Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaSingapore

8 Chapter Tax Risk of Regional Headquarters

-

-

1 Chapter Importance of Management by Regional Headquarters

1.1 Importance of Asian market

1.2 Regional management of the Asian market

1.3 Comparison of countries as headquarters

2 Chapter Regional Headquarters System and Utilization Examples

3 Chapter How to Utilize Regional Headquarters

3.1 Method of Consolidating Profit by Dividend and Making it as Reinvestment Base

3.2 Utilization as a Finance Company (Loan Function)

3.3 Example of Utilization of Efficiency by Consolidating Settlement Functions

3.4 Example of Reviewing Supply Chain Functions and Risks

4 Chapter How to Make Regional Headquarters

4.1 How to Set Up a Regional Headquarters

4.2 Singapore as a Business Base

4.3 Corporate Law in Singapore

5 Chapter Overseas Relocation of Head Office Functions

5.1 Head office relocation to low tax rate country

6 Chapter M&A

6.1 Trends in M & A in Singapore

6.2 Points to keep in mind when doing M & A

6.3 Laws and regulations concerning M & A

6.7 Investment regulatory environment of Singapore

7 Chapter Accounting

7.1 Accounting System in Singapore

7.2 Accounting Standard in Singapore

7.3 Disclosure System in Singapore

7.4 Accounting Audit in Singapore

8 Chapter Tax Risk of Regional Headquarters

8.1 Tax · Haven Countermeasure Tax System

8.2 Foreign Subsidiary Dividend Income Non-inclusion System

8.5 Taxation of Country of Residence and Double Taxation by Source Taxation

8.6 Tenuous Capital Tax System

9 Chapter Tax

9.2 Personal income tax in Singapore

9.3 Corporate income tax in Singapore

9.6 Singapore withholding system

9.7 International tax in Singapore

10 Chapter Labor

10.1 Work environment in Singapore

10.3 Social Security System in Singapore

10.4 Points to keep in bringing Japanese to Singapore

11 Chapter Q&A

-

-

-

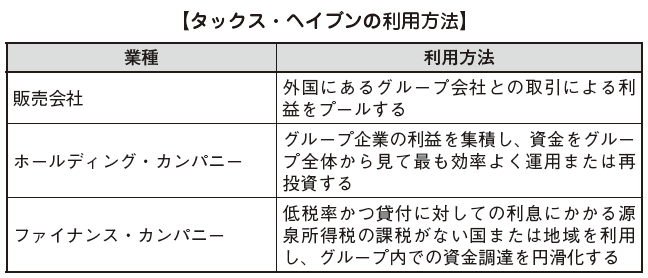

Tax · Haven countermeasure tax system

■ Tax · Haven (low tax rate country)

Tax Haven (Tax Haven) is a country or region where certain taxes are taxed at a very low rate or not at all. The Cayman Islands, Bermuda, Luxembourg, Cyprus, Belize, Singapore, Hong Kong, etc. are called tax havens (low tax rate countries), and by greatly enjoying the benefits of taxation by concentrating the profits in these countries. It is possible.

Generally, tax havens are classified as follows;

[Tax Paradise (Tax Paradise)]

Taxes on income does exist at all, or countries or regions close to it. (e.g. Bahamas, Bermuda, Cayman Islands etc.)

[Tax Shelter]

Regarding domestic income, we made regular taxation, but for overseas source income it is a country or region that taxes with tax exemption or extremely low tax rate. (e.g. Panama, Liberia etc.)

[Tax Resort]

A country or region that gives tax benefits to specific business activities only. (e.g. Netherlands, Switzerland, Luxembourg etc.)

When investing abroad, there are also cases where management established by making a company established overseas through the headquarters (HQ: Headquarters) rather than direct investment from Japan. By establishing a central office in Tax Haven, it is possible to retain the benefits aggregated from each subsidiary by making maximum use of the merit of the tax system.

However, if the HQ is approved by the tax authorities as a 'paper company without actual' on the Japanese side, the income retained by HQ is added to the income of the Japanese side and the corporation tax in Japan is taxed. It will be. This is called "tax-haven countermeasure tax system" and it is a system aimed at preventing tax evasion through subsidiaries and affiliates located in Tax Haven. It is necessary to carefully consider income collected in the regional headquarters established in the low tax rate country so as not to be subject to the tax and haven countermeasure tax system.

