

3) Regarding transaction amount regulation, one transaction is within 2,000 RMB, and annual amount is 20,000 RMB or less.

4) With regard to tax burden, tariffs are exempted from those within the amount regulation range, and the incremental tax and consumption tax are 70% of the statutory tax rate. The impact of the tax system revision will be different for each product type.

The table below summarizes the differences between the old system and the new system.

Amendment item

Before revision

After amendment

Remarks

Remarks

1,000 RMB / per purchase

2,000 RMB / per purchase

Beyond the purchase limit, it is treated as general trade, and the customs duty, the value added tax, the consumption tax will be applied as it is (before the revision: no row wage applicable, after the revision: tax rate 30% not reduced).

In addition, "20,000 RMB / person per year purchase" has not changed.

Row waiver

10 to 50%

Abolition

Tariff

duty free

Below the purchase limit, 0%.

If it exceeds the maximum amount,

Apply the same rate as general trade.。

Tax exemption up to tariff amount of 50 yuan is also abolished.

Import VAT

duty free

Applied to all at a tax rate of 30% reduction.

For example, if the import incremental tax rate is 17%, the increment tax 11.9% (= 17% x 70%)

consumption tax

duty free

Applied to all at a tax rate of 30% reduction.

For example, if the consumption tax rate is 30%, the value-added tax 21% (= 30% × 70%)

In addition, I will show specific examples below.

http://www.gov.cn/zhengce/2016-03/26/content_5058511.htmIn addition, I will show specific examples below.

Contents

Before revision

After amendment

After amendment

Health food, miscellaneous goods, etc.

(There is a row tax exemption)

duty free

Increase value tax 11.9% (= 17% × 0.7)

Cases with import duties up to 50 yuan. Item price within 500 yuan.

11.9% tax increase

Health food, miscellaneous goods, etc.

(No row tax exemption)

Line Tax 10%

Increase value tax 11.9% (= 17% × 0.7)

Case of import tariff exceeding 50 yuan. Product price over 500 yuan.

1.9% tax increase.

Health food, miscellaneous goods, etc.

(No row tax exemption, product price 2,000 RMB)

Total: 27%

Tariff 10%

Increase tax 17%

Increase value tax 11.9% (= 17% × 0.7)

Case with a product price of 2,000 RMB (In case before revision, case treated as general trade). 15.1% tax reduction.

Apparel, fashion, electrical appliances

(No row tax exemption)

Row tax 20%

Increase value tax 11.9% (= 17% × 0.7)

Case of import tariff exceeding 50 yuan. Product price exceeds 250 yuan.

8.1% tax reduction

Cosmetics (without line tax exemption)

Row tax 50%

Total: 32.9%

Increase value tax 11.9% (= 17% × 0.7)

Consumption tax 21% (= 30% × 0.7)

Case of import tariff exceeding 50 yuan. Product price is over 100 yuan.

17.1% tax reduction.

This program is partially amended on May 25.

In the new customs clearance system from April 8, it was necessary to issue a customs clearance certificate (customs clearance only) for products not included in the positive list (front Qingnan). However, as of May 25, we have been able to import in China without issuing a customs clearance certificate as before.

There are three main factors behind the postponement measures. One is that products that can not be imported into bonded zones have accumulated. The second is that products related to transboundary ECs are being sent directly rather than via bonded zones. Third, there was more than expected impact on cross-border EC market.

As for the first one, the company was unable to respond to the acquisition of the customs clearance certificate immediately for products requiring the customs clearance certificate, due to the new customs clearance system, and a lot of products were accumulated in the bonded area more than expected.

For the second one, on the cross-border EC, one of the big aims of the new tax system was crackdown on the direct delivery model that avoids taxation, but contrary to its aim, direct shipment model transactions have increased It is. Cross-border EC's goods delivery method is large, there are a bonded area model and a direct delivery model. In the case of a bonded area model, from the background that the EC site business operator is proxy tax payment, we will properly put tax (customs duty, value added tax, consumption tax) in the process of entering into the bonded zone. On the other hand, in the direct delivery model, the goods recipient (China side) directly ship from the goods sender (Japan side), so the product recipient basically pays the tax (In some cases the EC site business operator may take tax on behalf of the EC site business ). However, since customs does not check all items, almost all items are tax-exempt (roughly, around 0.1% at shipping amount of less than 1,000 yuan, 1 to 3% at more than 1000 yuan Check rate).

Regarding the third one, in the transboundary EC test area (Hangzhou, Shenzhen, Ningbo, etc.), the transaction volume decreased by more than 6 to 70% compared to before the new tax system construction. It is thought that the Chinese government decided that the impact on the market is too big.

In this way, it is expected that such taxation will be adjusted accordingly, due to the development situation of transboundary EC and changes in consumer needs etc. We must continue to focus on trends in relevant policies.

Details will be updated soon.

-

personal income tax

Personal income tax is imposed on various income earned by natural persons. It is important to note that natural persons mentioned here include individual industrial merchants and others. By imposing personal income tax, the government not only ensures tax revenue but also corrects the disparity between individuals by adjusting individual income. Rationale for personal income tax The law on personal income tax promulgated in 1980 was the Personal Income Tax Act of the People's Republic of China, which was subsequently revised and now revised as of the end of fiscal year 2007 (enforced on March 1, 2008) is applied. At the time of this revision, the Personal Income Tax Law Implementing Ordinance of the People's Republic of China has also been revised.

