Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaSingapore

9 Chapter Tax

-

-

Overview

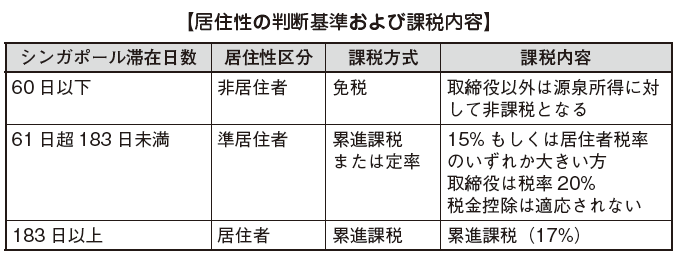

In Singapore, the place of residence is determined according to an administrative dominance.

A company established in accordance with the Company Law in Singapore is treated as a resident corporation even for foreign capital such as Japan. However, regardless of whether it was established based on the Corporate Law of Singapore, if a general meeting of shareholders and board of directors are held in countries other than Singapore and the operation & management of business execution are being conducted, the Singapore tax law Above, it becomes a non-resident corporation.

In Singapore's tax system, residents are given preferential treatment and non-residents are not subject to the tax exemption for the new company, tax exemption for foreign source income, and reduction or withholding tax etc. are all based on the double tax avoidance treaty. Residents' judgment is made in each taxable year.

■Taxable year

In Singapore, the tax year for corporate income tax is in the principle of standard for the fiscal year. -

Calculation of taxable income

Taxable income in the revenue law is generally calculated by deducting all deductions from all gross profits related to businesses that were operated in one accounting period (usually the business year). The business year is assumed to be 12 months in principle.

In addition, gains and losses are calculated based on the accrual principle. All gains and losses incurred during the business year are included in the transfer, and deductible expenses are included in the calculation of the income amount regardless of whether or not payment is made.

■ Taxable gains

Singapore's corporate income tax is calculated by territorial system. In other words, income from Singapore source or Singapore foreign source income will be subject to taxation in Singapore. Personal income tax is also calculated by territoriality.

· Gains and benefits earned from the business

· Dividend, interest, and rent

· Royalty Profit earned from other assets

· Gains and benefits other than those mentioned above with the nature of income

However, the following profit is exceptionally subject to tax exemption.

· Gain on sale of fixed assets

· Foreign Exchange Margin by Capital Transaction

■Deduction calculation

In Singapore, in calculating taxable income, taxable income is calculated by adding or subtracting adjustment items from accounting profit like Japan. However, whereas in Japan there are provisions that allow deductibility as a requirement for deductibility accounting like depreciation and amortization. The Singapore income tax law does not prescribe the independent accounting treatment of the tax law, and the proper opinion of the certified public accountant and also the accounting treatment of the financial statements with the attached items were considered to be appropriate under the tax law as well.

Moreover, from the draft budget for 2013, they will be able to receive a cash grant of up to 15,000 dollars in the total for the three years from 2013 to 2015, so that the deduction of traditional productivity and innovation PIC: Productivity and Innovation Credit). The target areas are as follows.

· Acquisition or lease of PIC approved automation equipment

· Empowering employees' training capacity

· Registration of intellectual property rights

· Acquisition of Intellectual Property Rights, Design

· Research and development activities

· Invest in design project

With small businesses in mind, they will refund cash of up to 60 thousand dollars for PIC target investment of 100 thousand dollars annually in the 2011 to 2012 tax year, and 100 thousand dollars annually for 2013 to 2015 tax years that has been established a mechanism.