■ Criteria for judgment by tax · haven

According to the Organization for Economic Cooperation and Development (OECD), the elements for judging whether or not the relevant jurisdiction falls under a tax haven are listed as follows.

[Free or very low tax rate]

In Tax Haven it is taxed at a very low tax rate under normal or special circumstances. It is considered to actually provide a place to use for tax avoidance for non-residents who’s trying to escape from the high tax of the resident country.

[Protection of personal financial information]

Tax Haven usually provides laws and administration to protect individuals and companies from detailed investigation by tax authorities of other countries. This information prevents on taxpayers who are benefiting from low tax rates from being leaked out.

[Lack of Transparency]

The lack of transparency in legislation, law, and the administration of administrative regulations is an element that shows tax havens.

The OECD says, "The law is made public, its application should be consistent, and overseas tax authorities should be able to obtain the information necessary to judge the situation of taxpayers." The lack of transparency of the law in a country makes it difficult for foreign tax authorities to apply the law efficiently. Confidentiality provisions, intentional low tax rates, customs without consistent law application are examples of lack of transparency.

Therefore, tax haven regulates the establishment of overseas holding company in low tax rate country for Japanese companies who tries to avoid taxes.

■ Outline of Tax / Haven countermeasure tax system

When a domestic corporation has a specified foreign subsidiary company (e.g. a foreign affiliated company located in a low tax rate country), the tax / anti-haven countermeasure tax system stipulated in the Japanese Corporate Tax Law (foreign subsidiary combined tax system). This is a system that considers the amount of the corresponding portion to the ownership ratio of the subsidiary company held by the domestic corporation among the profits retained by the subsidiary company, as the income of the domestic corporation, and intends to sum the taxes in Japan..png)

In other words, although it is not recognized as "profit" in accounting in Japan, it is taxed together in Japan on the retained earnings abroad by recognizing it as "profitable" for tax purposes.

There is no tax system in Singapore or Hong Kong that falls under Japan's tax and haven countermeasure tax system.

Companies that are subject to this taxation system are those who reside in Japan or in domestic corporations directly or indirectly by more than 50% of their shares (using a method to calculate excluding voting rights, shares without the right to distribute dividends) Companies that exist in countries or regions where there is no tax on corporate income at a foreign subsidiary that is owned or whose tax rate is 20% or less are eligible.

Among them, if a domestic corporation or a resident who directly or indirectly holds shares of a specified foreign company by 10% or more, the retained income amount of the foreign subsidiary will be subject to the same taxation system. In other words, a company that is located in Tax Haven, owns more than 10% of its shares in the same family, and a company with more than 50% of its capital is Japanese capital.

However, not all companies that meet the above requirement are subject to taxation, but in order to avoid hindrance to corporate normal overseas investment business activities by conducting a combined taxation, the exclusion criteria is set up.

■ Exclusion from Application of Tax / Haven Taxation System

In certain cases where a specified foreign subsidiary or the like has an entity as an independent company and it is deemed that there is sufficient economic rationality to conduct business activities in the country where it is located, it is considered that tax avoidance is not the purpose, the tax system does not apply.

[Application exclusion criteria]

Business criteria: Main business is not the following;

- Holding of shares and receivables (pure holding company)

- Industrial property rights, rights related to other technologies, production methods based on special techniques or equivalent, or provision of copyright

- Ship / aircraft lending (leasing industry)

· Entity standard: To have offices, shops, factories and other fixed facilities necessary for the main business in the country where the head office is located

· Management control standards: To manage, control and operate the projects themselves in the country where the head office is located (General shareholders meetings and board meetings are held in the country where the officer's duties are executed, preparation and storage of accounting books etc.., must be carried out)

· Unrelated party criteria: If you operate a wholesale business, a banking business, a trust business, securities business, insurance business, water transportation business, air transportation business, more than 50% of transactions are done with non-related persons

· Country criteria of location: In the case of industries (manufacturing industry etc.) other than those that do not meet non-affiliated person standards, they are mainly engaged in business in the country or region where the head office or main office is located

[Being a controlling company]

A specified foreign subsidiary company or the like that meets the following requirements falls under category 3 9 (1) 7.

· It is a specified foreign subsidiary, pertaining to a domestic corporation and all of the issued shares are directly or indirectly owned by the domestic corporation.

