Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaChina

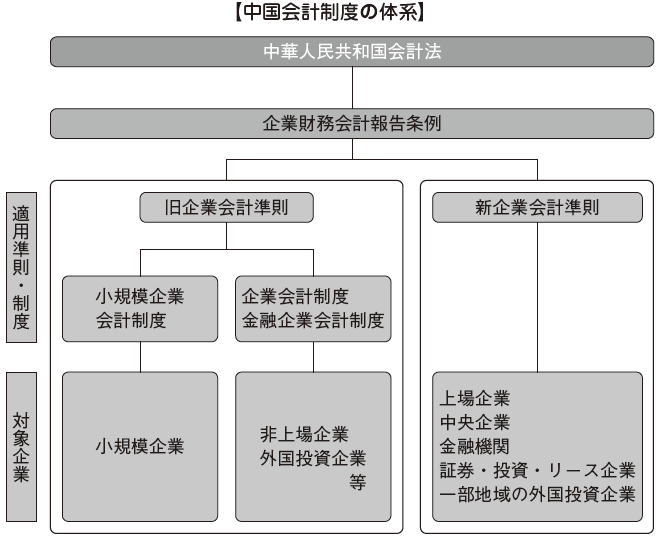

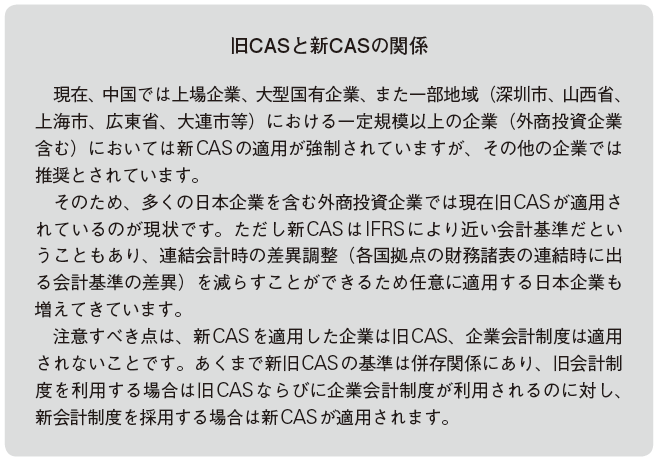

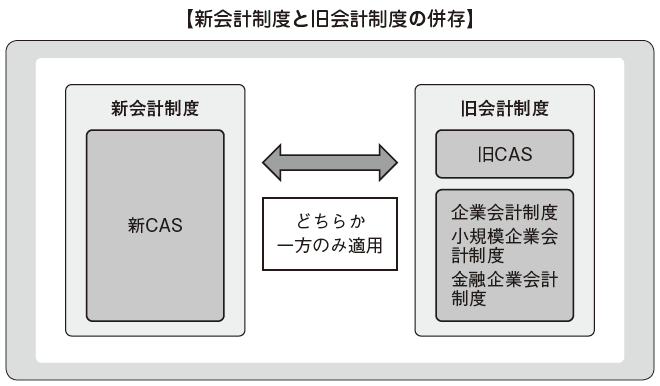

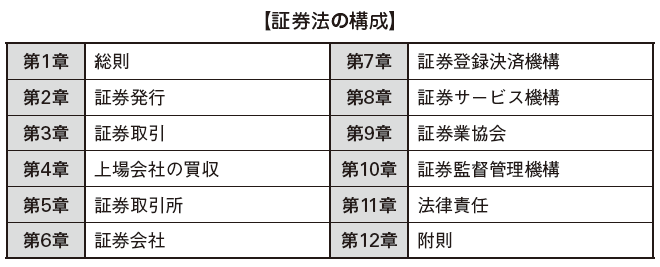

10 Chapter Accounting

-

-

Audit system

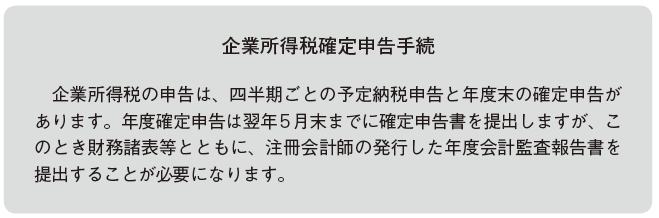

In China, companies are required to prepare financial statements at the end of each fiscal year and to have an audit of the accountant office / audit corporation according to the law (Article 165 of the Companies Act).Foreign investment enterprises must submit the annual financial statements to relevant organizations by attaching the audit report issued by the accounting accountant by April 30th from the settlement date (December 31). -