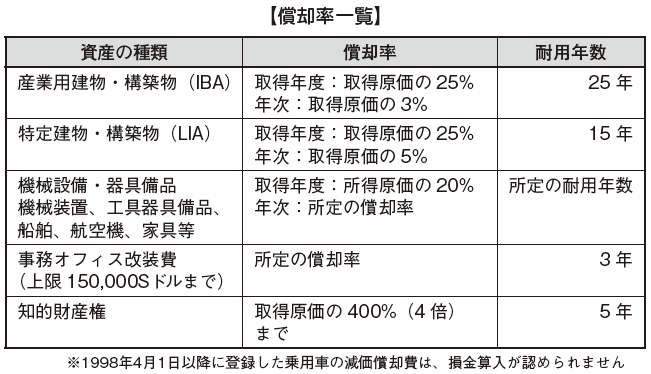

[Calculation of Depreciation Expenses]

In Singapore, depreciation expense is calculated accounting as symbolized by capital gains tax exemption but tax deduction is not allowed for tax purposes. This is because it is not allowed to include deduction of expenditure related to capital items in principle. As a general rule, accounting depreciation expenses are added to taxable income in full and the tax depreciation expenses are calculated again and subtracted from taxable income.

Method of depreciation

Since the method of depreciation is not stipulated in the Internal Revenue Code, basically follow the tax depreciation method. If you do not do the first year's amortization at the time of acquisition, you cannot write off from the following fiscal year. Also, if you do not do depreciation on the way, it is not permitted to include deductible sums in the past when amortizing again.

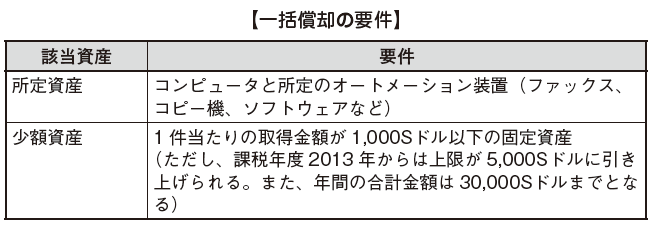

Depreciation rate Acquisition year lump-sum depreciationAssets that fall under the following conditions are allowed to be amortized in bulk during the acquisition year.

Acquisition year lump-sum depreciationAssets that fall under the following conditions are allowed to be amortized in bulk during the acquisition year.

Acceleration depreciation

Assets are classified as newly purchased machinery and equipment. They are permitted to be fully amortized using the straight-line method with a useful life of 3 years, and this is called Acceleration Amortization.

Earnings’ expenses before opening

Relevant expenses are incurred during the first income year can be included in deductible expenses. Also, from the 2012 tax year, in addition to the year in which the first income occurred, expenses that occurred in the previous fiscal year can also be included in deductible expenses.

R & D expenses

Research content that falls under R & D expenses means that the results of scientific or technical R & D that can lead to productivity and product quality improvement can be included in deductible expenses. This does not apply to data collection and questionnaire surveys that are regularly conducted, echo surveys and market research of sales advertisements, or software development that is not intended for sale. Mainly, it is the criteria whether there is innovative creativity that does not exist in a new product development or in Singapore.

Automobile related expenses

In general, the expenses of rental cars used in Singapore are not allowed to include deductions even if they are intended for business purposes. However, for rent-a-car expenses outside the country, deduction is allowed if it is for business purposes. In addition, depreciation expenses of passenger cars required by the company for business are permitted.

Entertainment expenses

In Singapore, there is no clear provision for classifying necessary expenses, all expenses necessary for business activities are allowed to be deducted. However, private expenses such as private dining expenses accompanying the family are considered non-deductible.

Provision of allowance for doubtful accounts

Regarding provision allowances, in principle, they are not included in the amount of deductible expenses. However, the provision for doubtful accounts is the amount that can confirm the certainty of defaults is included in the amount of deductible expenses. Therefore, preparation of appropriate evidence based on the following points is indispensable for inclusion of deductible.

· Name and address of obligor

· Date on which the claim occurred, its nature

· Amount of money that cannot be collected

· Reserve processing, reasons for bad debt treatment

· Processes taken during collection

Donation

Deduction is only allowed for donations made to specific organizations recognized by the Government and Charity Committee and performing only philanthropic activities.