· Having two or more controlled companies and conducting certain tasks to oversee the business of the managed company.

· Having fixed facilities related to supervising operations * in the country where they are located and those who are required to conduct supervisory operations (exclusively engaged in supervisory work, excluding officials of the specified foreign subsidiary etc.)

* Administrative work refers to operations that contribute to the improvement of profitability through comprehensive management or adjustment of business activities of the managed company by the controlling company (Article 66 (6) (3))

[Being a controlled company]

Foreign corporations that fulfill the following requirements (Applicable Article 3 9, paragraph 1, 2, 5, 6).

· A person who directly owns 25% or more of outstanding shares and who directly owns 25% or more of the voting rights (related persons in the non-affiliated person's standards, limited to foreign corporations, domestic corporations Etc., excluding related persons related to family related persons)

· Having a worker recognized as necessary for doing business in a country of residence

· It is a foreign corporation that is a subsidiary company, a sub-subsidiary company, a sub-minor company, and is "controlled" by a domestic corporation related to the controlling company and the controlling company

As a result of the reform of the tax system, substantial overseas holding companies are excluded from the combined taxation, making it easier for global development using the overseas holding company, which is a regional headquarters. In addition, it is thought that the tax saving effect of the whole group has increased.

1.0.5 Calculation of tax burden ratio

The tax burden ratio is calculated as follows.

Because Singapore or Hong Kong has a corporate tax rate of 20% or less, even if income is retained by establishing an overseas holding company, which is a regional headquarters company, the combined taxation of Japanese corporate tax rate (effective tax rate of approximately 35.64%) We will not receive the benefits of low tax rates. The corporate tax rate in Thailand is 20% (applicable from FY 2013), but if you receive the preferential taxation system of the regional headquarters, it will be reduced to 10%, so there is a possibility that the combined taxation will be done in the same way.

However, even if the tax burden ratio is 20% or less, if the tax exemption criteria are satisfied, such as having an entity as an independent company and being deemed to have sufficient rationality for doing business in that country, it does not apply.

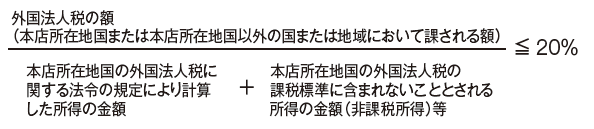

■ Definition of Specified Foreign Subsidiary Company

Tax / Haven Countermeasures Taxpayer obliged persons to whom shares, etc. of 10% or more of the total number or total of the issued shares or investments (excluding treasury shares etc.) of "specified foreign subsidiaries etc.", directly or indirectly, It is a domestic corporation belonging to the shareholder group (Article 66, paragraph 6, item 1 of the Act).

[Specified Foreign Subsidiary Company]

Definitions of specified foreign subsidiaries etc. are as follows;

· Foreign corporations (foreign affiliates) directly or indirectly holding shares or investments exceeding 50% of the total number of issued shares or total investment by Japanese residents, domestic corporations and special relationship nonresidents,

· Of foreign affiliated companies, tax burden ratio is 20% or less.png)

20% of the tax burden ratio, which is the criterion for judging whether it falls under "tax-haven countermeasures taxation system" or not, is not the surface tax rate stipulated by the tax law, it is judged by the burden ratio of corporate tax (effective tax rate).

Therefore, even a single foreign affiliated company may be a certain foreign subsidiary company in a certain business year and may not fall under a specified foreign subsidiary company in another business year.

■ Taxation on asset income

Even if the requirements for exemption from tax havens are met, if a specified foreign subsidiary or the like has certain fixed asset management income (hereinafter referred to as "asset income"), The portion corresponding to the share of the shares of the specified foreign subsidiary held by the domestic corporation will be subject to the tax and haven countermeasure tax system.

The taxation system of the asset income is originally operated in the home country. Asset income which is supposed to be taxed in the home country is set up to prevent taxable objects from leaking out in the home country by being operated and taxed in the low tax rate country in order to reduce tax burden.

The income subject to taxable income tax is as follows;

· Income related to dividends of shares with holding ratio of less than 10% or income from transfer

· Income related to interest on bonds or income from transfer

· Income from industrial property rights and copyright (including publishing rights and neighboring rights)

· Income from lending of ships or aircraft

In calculating the asset income, you can deduct the expenses that are deemed directly necessary to earn income. For stock dividends · bond interests, you can deduct the amount corresponding to the earning period of the interest expense.