Audit system and internal control in China

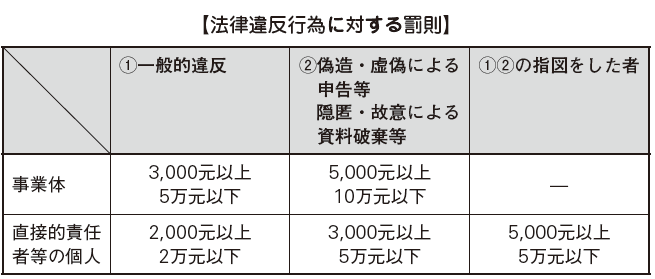

■AccountantChina employs an accounting system that allows accounting practices only for persons with accounting qualifications (Article 38 of the Accounting Act). The accountant will do from booking to tax return. The qualification equivalent to a certified public accountant in Japan is an accountant accounting professional, qualified as an accounting practitioner. Accounting professional refers to the person in charge of financial accounting within the company.In order to conduct accounting work within the company as an accounting practitioner, it is necessary to pass the accounting qualification examination. After passing, you will receive certain continuing training in addition to registration registration. In 2013, the Accounting Employment Qualification Control Law was revised and enforced, and there were some changes such as continuing educational management of unit system and paperless of examination, but when accounting work is outsourced to accounting office etc, accounting qualification possession If it does not hire a person, it is amendment to the extent that it does not affect the practice.The level of the examination has three levels of elementary, intermediate, and advanced, and accounting professionals are classified into four groups: accounting professionals, accounting professionals, accounting consultants and accounting personnel. Accounting as an Accountant Employee qualifications can be acquired by passing the elementary level and then appointed as Assistant Accounting Professional by taking certain practices. The accounting professional is an intermediate examination passing examination, and the luxury accountant needs the government certification in addition to passing the luxury examination.If the company conducts accounting practices etc. to persons without accounting qualifications, a penalty of 3,000 to 50,000 RMB will be imposed and will be subject to administrative penalty.

■ Notebook Accounting professional system[Note Accounting Professor]Qualified people equivalent to certified public accountants in Japan are called accounting practitioners in China in China. In order to be an accounting professional, after passing the papers accounting master examination, it is necessary to apply to the papers Accounting Professional Association, receive continuous training and meet certain requirements of practical experience and more.Note When you select accounting professionals, it is often that you usually ask the local accountant office. Therefore, it is important to work closely with the local accountant office, the staff of the parent company, and the audit corporation of the parent company. It may be possible to unify the audit corporation of parents and subsidiaries according to circumstances.Notebook The Accounting Professional Association was established in 1988 as an accounting professor's industry organization. Note The Chinese government department responsible for the Accounting Professional Association is the Finance Bureau and the Ministry of Civil Affairs. The association is engaged in the establishment of professional ethics, the accounting master's examination and implementation of the continuous training system, the examination of registered accounting office, etc. as the main work.

[Notebook work of accountant]Note The main task of accounting professionals is divided into audit work and non-audit work.

Audit work (Notebook Accountant Law Article 14)· Audit corporate financial statements and submit audit reports (including clearing financial statements)· Verify company capital at company establishment and submit investment inspection report· Conduct audits on company merger, division, liquidation and submit related report· Conduct other audit work as stipulated in laws and other administrative regulations· Other reviews, etc. for consolidated accounting etc.

Non-audit work (Article 15 Accountant)· Accounting consulting service· Accounting entries and substitution for preparing tax returns· Asset valuation service (However, valuation of state-owned assets is carried out by a valuable note asset evaluator)

[Notes Tenure of Accounting Professional]Notebook The term of accounting is usually one year and reappointment is also possible. Election is based on a resolution of the General Meeting of Shareholders, but if you do not re-appoint or dismiss it, you must make a public notice to the relevant publications and notify the relevant agencies. In addition, it is also necessary to give notice to the Accountant beforehand and to give opportunities for excuses at the general shareholders meeting.