Start-up cost

Since opening fees are not expenses for earning income, it is not generally permitted to include deductions. However, as policy preferential treatment, the inclusion of deduction for opening fee incurred in the same tax year as the year in which sales were recorded is permitted. -

Types and classification of taxable income

■ Taxable Income

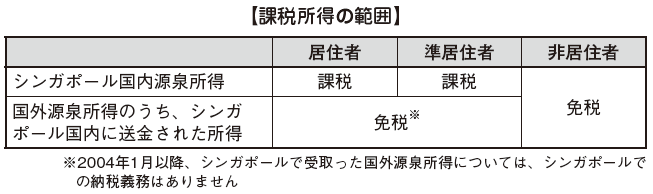

Taxpayer of corporate income tax in Singapore is supposed to be operated in Singapore within a corporation / association established in Singapore and a corporation / association established by foreign law, and these are called genus land ownership, Singapore domestic income and overseas income, which becomes an income in Singapore is subject to taxation.

Taxable income in Singapore are as follows.

· Income incurred in Singapore

· Income received in Singapore out of foreign source income

■ Foreign source income

Of the foreign source income, the income received in Singapore is regarded as source income earned in Singapore and subject to taxation. However, of foreign source income that is remitted to Singapore, income for which dividends and branch income and service income are taxed for income tax of 15% or more in that country in foreign countries is taxed in Singapore not.

Also, even if you are not engaged in Singapore domestic business, foreign companies are subject to taxation in Singapore if they conduct business at permanent facilities and are subject to withholding tax provisions.

■ Types of taxable income

Since Singapore's income tax law is targeted at corporations and individuals, there is no clear provision for corporate taxation standards. Therefore, in Japan's income tax law, the income is prescribed for each type, and these methods are combined to form taxable income. The income is as follows.

· Business income

· Income arising from employment

· Investment income (dividends, interest or discounts)

· Pension

· Asset income (income arising from assets such as rent, usage fee etc.)

· Gain or profit with other income characteristics -

Corporate income tax rate

A tax rate of 17% is applied from 2010 taxable year.

■ Income Tax Reduction

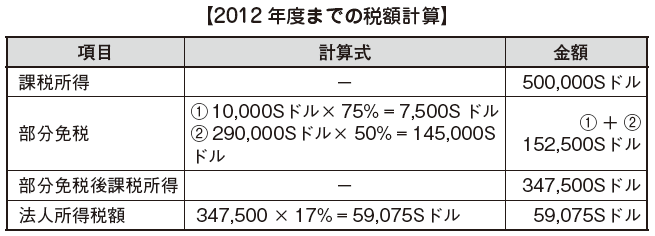

Singapore's corporate income tax rate of 17% has been applied, but Partial Tax Exemption has been adopted as before, and 75% of the taxable income up to the 10,000 S dollar is 75%, 10,000 About 2 90,000 S dollars, 50% is tax free.

In addition, a tax incentive system is introduced to newly established companies from the 2005 taxable year. Three years from the establishment, 100% of the normal taxable income of 100,000 S dollars in the first year and 50% of the 200 thousand dollars in the next fiscal year will be tax exempted. From the 2010 tax year, limited liability guarantee companies will be included in the tax exemption measures applied to the new company.

Furthermore, it was announced that a new tax reduction will be applied to all corporations from the 2013 tax year to the 2015 tax year in the 2013 budget draft issued by the Singapore Ministry of Finance. The tax reduction amount is 30% of the corporate income tax amount and the upper limit is 30 thousand dollars for each year. This tax reduction is also effective for corporations that have already applied the reduced tax rates.

■ Tax calculation

Assuming taxable income to be 500,000 S as a result of the tax reduction measures, the effective tax rate up to 2001 was about 1.8%, but from the fiscal year 2001 it is about 8.3%, which is even lower It becomes a tax rate.