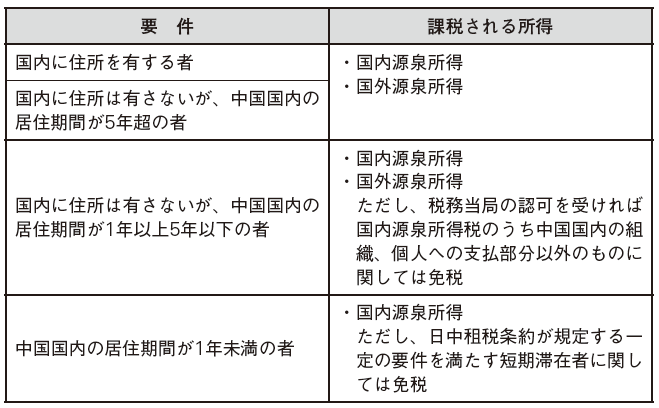

■ TaxpayerWhether it falls under the personal income tax payment obligor or not is determined by the domicile in China and the domestic residence period in China.

■Taxation standardIn calculating personal income tax, it is important to classify the taxable income corresponding to the tax base (the value underlying the calculation of the tax amount) or the tax free income not applicable.

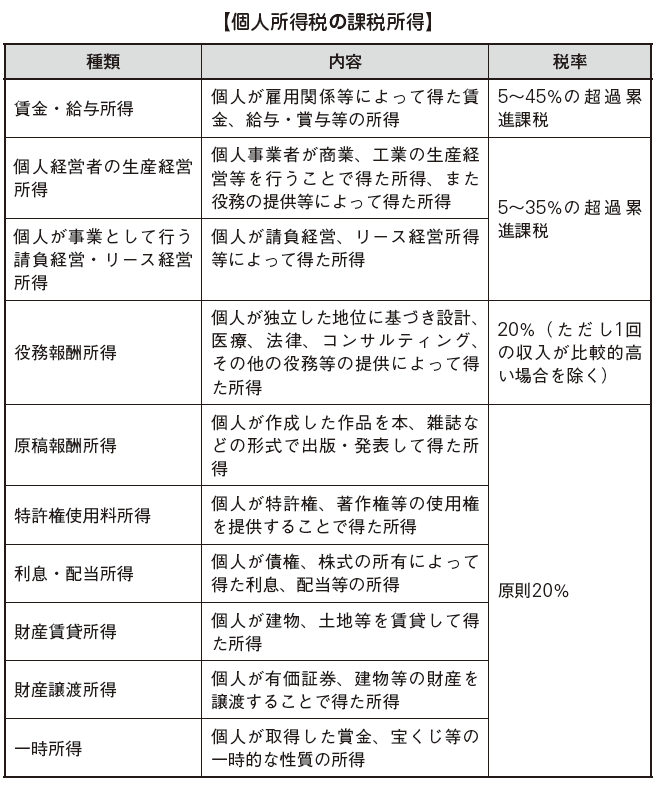

[Taxable income]Calculation method, tax rate, etc. will change for each taxable income of personal income tax.

[Tax-Free Income]The following income is stipulated as tax exemption income.

· Incentives for science, education, technology, culture, hygiene, physical education, environmental protection, etc, provided by national or local governments· Government bonds and interest on financial bonds issued by the country· Subsidies issued based on the unified regulations of the country, allowances· Welfare benefits, condolence money, relief money· Damages compensation· Military personnel transfer costs, vocational expenses· Housing allowance, retirement allowance, retired workers (pension), leave work (pension), living subsidies after retirement· Income of ambassadors, consular officials and other persons of embassies and consulates in China reserved for tax exemption under related laws in China· The international treaty that the Chinese government is a party, the tax free income according to the provision of the signed protocol· Other tax exempt income approved by the State Council Finance Division

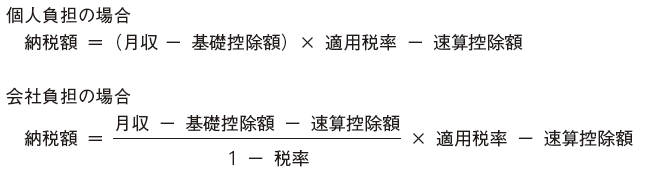

■ Calculation method[Wages / salary income] In the case of salary income, the calculation method differs depending on whether individuals pay the personal income tax or the company bears.

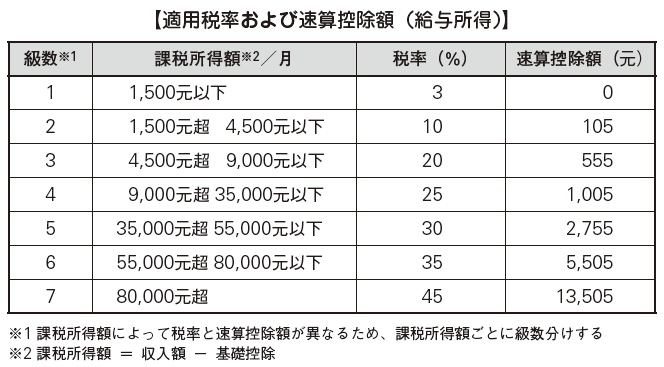

he basic deduction is 4,800 yuan for foreigners and 3,500 yuan for Chinese. The applicable tax rate and the deductible deduction are shown in the table below.