Audit by foreign invested enterprisesThe auditing system of foreign invested enterprises includes internal audits by internal corporate auditors and external audits by external accounting accounting professionals (investment audits and annual audits are conducted by external accounting ledger). Furthermore, since 2006 the new corporate law came into effect, it is obliged to establish auditor (equivalent to corporate auditor of Japan) and supervisory board (equivalent to the board of corporate auditors of Japan).

[Investment verification]For companies established by law in China, shareholders must receive investment inspections by the investment inspection organization after paying out the investment funds and receive investment inspection certificate (Article 29 of the Company Law). Foreign invested enterprises are obliged to verify investment at the investment stage (Article 29 of the Chugai Joint Venture Company Act Implementing Ordinance, Article 22 of the Chugai Business Collateral Corporate Law Implementation Law, Article 32 of the Foreign-owned Enterprise Law Implementing Regulations).Investment verification is a procedure to verify that both foreign and Chinese sides verify that foreign invested enterprises are surely making money, spot, etc. contribution. It is legally obligatory to obtain investment verification report from the accountant office in compliance with the law.In the case of capital investment, we receive investment verification within 60 days after investment and we will receive investment verification report within 10 days after verification is completed. The company holds the document and makes it evidence of investment. Careful attention is necessary because capital investment is also necessary when making capital increase etc. (Submission destination is Industrial and Commercial Administration Bureau, Foreign Exchange Administration Bureau, etc.).

