Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaChina

12 Chapter International taxation strategy

-

-

Points to keep in mind when withdrawing from business

Withdrawal from business in China is often accompanied by difficulties. The reason is that Chinese authorities do not like to withdraw investment, local connection is indispensable because there are areas where humanitarianism still remains, and Chinese courts are reluctant to resolve disputes among investors, There are many favorable court decisions on the Chinese side. In withdrawing, it is important to prepare a solid strategy in advance and to take appropriate measures while also including experts such as lawyers and accountants. -

Tax considerations

There are two methods of withdrawing from the Chinese business, roughly divided into dissolution, liquidation and transfer of equity.

■ Dissolution · LiquidationOf the methods of withdrawing Chinese business, we will explain issues to be noted at the time of dissolution / liquidation according to form of advancement, various taxes related to liquidation, tax treatment at investor side.

[subsidiary]In the liquidation of the Chinese subsidiary, the Chinese subsidiary, which had been subject to tax reduction tax incentive treatment, may incur additional taxes. A subsidiary that has received corporate income tax reduction tax measures (tax exemption for two years and 50% tax reduction for three years), if the project period is less than 10 years, the preferential treatment will be canceled and the total amount of tax reduction tax so far We have to pay. A subsidiary that had received import tax exemption (import value added tax and customs duty) of imported equipment, if it is within 5 years from the day of customs clearance and resells it to a domestic company in China, part of the tax-exempt amount (Foreign invested enterprises overseeing export and import cargoes and Article 18 of the tax collection valve law).

[Representative Office]In liquidation of a representative office, if there is clearing income, it is necessary to pay corporate income tax. Also, even for a representative office that is tax-exempt certified, it is necessary to certify to the taxing department that there was no income (National Tax Bureau [2010] No. 18, Foreign Corporate Representative Office Tax Revenue Management Interim Valve Method).

[Branch]Regarding the liquidation of the branch office, the head office must pay the corporate income tax up to the present year (collecting corporate income tax that runs across the district and collectively pay taxes) Article 5 (1) (4) of the temporary valuation method.

[Clearing Income Tax and Various Taxes]Before liquidationIn the course of the fiscal year, in case of terminating and liquidating business activities, you must file a tax return of the current corporate income tax to the tax authorities within 60 days from the end date.

After liquidationIn the liquidation process after the end of the management activity, distribution tax such as value added tax, business tax etc. occurs when property is transferred. As a result of liquidation, if clearing income occurs, in principle the tax will be levied on that liquidation income. Clearing income is the net realizable value of all assets, or the balance obtained by deducting net assets, clearing costs and related expenses from the transaction price.The settlement income tax is imposed on the above taxable income by deducting the tax loss carryforward from the previous year and a standard tax rate of 25%. The preferential tax rate is not applicable during the liquidation period.

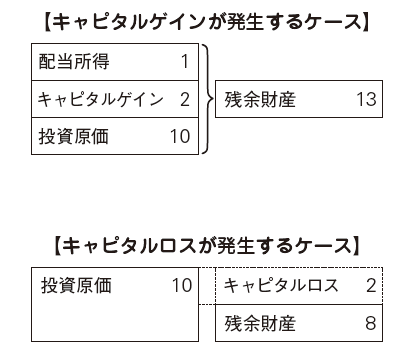

[Investment process]Of the residual assets acquired by the investor of the liquidation company based on the dividend, the portion calculated based on the shareholding ratio of the investor in each of the liquidating company's retained earnings retained earnings and retained earnings surplus is the dividend income. Capital gains (gains on transfer) will be taken if the amount obtained by deducting dividend income from residual assets exceeds the investment cost. If residual assets fall below the cost of investment, it will be capital loss(transfer loss).

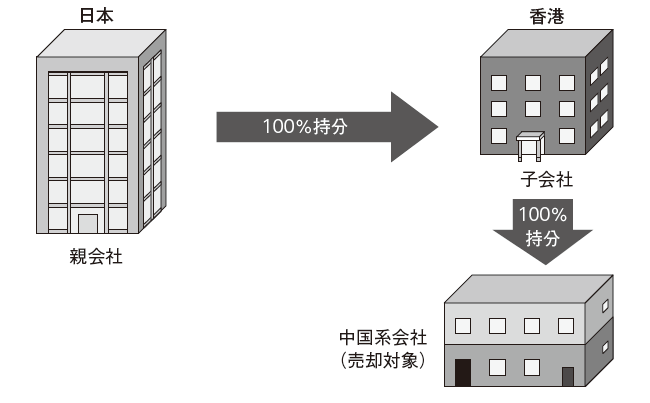

■ Equity transferIf you have established a wholly-owned subsidiary or a joint venture, you have the option of transferring the equity as a way to withdraw. I will explain matters to be noted and how to calculate transfer income by advance form.