In addition, if the total amount of asset income of specified foreign subsidiaries etc. is less than or equal to 5% of the pretax income of the company etc., or the total amount of income on asset income is 10 million yen or less, In that case the provisions does not apply.

In addition, due to the nature of the projects performed by specified foreign subsidiaries, income related to stocks and bonds arising from basic and important and indispensable operations can be excluded from calculation.

-

-

-

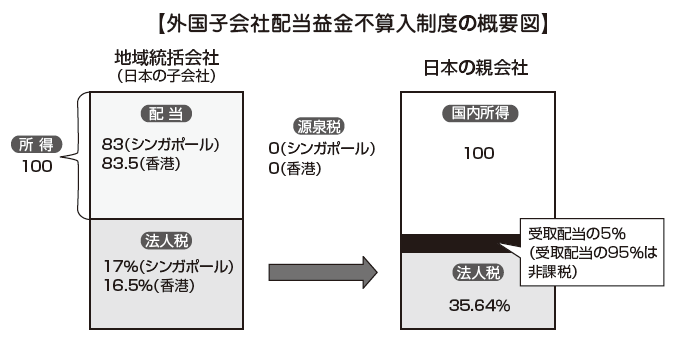

Foreign subsidiary dividend income non-inclusion system

■Introduction of foreign subsidiary dividend income non-inclusion system

In the past, by using overseas holding companies, etc., the income taxed at a low tax rate was retained and reinvested in the form of investment or lending in foreign subsidiaries of other countries without refunding to income in Japan.

95% of the dividend will be tax exempt (exemption from Japanese income tax) if the Japanese parent company receives dividends from overseas holding company, which is a regional headquarters that satisfies certain conditions, by introducing a foreign subsidiary dividend profit margin non-inclusion system , Japanese corporate tax (about 3 5.6 4%) will be imposed on 5% of the dividend amount.

As a result, the total tax burden will be greatly reduced in funds refunding from countries with low corporate tax rates such as Singapore and Hong Kong.

Foreign subsidiary dividend income tax exclusion system has the benefit of alleviating obstacles when funds are refunded to Japan and increasing the degree of freedom of building an international taxation strategy.

However, direct foreign tax credits on interests other than withholding income tax, withholding tax on royalties, on local branch offices of foreign corporations, etc., imposed on non-profitable dividends will continue to be applied as before.

-

-

-

Overview

There is a dividend as a representative way to return profits from the regional headquarters to the parent company in Japan. Transaction consideration such as royalty may be paid to the parent company in Japan.

When a company deals with an overseas affiliate, by increasing or decreasing the setting of the transaction price (transfer price), it becomes possible to transfer the profit of the company in one country to the company in the other country.

Transaction price (transfer price) between foreign affiliated companies was established with non-affiliated companies if arbitrarily decides the transaction price between affiliates for the purpose of transferring profits to low tax rate countries The transfer pricing taxation system is a system that requires taxpayer to calculate taxable income as it did at 'inter-industrial enterprise price'.