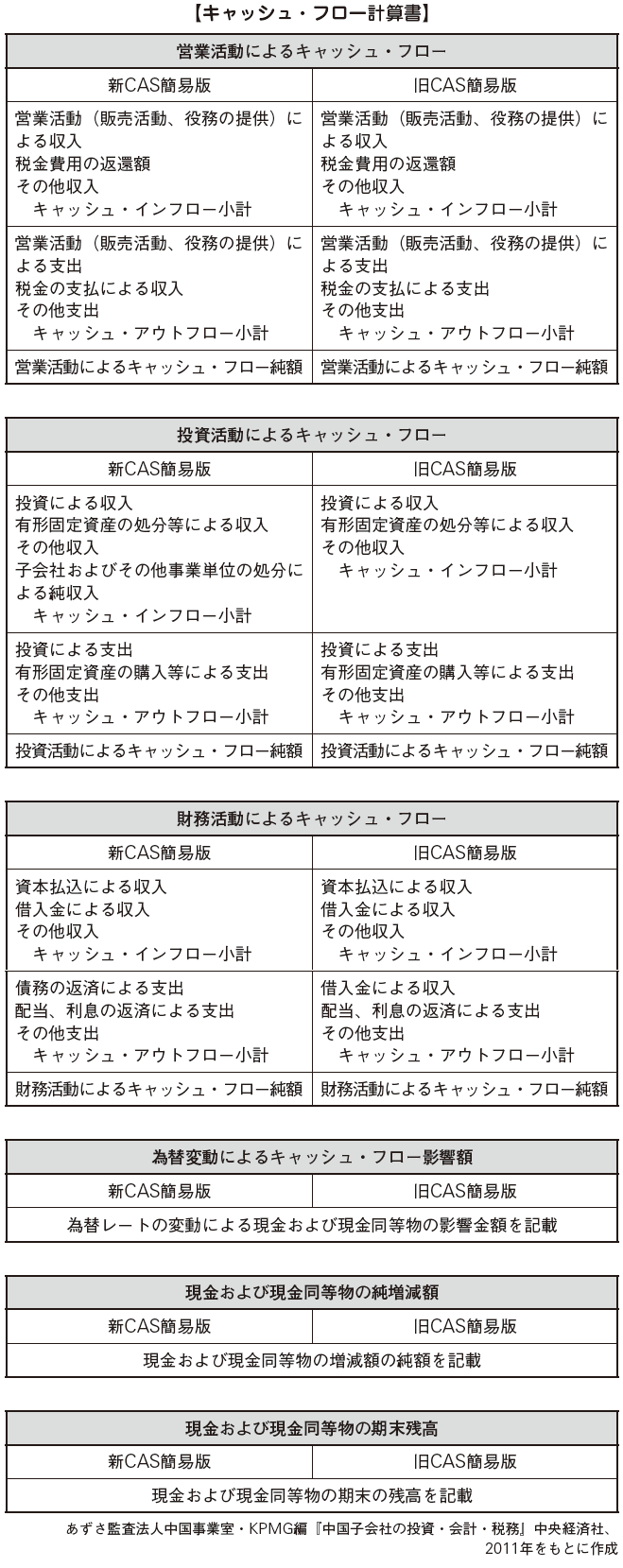

[Yearly audit]Under the Companies Act of China, it is stipulated that the company must prepare financial statements at the end of the fiscal year and receive an audit of the accountant office according to the law (Article 165 of the Companies Act). Foreign invested enterprises are obliged to receive annual audits at the end of every fiscal year (Article 79 of the Chugai Joint Venture Company Act Implementing Ordinance, Article 46 of the Chugai Regional Cooperative Enterprise Law Implementing Law, Article 60 of the Foreign-owned Enterprise Law Implementing Regulations).There are accounting audits and foreign currency audits for fiscal year audits. Foreign invested enterprises must submit audit reports to the relevant financial institutions with annual financial statements attached to the fiscal year financial statements between April 30th and the end of the fiscal year (December 31st) (The submission destination is Industrial and Commercial Administration Department, Foreign Exchange Administration Bureau, Taxation Bureau, Total 6 Departments). Foreign invested enterprises will ask the accountant office to receive an audit report by the due date of the annual financial statements. In addition, we can also receive voluntary audits for consolidated accounting etc. of our parent company. For listed foreign-invested enterprises, it is obligatory to submit interim reports in addition to annual financial statements. However, with respect to the interim financial statements included in the interim report, it is unnecessary to audit the accounting auditor except for certain cases (see P.450 "Audit of listed companies").

Accounting auditThe accounting audit is to report the financial statements prepared by foreign independent investors in a voluntary independent third-party accounting book on the appropriateness of their financial statements based on relevant laws and regulations. An accounting audit report will be issued after the accounting audit.

Foreign currency auditForeign currency audit is an independent independent third-party accounting practitioner who reports on the foreign currency balance situation of the inspected company. A foreign currency audit report will be issued after the end of foreign currency audit.

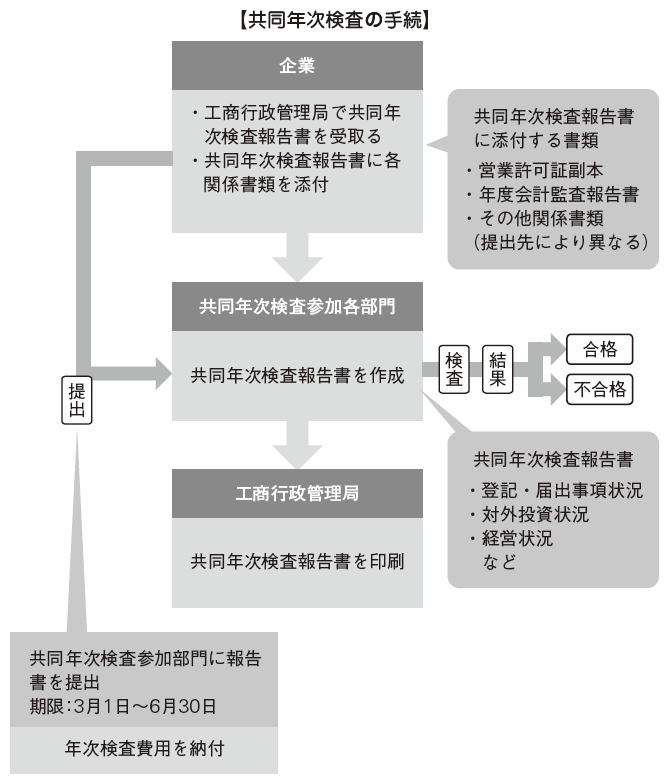

■ joint annual inspectionJoint Annual Inspection (Union Yearly Opinion) is a joint inspection by foreign enterprises invested enterprises jointly by the Industry and Commerce Administration Bureau, Foreign Exchange Administration Department, Tax Bureau, Commerce Department, Finance Department and Customs etc.