[Whole subsidiary]100% Stakeholder When assigning a share of a subsidiary in China, it is necessary to change the registration at the registrar, with approval of the approval authority. According to some regulations concerning equity change of foreign invested enterprise investors, concrete processing procedures are as follows.First of all, we create an equity transfer agreement, and if there are investors other than the parties, we will obtain agreement of all of them. Next, you will apply to the approval authority at the time of establishment, change the change of the certificate of approval (rewrite of the business license) and register the change to the customs office of the tax office, the Finance Bureau, and the competent jurisdiction.Attention should be paid if the company has undergone a preferential policy of exemption for 2 years or halving for 3 years if the company changes from a foreign capital company to a domestic capital company through a share transfer. In the case that the company is less than 10 years, there is an obligation to return part or all of tax reduced or exempted for the period that received the preferential policy.

[Joint Venture]Cases to be transferred to China investorsIn the case of transferring a joint venture's interest to a Chinese investor, the joint venture will be reorganized into a Chinese company, so tax relief tax incentives enjoyed by the Chinese joint venture as well as a wholly owned subsidiary will be canceled. As a result, there is a possibility that an additional tax liability may arise as in the case of the Chinese subsidiary being dissolved or liquidated.In the case that the investment ratio of foreign capital is less than 25%, there are disadvantages such as being unable to enjoy the tax incentive measures, so the partner in China often refuses to transfer the contribution of foreign capital. When transferring an equity interest, it is necessary to obtain approval from an authorized body in China.

Case of transferring to a third partyIn the case of transferring a joint venture's shares to a third party, the consent of the Chinese investor is necessary. There is provision that each investor has priority purchasing right of the equity interest and consent right (Chugai foreign enterprise enterprise law enforcement regulation). If the third party is a foreign company and the equity ratio of the Chinese invested company that invests the unique asset is changed, the transfer of the equity will be evaluated by the asset evaluation office registered with the inherent asset management agency Additional processing such as must be done.

[Calculation of Assigned Income]Transfer income is calculated by subtracting transfer cost from transfer income. A 10% corporate income tax is imposed on transferred income. Income tax on corporate income is recognized in Japanese corporate tax law, but corporate income tax in China is subject to foreign tax credit.