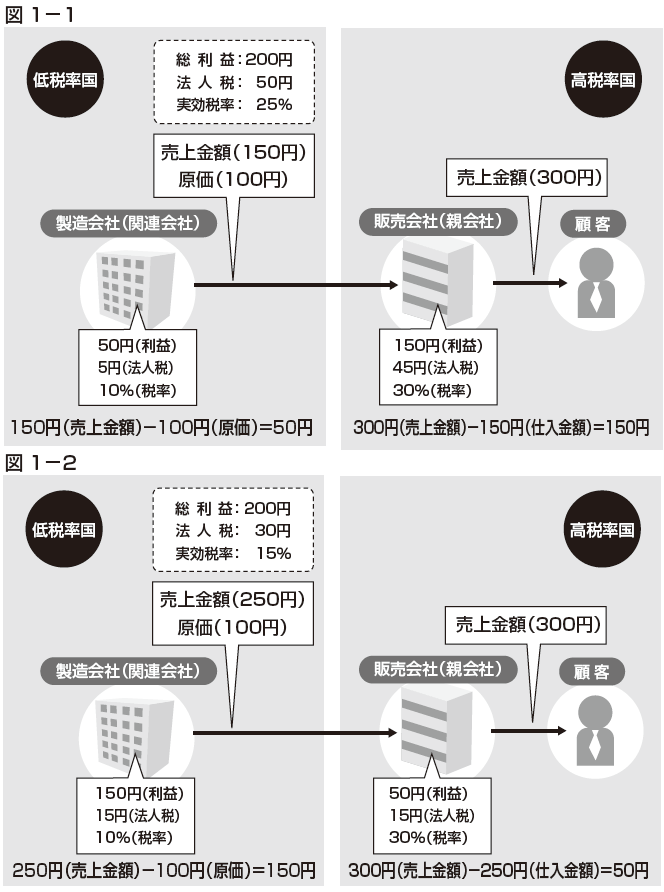

■ Transfer of profit by adjustment of transaction price (transfer price)

Regarding on the pricing of transactions, it is a major principle under the free trading market that can be entrusted to the free will of the enterprise, but by adjusting the transaction price within the corporate group, the tax burden of the entire group is reduced as a result It will be possible.

【Transfer of profit by adjustment of transaction price (transfer price)】

In Figure 1-1 above, a sales company (parent company) in a high tax rate country purchases a product (cost 100 yen) from a manufacturing company (affiliated company) in a low tax rate country for 150 yen and sold it to customers for 300 yen, The profits of the sales company (parent company) and the manufacturing company (affiliated company) are 150 yen and 50 yen, respectively, which means that many profits are taxed in high tax rate countries.

In the case of Figure 1-2, a sales company (parent company) in a high tax rate country purchases a product (cost 100 yen) from a manufacturing company (affiliated company) in a low tax rate country for 250 yen and sells it to customers at 300 yen If you do, the profit of the selling company (parent company) and the manufacturing company (affiliated company) is 50 yen and 150 yen respectively, and many profits are taxed in the low tax rate country.

■ Application target of transfer pricing taxation

As royalty payments become subject to transfer pricing taxation and these are transactions of intangible assets, it is practically difficult to calculate royalty prices among independent companies. Many of the disposition from the tax authorities are said to be intangible asset transactions and are considered to be very risky transactions.

The transaction to which the transfer pricing taxation is applied in Japan is the transaction of assets which the corporation carries out with foreign affiliated persons, the provision of services, and other transactions (overseas related transactions), and capital transactions (investment, dividends) All transactions excluded are subject.

A foreign affiliated person is a foreign corporation in a "special relationship" with a corporation, and the following two are based on the judgment of "special relationship".

[Capital ties]

Refers to a relationship in which one corporation directly or indirectly holds 50% or more shares, of issued shares of the other corporation, and when the corporation owns 50% or more shares etc. of each outstanding shares by the same person is directly or indirectly held.

[Substantial Relationship]

The existence of specific facts is a relationship in which one corporation can substantially decide the whole or a part of the business policy of the other corporation. The following are examples of specific facts (Action 3 Article 9, 1, 3, 12, and Measures Law Notice 66: 4 (1) -3).

· One-half or more of officers of the other corporation or officers having representation right con-currently serve as officers or employees of one corporation, or once an officer or employee of one corporation

· The other corporation makes a substantial part of its business activities dependent on the transaction with that one corporation

· The other corporation has borrowed a substantial portion of the funds required for its business activities from one corporation or that it is procured under the guarantee of one corporation

· The copyright (the right of publication and neighboring rights and other equivalent), the industrial property right (patent right, utility model right, design right and right), which is the basis of business activities provided by one corporation to the other corporation. We refer to trademark right), knowing how to do business activities depending on know-how etc.

· There is a fact that it is recognized that more than a half of officers of one corporation or officers who have representation rights are substantially determined by the other corporation

3.1.3 Calculation of Independent Intercompany Price

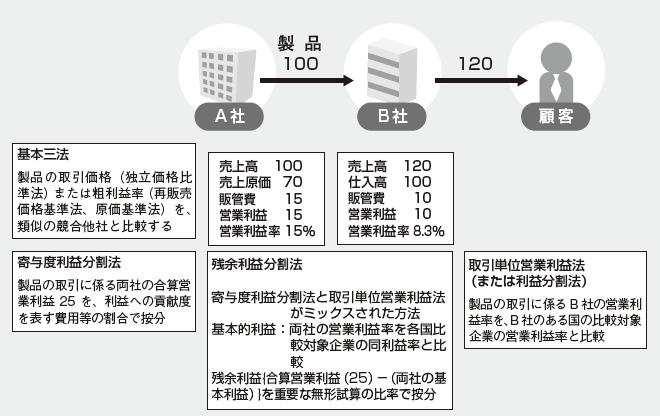

The method of calculating inter-independent enterprise price is decided by considering transaction details / form from several methods. Generally, the following calculation method is used.