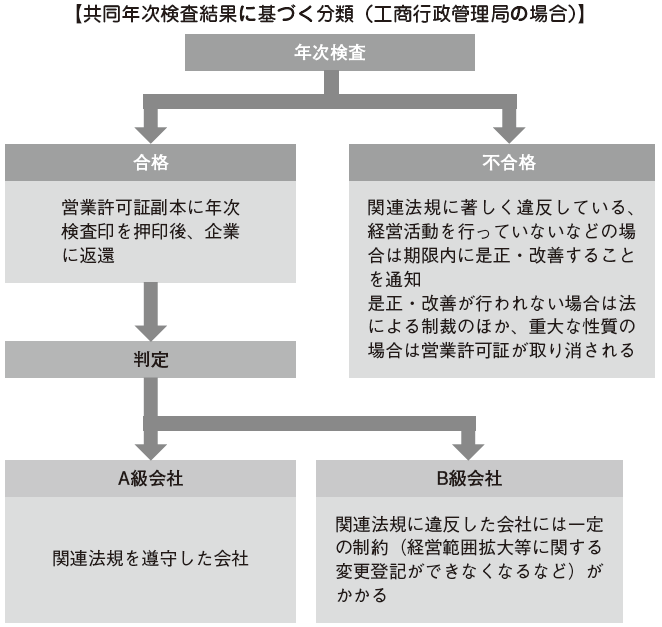

The procedure of the joint annual inspection is as follows. The company receives the joint annual inspection report at the Industrial and Commercial Administration Bureau, fills in necessary items, attaches other necessary related documents, and sends them to each joint annual inspection participation department I will send it. Documents to be submitted vary by region. After that (after several weeks), the result will be notified from each joint inspection participation department after paying the annual inspection fee.In case of failure, the company must take corrective measures and improvement measures within the time limit specified by the government official. In addition to sanctions by law if appropriate response is not taken, business license may be canceled if the content is serious. Even if you pass, certain limitations will be added if you are certified as a Class B Company.In some areas, the introduction of the annual inspection by the Internet is being promoted and there are cases where it is not necessary to go directly to the government agency, so it is important to check the instructions of each local government before proceeding. The Joint Annual Inspection Report needs to be submitted to each relevant organization from March 1 to June 30 of the following fiscal year. However, if there is a legitimate reason, it is possible to extend the deadline for up to 30 days after obtaining the approval of the relevant agencies. Newly established companies will be participating from the following fiscal year.

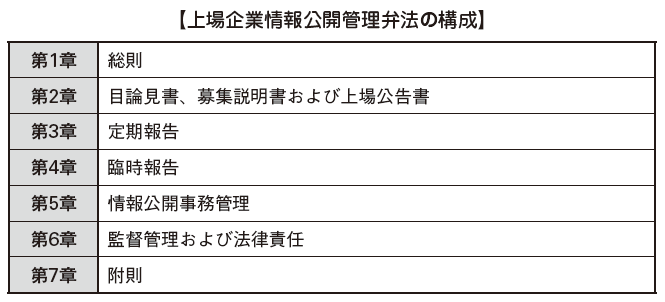

■ Audit of listed companies[Accounting audit] In addition to annual financial statements, listed companies are obliged to submit interim reports. However, with regard to the interim financial statements included in the interim report, no accounting auditor is required, except in the following specific cases.

· The audit opinion in the last three years was not an unqualified opinion (opinion of an accountant judged to be appropriate in all important points of the financial statements), and application or implementation of stock dividends or new shares was issued in the second half Case· In the interim period, dividends, capital stock of capital reserves or supplementary deficitIn the case of implementation in the second half

Listed companies are also supervised by the China Securities Regulatory Commission, in addition to the accounting auditor's note.