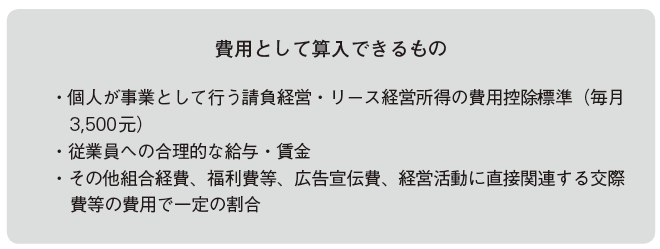

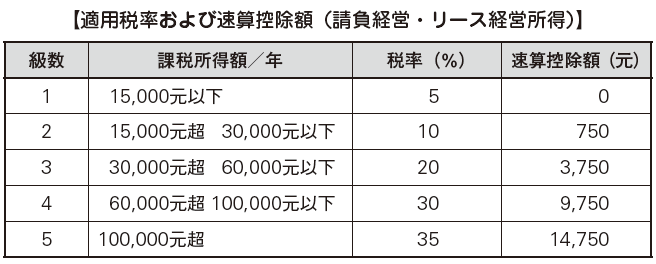

[Production management income, contract management, lease management income by individuals]The production management income of an individual manager is calculated as follows.

納税額=(年収-原価・費用・損失)×適用税率-速算控除額

Tax payment amount = (annual income - cost, expenses, loss) x applicable tax rate - budget deduction amount

The following table shows the applicable tax rate and the deductible deduction for contract management and leasing business income.

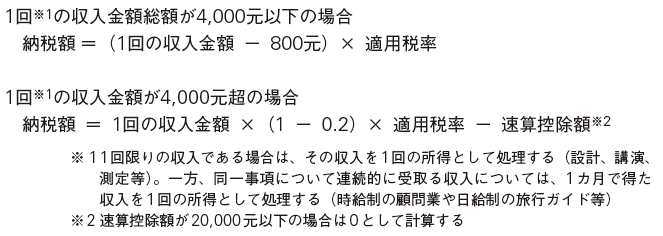

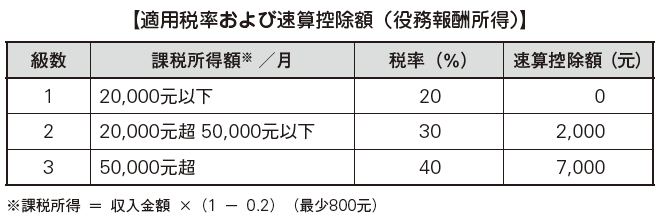

[Service fee income]The applicable tax rate of service fee income is basically 20%, but if the taxable income (amount of income of one time × (1 - 0.2)) exceeds 20,000 RMB the tax rate will change. If the income amount exceeds 4,000 RMB, caution is required because the deductible amount is different.

[Original reward income]The applicable tax rate for manuscript-based compensation income is 20%, but since it is multiplied by (1-0.3) by the formula as follows, the real figure is 14% (personal income tax law Article 3, paragraph 3).If the amount of income exceeds 4,000 RMB, the amount that can be deducted from the amount of income will differ.

When the amount of one payment is 4,000 RMB or lessTax payment amount = (one revenue amount - 800 yuan) × 0.2 × (1 - 0.3)

When the amount of income for one time exceeds 4,000 RMBTax payment = 1 revenue amount × (1-0.2) × 0.2 × (1-0.3)

[Patent royalty income]The applicable tax rate for patent royalties income is 20%, but as in the case of manuscript fee income, the amount of deductible from the amount of income will differ if the amount of income exceeds 4,000 RMB.

When the amount of one payment is 4,000 RMB or lessTax payment amount = (one revenue amount - 800 yuan) × 0.2

When the amount of income for one time exceeds 4,000 RMBTax payment = 1 revenue amount × (1-0.2) × 0.2

[Interest / dividend income]Regarding interest / dividend income, tax payment will be 20% of one revenue amount.

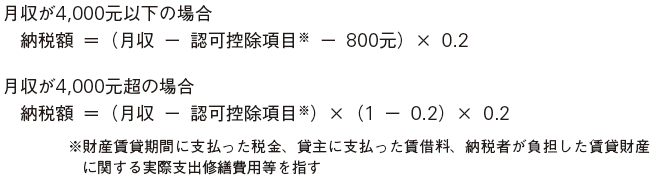

[Property lease income]The applicable rate of property rental income is 20%, but if the monthly income exceeds 4,000 RMB, the amount that can be deducted from the income amount will be different.

[Property transfer income]The applicable tax rate of property transfer income is 20%, but the tax deductible amount is calculated by multiplying the tax deductible amount by deducting certain expenses from the income amount. In addition, income earned by assigning houses (limited to cases where you do not have other residential houses) that individuals have for more than five years for personal use is exempted.

Property incomeTax Amount = (Revenue Amount - Cost - Cost) × 0.2

[Temporary Income]Temporary income is tax payment of 20% of the amount of one time income. However, for sports betting, disaster rehabilitation special lottery etc, less than 10,000 RMB will be exempted.

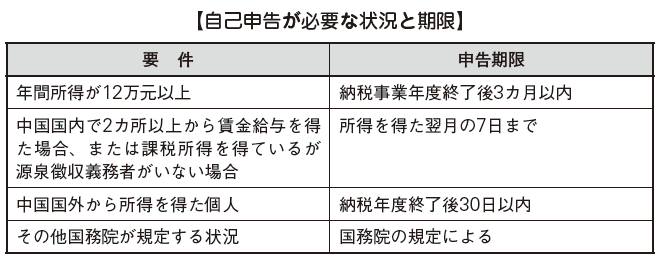

When the monthly income is less than 10,000 RMBExemptionWhen the monthly income exceeds 10,000 RMBTax payment = 1 revenue amount × 0.2■ Declaration / PaymentFor declaration and payment, there are individual self-declaration and declaration / tax payment by withholding tax, but here we describe self-assessment of individuals (see p. 406 "Withholding collection system"). There are four cases when self-declaration is necessary, and cautions are required because each deadline is different. Taxpayers are required to declare to the supervising tax bureau (Those who have an annual income of 120 thousand RMB or more need to submit other documents required by the supervising tax bureau, such as a copy of identification card in addition to the personal income tax declaration form ). The declaration method can be either data transmission, mailing (registered mail only), bringing it directly, intermediary institution with tax deputy qualification, substitute declaration by another person, or other method based on the regulations of the supervisory tax bureau.