■ Preferred tax system for regional headquarters

A preferential tax system will be applied to companies that meet certain conditions and active in Singapore as regional headquarters. If you were recognized as a Regional Headquarters, the tax rate is 15% or less, and if they are approved as the International Headquarters, the tax rate is 10% or less.

-

Declaration and Payment Procedures

■ Tax return

The planned tax payment is made after the closing date by submitting Estimated Chargeable Income (ECI) and Estimated tax payment to IRAS. After that, they will finalize the corporate income tax amount by submitting the corporate income tax return form (Form C) and pay the difference with the planned tax payment amount.

[Tax payment]

All companies must file an ECI and estimated tax payment amount for the relevant business year to IRAS within three months from the last day of the business year.

After the submission of ECI, a notice of assessment (NOA) will be send from IRAS in several months. Because NOA will be send from authorities as forecast based on revenue from taxable period, if there is a difference from income tax amount determined later, it will be the flow of adjustment.

In addition, if the annual profit is less than S $ 10,000, declaration of ECI is unnecessary.

Declaration deadline

Every year, a Form C will be send from IRAS in April. 1 They have to submit the Form C after attaching audited settlement statement and an income tax statement (Tax Computation) by January 30. In addition, if the Form C was not send by April 30, it must be downloaded from the tax authority's website or asked to send tax returns to tax authorities.

[Tax on corporate income tax]

A few months after submitting Form C, NOA should be send. Payment or refund of the difference between the planned tax payment amount and the corporate income tax amount are made, and in the case of payment, the difference must be paid within 30 days from the issue date of NOA..png)

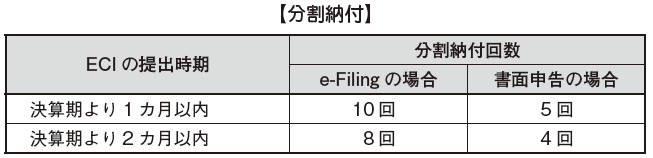

[Partial payment]

With the approval of the tax authorities, payment of corporate income tax can be paid in bulk or up to 10 times. The number of permitted split payments depends on the timing of ECI submission. Because they are promoting e-Filing, dividing payment by e-Filing is allowed more times than written of declaration. However, if ECI is submitted after 3 months from the fiscal year, split payment will not be accepted.

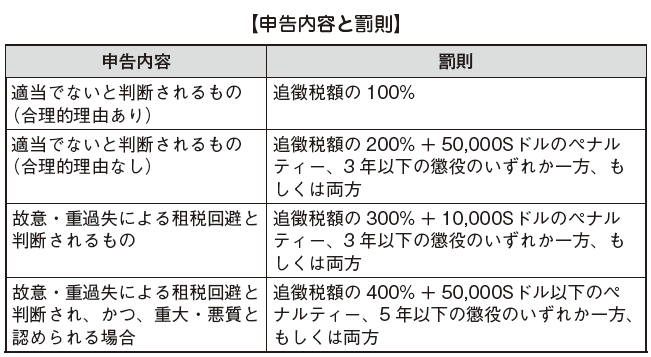

■ Penal Provisions

Contents of penalties differs between cases where it is determined by the Internal Revenue Service that the declaration content is not appropriate and cases where it is judged to be avoidance of tax due to willful or gross negligence. Declaration contents and penalties are as follows.

[Delay]

The payment deadline is within 30 days from the issue date of NOA if they do not use the split tax payment system. If they do not pay by the payment deadline, a delayed tax equivalent to 5% of the tax amount to be paid is charged. If the delay continues after 30 days, a dunning letter will be issued, and if you are delinquent after 60 days from the stated date, the 1% delinquent tax will be added every month. However, the total overdue tax will not exceed 12%. If delinquency continues, IRAS is permitted to take legal measures.

-

.png)

.png)

.png)