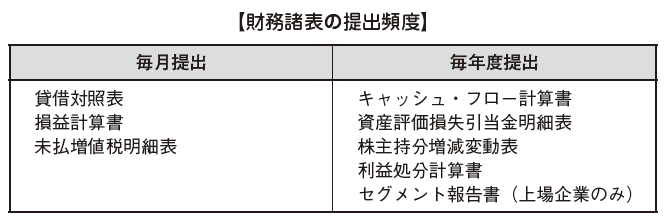

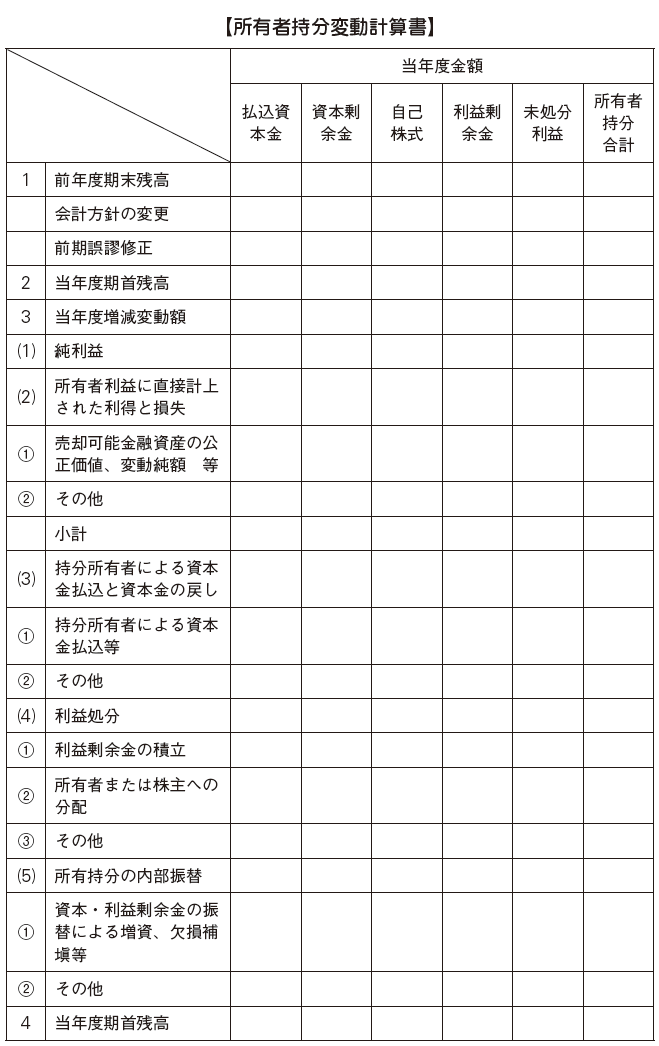

Submission scopeIn addition to preparation of individual balance sheet, income statement and cash flow statement, preparation of consolidated financial statements is required.

Submission DeadlineWhile the deadline for submission of annual financial statements is within four months from the end of the fiscal year, the deadline for submitting the interim financial statements is within two months from the end of the first half.

[Internal Control Audit]Internal control audit is implemented for listed companies, guaranteeing the truth and completeness of compliance of corporate management and management, asset preservation, financial reporting and related information, improvement of management efficiency and effectiveness, improvement of corporate development strategy We are aiming to realize (see page 454 "SOX Act of China").

■ Risk managementIt is important to consider various country-specific country risks in China when doing business in China. Specifically, there are uncertainties about the future of exchange rate fluctuations, relationships with joint venture partners, infringement of other intellectual property, boycottes due to anti-Japanese emotions, and lack of legal system.It is also important to consult with specialist consultants and legal experts on country risk, and it is also important to deal with companies withdrawing business due to lack of internal control of Chinese subsidiaries, It is necessary to pay attention to the current situation that there are many.Below, from the perspective of maintenance and operation of the internal control of the Chinese subsidiary, we will touch on risk management in doing business in China.

[Response to risk]Responding to risks can be divided into activities to avoid risk beforehand and correspondence after risk occurrence. In any case, it is necessary to work with the head office in cooperation with a Chinese subsidiary.

Activities to avoid risk in advanceIn order to avoid the occurrence of risk, we must have all stakeholders recognize our company's basic policy on risk response, not only to the management level of the company but also to the employee level. On the other hand, it is necessary to construct and maintain an internal control system for risk aversion. In addition, it is important to prepare manuals to ensure that the internal control system is operated, to periodically check whether they are properly operated and to establish them in companies.

Response after risk occurrenceIt is most important to solve not only the solution to the risks that occur but also the risk quickly. Especially for risks that can not be predicted beforehand, it is important to prepare for minimizing damage, such as maintaining an emergency contact network with the headquarters, not by only subsidiaries.