-

Corporate income tax

The corporate income tax is the income tax that is taxed on other income, production income earned by the corporate organization in China. And the scope of the taxable subject and the tax rate differ depending on the form of the company.Before 2008, in China, we divided Chinese domestic enterprises and foreign enterprises and taxed them according to separate laws. After that, as a result of the integration of the tax law into one (January 1, 2008 enterprise income tax law) in order to rectify the tax differential of Chinese domestic enterprises and foreign companies against the background of China's international development, Many of the tax burden differences between them will be resolved.

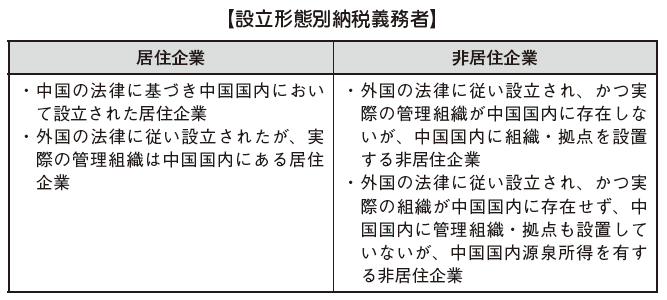

■ TaxpayerCompanies that are subject to tax obligations in China are categorized according to their form of establishment. There are two types of enterprises to be established: resident companies and non-resident enterprises, and the range of income to be taxed is different.

[Resident company]Resident companies are obliged to pay corporate income tax on domestic and foreign source income.

[Non-resident enterprises]In cases where non-resident enterprises have established organizations / bases in China (organizations that are substantially controlling and controlling enterprises' production management, personnel, accounting finance, etc.), occur in China domestic source income and outside China Among those that have been incurred, corporate income tax is required for income related to the organization / base.In cases where non-resident enterprises have not set up organizations / bases in China, or if the income acquired for those who have established organizations / bases are not related to them, payment of corporate income tax on domestic source income in China is mandatory I will.The representative office falls under non-resident enterprises and is subject to taxation in principle, but it will be tax exempted if certain requirements are met (see the "Representative office taxation" section).

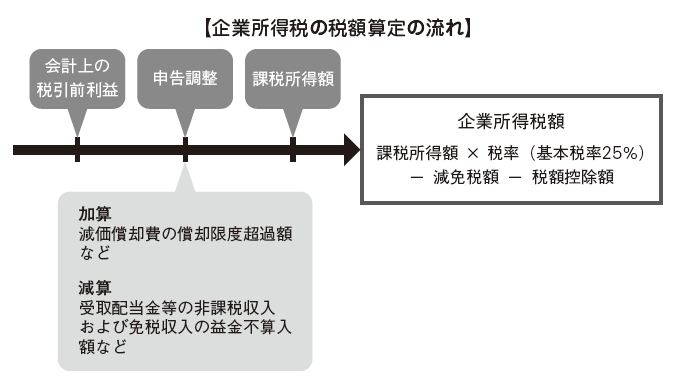

Calculation of tax baseThe standard taxable income is calculated by adding a certain adjustment to the pretax profit calculated accounting in the same way as in Japan.Specifically, cost, expenses and losses are compensated for from the total income for each tax year by accrual basis (see "Amount of money" and "Deductible amount") based on Chinese accounting standards Including the amount of prior year's loss that is recognized to be acceptable) and adjust tax exemption and tax exempt income after tax adjustments such as addition of non-deductible items and subtraction of non-taxable items. The adjusted profit and loss will be the taxable income.Companies are obliged to attach tax adjustment schedules for declaration adjustment to the annual audit report. This tax adjustment table corresponds to Appended Table 4 of Japanese tax return declaration. Unlike Japan, the style is not basically prescribed, there is no material equivalent to Appendix 5.The process leading up to the tax calculation of the corporate income tax by the tax return method is as follows.

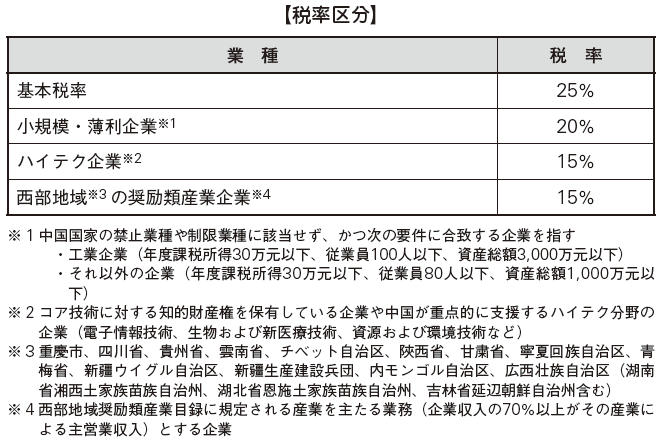

■ Tax rateWe calculate the corporate income tax amount by multiplying the tax base by the tax rate. The basic tax rate of corporate income tax is 25%, but please be careful as it may be different depending on industry as follows.