[Independent price comparison method]

The CUP (Comparative Uncontrolled Price Method) is a method of comparing the amount of consideration for transactions made in non-related parties (third party transaction) under almost the same conditions as those of foreign affiliated transactions, its independent company-to-company price and way. In the case where the transactions to be compared are sales of goods etc., it may be difficult to compare because the transaction conditions change due to the business strategy and market conditions. As a result, this method is often used for interest rate transactions with little fluctuations in terms of transactions and for commodity transactions with quotes, and it is not widely adopted for ordinary goods transactions.

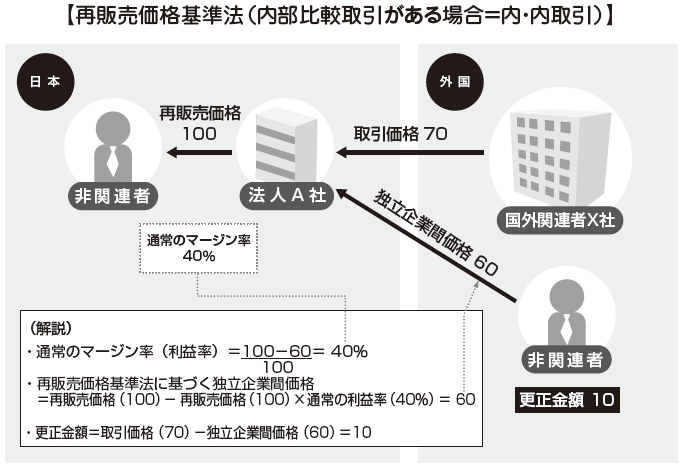

[Resale Price Standard Law]

The Resale Price Method (RP method) is a method in which an intercompany price is determined by subtracting the amount of profits that would normally be obtained from the transaction from the resale price to a third party. This method is often used when overseas related transactions are import transactions (especially in the case of import transactions, since data to be compared is published in many cases).

The cost method (CP method: Cost Plus Method) is calculated by adding to the amount of costs incurred by targeted foreign affiliated transactions, adding the amount of profit that the other corporation would normally obtain from the transaction It is a method to make the amount made as independent company price. The normal profit in this case is calculated by multiplying the cost of the product by the normal profit margin (gross profit margin / cost).

In the case that costs are included in manufacturing costs, we will calculate the cost of manufacturing related parts based on the price in the case of transactions between third parties. (e.g. if you purchase raw materials from related persons, you will calculate the manufacturing cost by replacing the purchase price of that raw material with the price you purchased from a third party.)

This method is adopted for raw material processing / export, service provision transaction, etc.

[Profit division method]

The Profit Split Method (PS method) is a method of allocating the total amount of operating income realized by overseas related transactions according to the extent contributing to its realization, and there are the following methods;

Contribution profit division method

How to allocate the total amount of operating income according to the amount of expenses spent, the value of fixed assets used, and other contribution to operating profit

Comparative profit division method

Method using a dividing ratio of profit in non-related party transactions conducted under similar circumstances as overseas related transactions

[Residual profit division method]

The Residual Profit Split Method (RPS: Residual Profit Split Method) is used when a corporation related to transactions and overseas related persons have significant intangible assets. In transactions that do not take into consideration important intangible assets of the total profits, we allocate amounts equivalent to the profits that would normally be obtained, and the value of the significant intangible assets each of which has the remaining amounts (intangible assets The cost of the development etc., etc.) is allocated according to;

[Transaction unit operating profit method]

The transaction unit operating profit method (TNMM: Transactional Net Margin Method) is a method based on gross profit margin, operating profit margin, markup rate, etc. realized by transactions with third parties, It is a method to calculate the transaction amount compared with those.

■ Selection of calculation method of independent intercompany price

In calculating the independent company price, the company side will select the calculation method according to the transaction type, but in general, the calculation method corresponding to the next transaction classification is used.

[Sales of inventory (products etc.)]