OtherIn Chinese subsidiaries, documents are usually created in Chinese. Therefore, when preparing a report to the parent company it is necessary to translate it into Japanese (or English). There is also a way to create the report itself from the beginning in Japanese (or English), but it is thought that it is desirable to create it in Chinese to promote the development and operation of the internal control by the local staff.Importance of Chinese subsidiaryIn conducting financial reporting by the parent company, depending on whether the subsidiary in China considers importance or not, the response to internal control assessment and maintenance will change.If a subsidiary in China is included within two-thirds of consolidated sales from the top of sales of each consolidated group company, the Chinese subsidiary is recognized as an important business base. In this case, in addition to enterprise-wide internal control, it is necessary to evaluate financial accounting reporting process, business process, general control over IT. Even if it does not correspond to an important business base, if it is judged that importance and risk (management, accounting, legal risk, etc.) exist in individual business processes, in addition to companywide internal control, settlement financial report Process and business processes may need to be evaluated. In this case, the points that the Chinese subsidiary should deal with are as follows.

· Clarify matters required by the parent company and clarify matters to be addressed by the Chinese subsidiary· Understand the internal status of internal control of subsidiaries, grasp the status of external audits, also grasp the status of external audits, and also grasp the subsequent countermeasures, etc.· Based on the above, devise plans for work required for subsidiaries

In addition, it is important not only to strengthen the coordination to cooperate with the parent company, to reconfirm and understand the policy of the parent company, but also to raise the importance of internal control to Chinese local staff.

■ Chinese SOX ActIn China, the internal control system has been expanded since the 1990s. Independent audit standards No. 9 was promulgated in 1996 and the basic concepts of internal control (organizational structure, procedure method, internal supervision) were clearly stated. Thereafter, provisions concerning internal controls were established under each related laws such as the Company Law, and from 2001 onwards, the Internal Accounting Control Code was published from the Finance Bureau one by one, and the basic framework of internal control has been established.However, following the publication of the Internal Accounting Control Code, due to frequent false accounting and misconduct at the securities market, in 2006, the Securities Regulatory Commission adopted the "Regulations on Issuance and Listing Management" On the other hand, the Shanghai Stock Exchange and the Shenzhen Securities Exchange also announced the internal control guidelines of the listed company, and this rule came into effect in 2007.Furthermore, the Finance Bureau, the Securities Regulatory Commission, and other committees jointly strengthened provisions on internal control of the company, and the following efforts are made to contribute to the development of a fair securities market.

2006 Company Internal Control Committee established2008 Corporate Internal Control Basic Code promulgated (enforced in 2009)Prompted issuance guidelines for corporate internal control in 2010 (enforced in 2011)

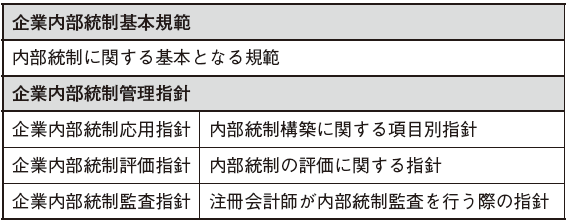

The Chinese version SOX law refers to the company's internal control basic norms and the company internal control management guidelines.The internal company's internal control of the Chinese formed in this way was established based on the internal control framework of the American Treadway Committee Organizing Committee (COSO), similar to the US corporate reform method (SOX law) Therefore, it is called Chinese version SOX Act or C (China) -SOX.

The main norms concerning corporate internal control are as follows.