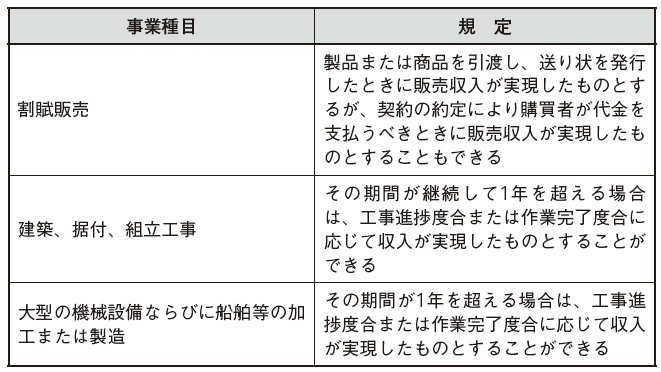

■ Amount of moneyAs for income tax in the Corporate Income Tax Law, it is calculated on an accrual basis as in Japan. Unlike cash basis, regardless of whether or not you actually received consideration, revenue generated within the period must be included in the amount of gross profit during that period. However, even if you receive consideration like the previous receipt of income, if you do not belong to earnings for the current period, it will not be included in gross profit for the current fiscal year.Regarding the following businesses, there is a special provision for exceptional recognition of revenue recognition.

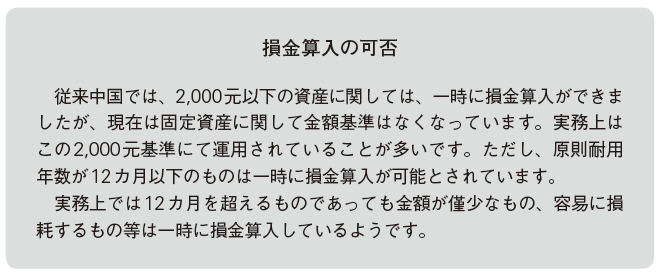

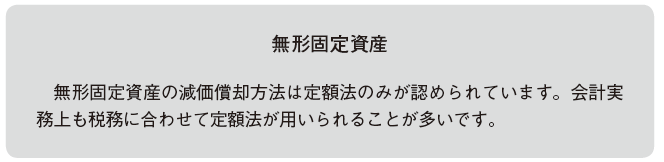

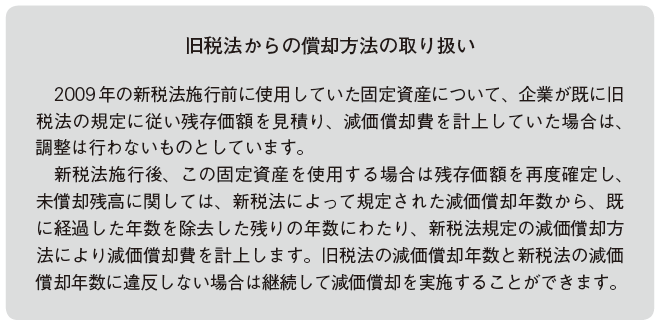

■ Deductible amountDeductible fees paid by companies are required to be truthful and legitimate. In other words, it is necessary to be able to submit evidence to prove that spending has actually occurred, and also to process according to the provisions of the tax law.Although the amount of deductible money is recognized on accrual basis, there are certain restrictions on deducting money. The special case is the timing of depreciation. In China, we do not depreciate in the month when we start using fixed assets, we will do from the following month.

DepreciationDepreciation and amortization refers to the cost reduction of fixed assets. When purchasing fixed assets, it is recorded as an asset, and its asset amount is converted into monetary amount as depreciation expenses according to frequency of use and year of use.

[Acquisition cost of fixed assets]If you purchase fixed assets, the acquisition cost will be the total cost including transport fee, installation cost and other incidental expenses, including those that occurred before the start of use. Vat tax relating to the purchase of fixed assets is included in the acquisition price of fixed assets. In addition, the following are mainly listed as included in the acquisition cost.

Finance lease fixed assetsTotal payment contracted to the lease agreement (including related expenses incurred by the lessee that occurred in the process of entering into the lease contract).

Borrowed Interest for Purchase of Fixed Assets The portion of interest expenses of borrowings for purchasing fixed assets that occurred before fixed assets were used as business.

Self-built fixed assetExpenditure that occurred before completion.

Investment in kindThe amount that the investor confirmed and passed through the evaluation of the asset evaluation office.

Fixed assets acquired through giftIf there is evidence from the donor, the sum of the amount stated in the voucher and the accompanying expenses etc.

[Useful life of fixed assets]Types of assets

service life/year

Buildings / structures

20

Machinery equipment, train, ship

10

Forest trees

10

Transportation equipment, tools / instruments / fixtures

5

Aircraft, train cars, carriers other than ships

4

Electronic equipment

3

Long-term prepaid expenses

3

Livestock

3

Intangible fixed assets*

Limited duration of contract

Contract period

No contract period limit

over10

* As for goodwill, it is not amortized by new accounting rules[Long-term prepaid expenses]The following expenses incurred in a company can be amortized as long-term prepaid expenses based on the provisions (Article 13 of the Corporate Income Tax Law, Articles 68 and 69 of the Act).

· Improvement expenditure of fixed assets depreciated· Improved lease fixed assets expenditure· Large repair expenditure of fixed assets· Other long-term prepaid expenses

Improvement expenditure refers to expenditure incurred due to changes in the structure of buildings or structures, extension of useful life, etc. Fixed assets are amortized based on estimated remaining useful lives and lease fixed assets are amortized based on the remaining lease term. Large repair of fixed assets means that repair expenditure reaches 50% or more of the tax base at the time of acquiring fixed assets and the service life of fixed assets after repair is extended by 2 years or more.