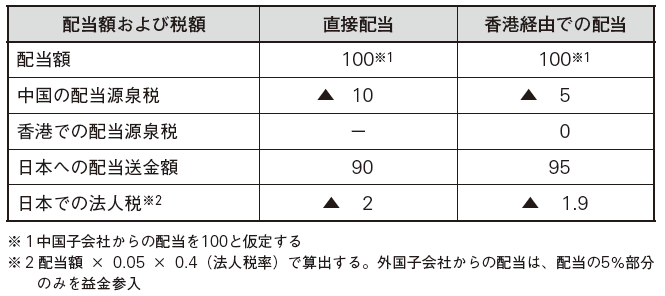

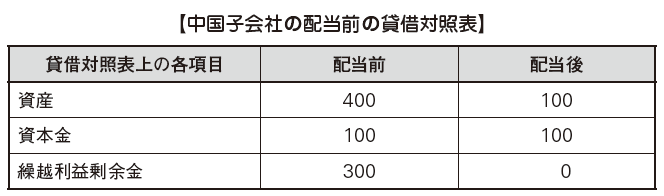

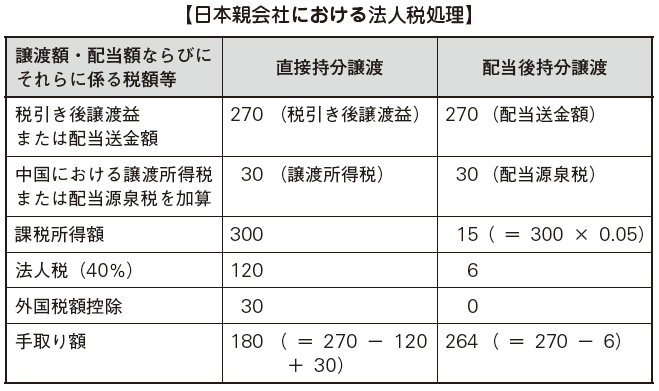

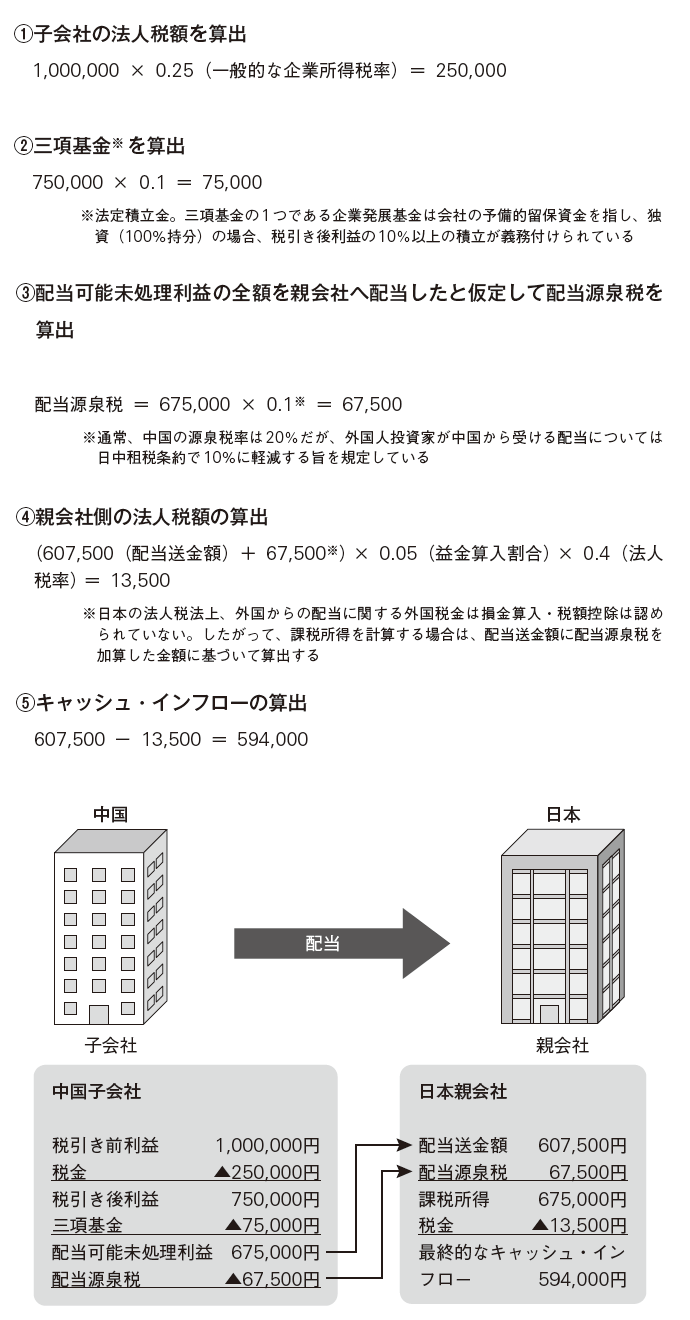

[Strategic equity transfer]If you pay a dividend before you transfer the equity, you can reduce the tax burden. Dividend processing is due to affecting the condition of the transfer of equity, which is not always a good idea, but it is an effective means. Below, we will compare and verify the case of transferring the equity directly without dividing and the case of transferring the equity after dividing. The relationship between the Japanese parent company and the Chinese subsidiary shall be 100% equity and the dividend shall be 300.

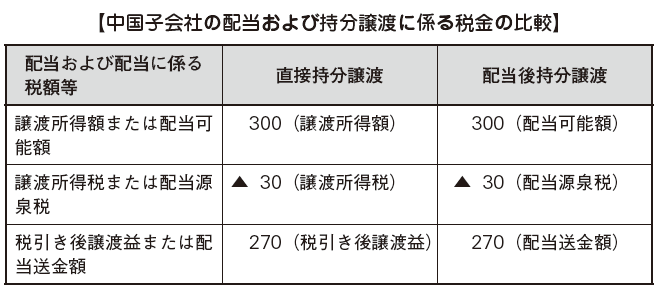

In case of direct transfer of equity interestIn the case of directly transferring the equity interest, the transferred income amount will be 300 (transfer profit 400 - transfer cost 100) and a transfer income tax rate of 10% will be imposed. Thereafter, according to the Japanese corporate tax law, the taxable income amount 300 (profit after tax transfer 270 + transfer income amount 30) is calculated and 40% corporate tax is imposed.Furthermore, the corporate income tax amount on transfer income in China is deemed as a foreign tax credit amount, and the takeover amount will be 180 (transfer profit 270 - corporate tax 120 + foreign tax credit 30).

In case of transfer of equity after dividendIn the case of transferring an equity interest after dividends, a 10% dividend withholding tax is imposed on the dividend. Thereafter, according to the Japanese Corporate Tax Law, only 5% is taxed on dividends from foreign countries, so the taxable income amount 15 ({dividend remittance amount 270 + dividend withholding tax 30} × 0.05) is calculated and 40% It will be. As a result, the takeover amount will be 264 (dividend remittance amount 270 - corporate tax amount 6).

VerificationAs a result of the above, it can be seen that, in the case of transferring the equity interest after dividends, the takeover amount is 84 (264-180) more than in the case of directly transferring the equity interest. If the profit that will be the source of the dividend is the profit that occurred before January 1, 2008, dividend withholding tax in China will be tax exempt based on the preferential tax system, which is effective in reducing tax burden.

-

g

g