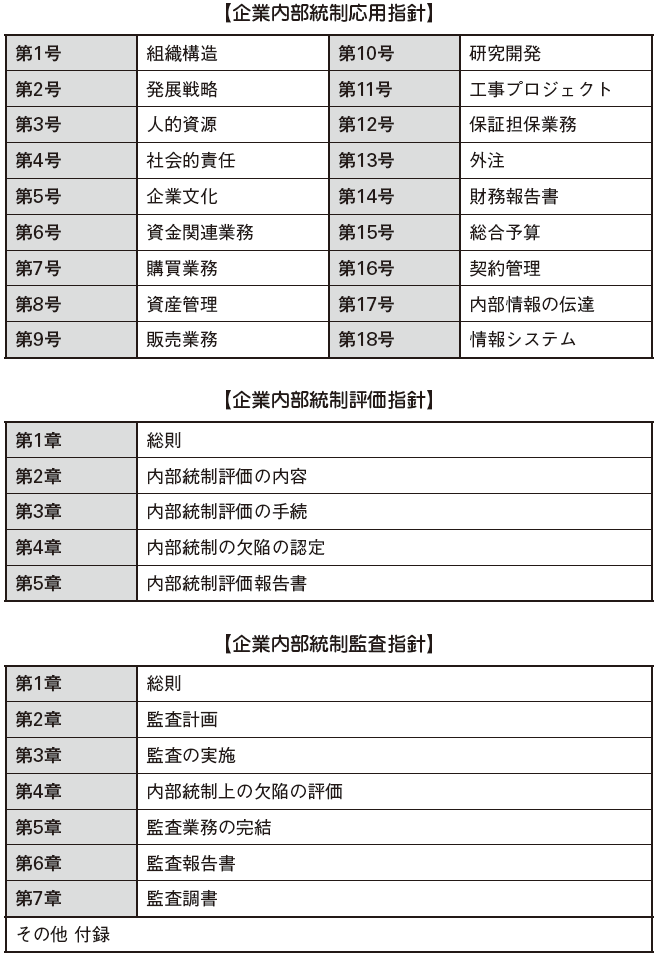

[Corporate Internal Control Basic Code]It describes the basic matters such as the definition and scope of internal control that companies should observe. It consists of all seven chapters of Article 50. Below, I will describe the contents of the internal control.

significanceInternal control is a process that is implemented by the company's Kaoru Kai, the board of directors, the senior management and all employees and aims to achieve the control objectives. Its objective is to strengthen and standardize corporate internal controls, enhance corporate management level and risk prevention capability, promote sustainable development of enterprises, protect socialist market economy and the interests of society masses It is in that.

rangeAlthough it is enforced for listed companies, it is also recommended to apply to large and medium size companies (it can also be applied to small companies). Internal control companies need to periodically evaluate the effectiveness of internal control in accordance with the situation of internal supervision and to prepare their reports.

Control targetWe aim to guarantee the truth and completeness of compliance of corporate management control, asset preservation, financial reporting and related information, improve management efficiency and effect, realize the company's development strategy.

Basic componentInternal environment, risk assessment, control activities, information and communication, internal supervision.

Regarding whether or not to provide internal control audit work and consulting work at the same time, in Article 10 of the Basic Code of Internal Control for Internal Control,Accounting professional office providing salting service should not provide internal control audit services to the same company at the same time ". Since the internal control audit needs to maintain independence and consulting work may hinder its independence, simultaneous provision of both work is prohibited.

[Corporate Internal Control Management Guidelines]Corporate internal control management guidelines consist of corporate internal control application guidelines, corporate internal control evaluation guidelines, and corporate internal control audit guidelines. For each guideline, there are descriptions concerning the construction of items by internal control items, guidelines when internal organizations such as the Kura Kai or the like evaluate internal control of the company, and note on guidelines for accounting auditors to conduct internal control audits.

In addition, the following points are noteworthy regarding the corporate internal control management guidelines.

Standard date of internal control evaluation reportIt is necessary to submit December 31 as the base date within 4 months after the base date (Corporate Internal Control Evaluation Guideline Article 26).

Outsourcing of internal control evaluationA listed company in China needs to prepare a self-assessment report for fiscal year concerning the evaluation of the effectiveness of its internal control. However, regarding the effectiveness of the report, it is stated that evaluation can be entrusted to accounting professors and others. Also, it is prohibited accounting practitioner to audit the internal control to the same company (Article 14 of the internal control evaluation guidelines).

Note Integrated implementation of audits of financial statements and internal control audits by accounting professionalsEven in China, it is possible to carry out audits of financial statements and internal control audits as a unit from the viewpoint of the effectiveness and efficiency of audits. The point that it may be carried out alone is in contrast to the United States and Japan.

Audit method, objectNote Accountant's internal control audit is conducted by top-down approach, and direct opinions are expressed for internal control itself. The deficiency classification of internal control evaluation is divided into three stages of serious defects, important defects, general defects (Article 4 of the Internal Controls Evaluation Guidelines).

These features are based on the guidelines on internal corporate internal controls in China based on the US SOX Act, COSO report, etc., but the practical burden is large, the theory and practice are divergent Is the current situation.

-