[Recording depreciation expenses]Depreciation expenses for fixed assets will be recorded from the month following the month of start of use of fixed assets. For fixed assets that have been discontinued, we will stop depreciation expenses from the month following stoppage of use.

[Method of depreciation]Depreciation methods are generally amortized by the straight-line method. However, for the following fixed assets, it is possible to adopt shortening of service life or amortization of acceleration (Article 32 of the corporate income tax law, Article 98 of the law enforcement act).

· Fixed assets with fast model changes due to technological progress· Fixed assets that are violently vibrating throughout the year and are ready to corrode

In adopting the reduction of the useful life, in the case of fixed assets purchased newly, it is limited to 60% of the statutory depreciation years based on the corporate income tax law, and in the case of used second fixed assets, it is limited to 60% of the remaining useful life . As an acceleration depreciation method, 200% declining declining method and series method are allowed.

In order to adopt shortening of service life and accelerated depreciation, the following procedures are necessary. If the following requirements are not met, the supervising tax bureaus will request companies to suspend the application of these provisions.

· Notification to the supervisory tax department within one month after acquiring the fixed asset· When filing a corporate income tax at the end of the fiscal year, field inspection of the fixed assets by the supervising tax bureau

[Residual value]The salvage value is the amount obtained by deducting the estimated disposal cost from the estimated disposal value at the end of the scheduled use period of fixed assets according to the nature and usage of fixed assets for each company. This is consistent with the provisions of the New Enterprise Accounting Standards (see Chapter 10 "Accounting").

■ Other deductible expenses[Management fee, etc.]Administrative expenses paid between companies, lease fees paid in the business period within the company, royalties for royalties and interest paid in internal nonperiodic banking period are not deductible.

■ Other deductible expenses[Management fee, etc.]Administrative expenses paid between companies, lease fees paid in the business period within the company, royalties for royalties and interest paid in internal nonperiodic banking period are not deductible.

[Advertisement cost and business promotion expenses]As a general rule, it is considered possible to deduct 15% of sales income for the current fiscal year (excluding non-operating income, including deemed sales as prescribed in the main business of the company and other sales and tax laws). Overdraft can be carried over to next fiscal year and beyond.Cosmetic Manufacture and Sales, Pharmaceutical Manufacturing, Beverage Manufacturing (Excluding Alcoholic Beverages) Advertising expenses and business advertising expenses incurred in companies can be deducted up to 30% of sales revenues for the current fiscal year.Advertising and business advertising expenses and tobacco expenses for tobacco of tobacco companies are not deductible.

[Asset Loss]For asset losses, documentation evidencing that the enterprise meets the recognition criteria for the loss on the asset is required. Below are examples of evidence relating to main assets (including other documents, vouchers, etc. specified in the tax law in addition to those listed below) Details of corporate assets loss Corporate income tax pre-deduction control law Laws 16 to 36 ). External evidence that has legal effect to prove that it satisfies the conditions for recognition of asset losses, and the internal documents of companies concerning specific matters are mainly as follows.

· External evidence with legal effect· Judicial sentence of judicial organization, ruling· Public Safety Organization's Settlement Proposal, Response Form· Certificate of deletion / suspension of leave issued by the industrial and commercial sector· Corporate bankruptcy liquidation announcement, payment document· Public documents of government agencies· Documents specified in other tax laws, vouchers, etc.

Internal document of company concerning specified matter· Materials related to accounting processing and original evidence vouchers· Asset inventory table· Transactional contract for economic activity· Appraisal documents and materials issued by the technical appraisal department inside the company· Decision documents inside the company, documentation on situation· Documents specified in other tax laws, vouchers, etc.

[Loss on monetary assets]A monetary asset is an asset that is in a cash or cashable state. Losses due to loss of monetary assets etc can be deducted on condition that the following documents exist.

Cash loss· In-house audit documents related to cash inventory tables, descriptions made on inventory losses· In-house audit document related to the explanation made by the cash holder against the inventory loss· Explanation of loss liability certification and status of compensation by the responsible person (on-site supervisor etc.)· If the cause of the loss relates to a criminal offense, refer to related documents issued by the judicial body· Certificate of taking counterfeit notes issued by the financial institution

Loss on bank deposit· Beneficial evidence of deposits and other assets· Legal documents concerning bankruptcy and liquidation of financial institutions

Loss on accounts receivable, advance payment· Related items Contract, consultation letter or instruction· In the event of bankruptcy or liquidation of the obligor, bankruptcy issued by the People's Court and public notice of liquidation· If it falls under the obligor's leave of absence, deletion of business license issued by the Industrial and Commercial Bureau and certificate of cancellation· If it falls under the obligor's death or missing certificate, a certificate concerning the death or missing of the obligor issued by the department related to the public security organs· If it falls under the debt restructuring, please refer to the debt restructuring consultation document and tax statement details on debt restructuring of the obligor· If it falls into a thing unrecoverable due to force majeure such as natural disaster, war, etc., explanation on the situation of the disaster encounter situation of the obligor and disclaimer of claim

If the receivables are dealt with losses exceeding 3 years, or certain receivables * with a due date exceeding 1 year, they can be recorded as bad debt losses. However, it is necessary to issue a situation explanation and a special report on it.* The amount of money which exceeds 50,000 yen for 1 mouth or does not exceed 1 / 10,000 of annual income of company

[Loss on nonmonetary assets]Nonmonetary asset refers to an asset that has not finished its return on investment such as fixed assets and inventory. Losses due to loss of non-monetary assets etc can be deducted on condition that the following documents exist.

Inventory loss (loss amount less amount of compensation)· Taxable inventory tax base document on determination of basic cost· Internal accreditation of internal responsibility, explanation of compensation status of responsible person and internal decision document· Instructions and confirmation materials on internal company's inventory disposal, damage, quality deterioration, residual value· Physical inventory table of inventory· Custodian's instructions on inventory loss

The theft loss of the inventory (the amount obtained by deducting the amount of compensation from the basic tax cost)· Taxable inventory tax base document on determination of basic cost· Notification documents to be submitted to public security organizations· In case of reparation by the person responsible for management of inventory assets or insurance company, explanation on damages situation etc.

Inventory loss of fixed assets, lost loss (amount deducting reparation from loss amount)· Company internal responsibility accreditation and confirmation materials· Physical inventory table of fixed assets· Materials related to the tax base of fixed assets· Inventory loss on fixed assets, loss situation document· If the loss amount is large, special report on technical expertise report or special report issued by intermediary agency with statutory qualification etc.

Loss on disposal / damage of fixed assets (residual value from the book value, amount deducting reparation)· Materials related to the tax base of fixed assets· Accreditation and confirmation of relevant responsibility within the company· Appraisal materials issued by relevant departments within the company· In case of compensation by the manager who is responsible for the fixed asset, explanation on compensation status· When the amount of loss is large, in case of damage or disposal of fixed assets due to force majeure such as natural disaster etc, special opinion opinion opinion or special report etc. issued by intermediary agency with statutory qualification etc.

Stolen loss of fixed assets (amount deducting reparation from book value)· Materials related to the tax base of fixed assets· Notification documents to be submitted to public security organizations, certification materials related to incident handling in public security organizations· In case of reparation by managers responsible for managing fixed assets, explanation on compensation liability certification and compensation status etc.

[Various provisions]Allowance for doubtful accountsAlthough it is possible to set up an allowance for doubtful accounts for accounting purposes, in principle, the provision for doubtful accounts is not deductible for tax purposes. It is permitted to record as a loss at the stage when it eventually becomes a bad debt loss.

Provision for impairment loss Under the Corporate Income Tax Act, impairment allowances are not permitted to be treated as expenses or losses. Provided, however, that the reasonable loss (actual asset loss) that occurred in the process of actually disposing and transferring the asset * owned or controlled by the company out of the deductible asset losses, and the actual disposal and transfer of the assets by the company Loss (statutory loss of assets) calculated and recognized without satisfying certain conditions is accepted.Actual asset loss must actually apply and apply for deduction in accounting loss treatment year. With respect to statutory asset loss, it is necessary to submit documentation evidencing that the enterprise meets the recognition condition of the asset loss to the supervising tax bureau and apply for the deduction in the accounting loss treatment year.External evidence with legal effect and internal document of company pertaining to specific matter are required as confirmation documents of asset loss.

* Monetary assets such as cash, bank deposits, receivables and advance payment items (including bills receivable, advances, intercompany debts), inventory assets, fixed assets, intangible assets, construction in progress, productive biological assets Non-monetary assets such as credit investment and equity investment

[Entertainment expenses]Entertainment expenses can be included in the amount of deductible up to 60% of the incurred amount (but up to 0.5% of the current fiscal year's maximum).

[Salary-related]In general, the amount of salary can be deducted. Social insurance premiums and commercial insurance premiums can also be deducted within the scope or criteria stipulated by the state or province.Employee welfare expenses can be deducted up to 14% of total salary and union expenses up to 2% of total salary. As for the educational expenses of employees, we can deduct the deductible amount up to 2.5% of the total salary amount during the current fiscal year. Overdrafts can be carried forward after the next period.

[Donation]You can deduct up to 12% of the total profit of the year up to the maximum. However, donations that can be deductible are limited to donations spent through public-interest social organizations, government departments over provincial level.

[commission]The commission (commission) related to production management that occurred in the company can be deducted up to the calculation limit stipulated below, but the excess portion can not be included.

■ Asset valuation in special cases[Business combination accounting]In the case of acquisition of equity or assetsThe acquiring company will evaluate the tax base value of the acquired equity or asset by fair value. Meanwhile, the acquired company needs to recognize gains or losses related to the transfer of equity or assets.

In case of mergerMerger enterprises will evaluate the tax base value of various assets and liabilities received from the company to be merged based on fair value. The company to be merged needs to calculate income tax as well as in case of settlement.

In case of divisionSplit firms will evaluate the tax base value of the assets they will accept based on fair value. The companies to be split evaluate the assets with fair value and recognize the profit and loss.

[Finance lease transaction]For fixed assets leased by finance lease, in addition to the total payment contracted to the lease contract, the related cost which took the time to contract is taken as the tax base value. If the total payment is not agreed to the lease contract, the related basic expenses required to contract in addition to the fair value of the asset is taken as the tax base value.

[Financial instruments]When financial instruments are actually disposed of or settled, the difference between the disposal price and the acquisition cost is recorded as income on taxable income, so if you evaluate it at fair value, it is necessary to adjust it for tax purposes.

■ Other[Carry over of deficits]Deficits that occurred in the corporate tax payment year (in cases where the amount obtained by deducting various deductible items, excluding tax exempt income and duty - free income from the total income for each taxable year is negative) can be carried forward and deducted from income of subsequent years can. The maximum number of years to carry forward is 5 years.

[Tax reduction system]With regard to specific industries and projects in the following ① to ⑨ in China, tax exemption or tax reduction system is established for tax purposes (Article 27 of the corporate income tax law, Article 86 to 91 of the Implementing Ordinance).

① Agriculture, Forestry, Farming, FisheriesIncome obtained by agriculture, forestry etc etc is reduced corporate income tax.

② Infrastructure Project Income obtained by engaging in investment management of the infrastructure projects (namely port project site, airport, railroad, road, urban public transportation, electricity, water supply, etc.) that the national government supports heavily The tax reduction tax is taken for the period.* The corporate income tax is exempted from the first to third fiscal year starting from the tax payment year, and the corporate income tax from the fourth to the sixth fiscal year is halved

③ Environment protection, energy saving, water conservation projectEnvironmental protection, energy conservation, water conservation project established by Ministry of Finance, State tax bureau, etc. Comprehensive use of public wastewater / garbage disposal, tungsten treatment, technological remodeling for energy saving and emission reduction stipulated in the income tax incentive incentive inventory, As for the income earned by engaging in projects such as desalination of seawater, a tax reduction tax is taken for three years of triple exemption as well as infrastructure project.

④ Dedicated capital investment for environmental protection, energy conservation, water conservation projectThe amount invested in a certain facility (fixed facility enterprise income tax incentive inventory and energy conservation · water saving special facility enterprise income tax preferential inventory and equipment dedicated to safety production enterprise income tax inclusive) for certain facilities invested (after purchase, self-use ) 10% of the capital investment amount can be deducted from the corporate tax payment amount.If we can not deduct, we can carry forward for 5 years. However, if the facility is transferred (including lease) within five years after the purchase of the facility, the preferential treatment system is not applied and the tax amount already deducted must be paid (Article 34 of the Corporate Income Tax Law, the Act Implementing Ordinance 100 Article).

⑤ Technology transfer projectWithin the taxable year, corporate income tax will be exempted for parts where technology transfer profits of resident enterprises do not exceed 5 million yuan, corporate income tax will be halved for parts above 5 million yuan.In the case that the projects of ③ and ⑤ are transferred within the applicable period, the transferee can continue to receive reductions only for the remaining period from the date of transfer (Article 89 of the enterprise income tax law) .

⑥ Company in the national autonomous regionAutonomous organs in the autonomous region autonomously obtaining the approval of the provincial, autonomous region, and directly controlled municipalities can decide to reduce or exempt the part attributable to local tax among corporate income taxes to be paid by companies in the same autonomous region (Article 29 of the corporate income tax law).

⑦ Including deductible expenses at company expenditureFor the following items expended by companies, in addition to the actual incurred amount, the following expenses can be deducted for deduction (Article 30 of the Corporate Income Tax Law, Article 95 and Article 96 of the Law on Implementing the Act).

· R & D expenses (actual incurred amount × 50%) arising from the development of new technologies, new products, new processes· Salary paid by hiring a disabled person and other employees who encourage employment by the state (actual occurrence × 100%)

⑧ Venture capital companyA venture capital company that invests in a company engaged in a venture business that the state needs to focus on and support, can deduct a certain percentage of the investment amount from taxable income (Article 31 of the corporate income tax law Implementation Ordinance 97).When a venture capital company invests in an unlisted small and medium-sized high-tech enterprise for more than two years according to the equity investment method, 70% of the investment amount is deducted from the taxable income of the venture capital company in the year when the equity investment becomes full two years can. Amounts that can not be deducted in the current fiscal year can be deducted for carryover after the next fiscal year.

⑨ Comprehensive resource utilization company Companies on incentive tax incentives catalogRevenue acquired through production of products that conform to national and industry related standards (excluding those prohibited by the state) with the main materials of 16 types of resources specified by the comprehensive resource enterprise income tax preferential inventory (2008 version) , It can be reduced to 90% to be the total revenue (Article 33 of the corporate income tax law, Article 99 of the law enforcement act).

[Tax deduction]As in Japan, there is a foreign tax credit system in China.

① Foreign tax creditFor the following taxable income of income acquired by a company, the income tax tax paid outside the country can be deducted from the current tax payment amount.

· Taxable income of resident enterprises outside China source· Taxable income acquired by non-resident enterprises with mechanisms and bases in China, taxable income that occurred outside of China, but has actual relationship with the institution, base

There is a limit on the tax deduction, and the maximum tax payment calculated based on the provisions of the Corporate Income Tax Law for that income is the maximum amount. For parts beyond the deduction limit, you can deduct carryforwards from the balance after deducting the deductible tax amount for the current period within the deduction limit for each fiscal year within 5 years from the following period.China's foreign tax credit is a country-specific limit method that calculates the deductible limit for each country. In the case of Japan, it is not calculated by country, so it is called bulk limit method.

② Income tax paid by foreign companies abroadThe income tax amount actually paid by overseas control companies overseas by the domestic controlled enterprise concerning the interest on China's foreign interests, dividends etc acquired by the resident enterprise from a foreign controlled entity (foreign enterprises controlled directly or indirectly) is explained in ① As stated, it can be deducted within the range of the deduction limit prescribed by the Corporate Income Tax Law.

③ Tax calculationFor corporate income tax, the tax amount is calculated based on the tax rate of 25% of the taxable income for resident enterprises. Regarding non-resident enterprises, if the facility belonging to China is a PE (permanent establishment), the domestic income of China and the income attributable to PE out of income attributable to PE are taxed based on the 25% tax rate It is calculated. If a company without facilities and facilities in China gets income such as dividends, interest income or royalties in China, the tax amount is calculated based on the 10% reduction tax rate for that income.