Independent Price Compensation Substitution Law, Resale Price Standard Law, cost basis method, and other equivalent methods (such as profit splitting method) are used. When applying these methods, it is necessary to consider whether the type of inventory, transaction quantity, transaction time, and other various conditions are similar when selecting the transaction as a reference.

[Borrowing money]

Independent price comparison method, cost basis method, and other equivalent methods are mainly used. In this case, in consideration of the selection of the transaction to be compared, factors such as the fact that the currency concerning the transaction is the same, the term of lending and borrowing of money, the method of setting interest rates, payment method, creditworthiness, and other interest rates The price calculation above is required.

[Service offer transaction]

Like the lending and borrowing of money, the independent pricing method, the cost basis method, and other equivalent methods are mainly used. When selecting the transaction to be compared, the similarity of the services, the service provision period and various terms of service provision must be the same.

In addition, when service provision transactions are carried out together with the use and transfer of assets, it is necessary to carefully calculate each consideration such as the consideration of the service provision part and the use of the asset, so care must be taken.

[Use or transfer of intangible assets (royalty transaction etc.)]

Intangible assets refer to legal rights such as patents and trademarks as well as trade secrets, other know-how, etc. There are slight differences in the scope depending on the country. Independent price comparison method, cost basis method, and other equivalent methods are used for the calculation method, but when selecting the comparison target, the assets relating to the comparison target transaction are the same type, and the use or transfer Care must be exercised because it is necessary that the time, period, and other transaction terms are the same. Among intangible assets, it is difficult to grasp the value of anything other than legal rights. If you use or transfer it, further pricing becomes difficult, and there are many cases of practical rehabilitation. When these entities are involved in a transaction, it is necessary to show clear pricing basis.

In any of these calculation methods, the selection of the transaction to be compared becomes important. There are two ways of selection based on the transaction price and profit ratio concerning transactions, a method to be carried out between a corporation and a non-related person, and a method to be performed between non-related persons.

In practice, there are many cases in which there is no applicable transaction within the company, so there are many cases where external transactions among non-related persons are standardized.

[Selection of calculation method for independent company price]

Independent intercompany prices are adopted as a basic concept of transfer pricing taxation in many countries and there is no big difference in the basic way of thinking. However, there is a difference in interpretation by the country, and even if a surcharge collects additional taxation amount in a certain country, it is not necessarily the case that the additional taxation amount is fully refunded by request of correction in another country.

Therefore, it is important to be able to set a method for calculating a unified transfer pricing that is valid for transfer pricing taxation in any country.

In Japan, there is an advance confirmation system (APA: Advance Pricing Agreement) in which taxpayers and taxing authorities agree on the method of calculating transfer pricing in advance, and it is considered to be effective as a method of reducing the transfer pricing taxation risk.

In addition, there is Mutual Agreement Procedure (MAP) as a method to eliminate or avoid double taxation on transfer pricing taxation with the country signing the treaty.

-

Transfer Pricing Taxation in Singapore

The Singapore Income Tax Act (SITA: Singapore Income Tax Act) does not have any provision on transfer pricing taxation. We have dealt with this by operating the Singapore Income Tax Law of 33 and 5 3 2A / 3 in accordance with the OECD guidelines on the grounds of the tax avoidance prevention provision of the tax treaty concluded between Singapore and each country. In 2009, we added Article 34 D of the Income Tax Law, which requires compliance with inter-company price.

The Internal Revenue Service announced the "transfer pricing guidelines" on February 23, 2006. In the guideline, we recommend using the independent company price as stipulated in the OECD guidelines for transfer pricing.

The transfer pricing guidelines stipulate the principle of independent army price (The Arm's Length Principle), document preservation obligation (Documentation Requirement), advance confirmation system (APA), mutual consultation (MAP).

■ Calculation of Independent Intercompany Price

About calculating the intercompany price The Internal Revenue Service recommends the following three-step procedure.

Step 1: Comparability Analysis

Step 2: Calculation method of proper independent company price and selection of companies to be verified

Step 3: Determining Independent Intercompany Price

Regarding the method of calculating inter-independent enterprise price, we recommend dividing it into the following two groups and selecting the best method, so we do not prioritize the choice of calculation method.

[Traditional Transaction Methods]

· Independent price comparison method (CUP method)

· Resale price method (RP method)

· Cost method (CP method)

[Transactional Profit Methods]

· Profit division method (PS method)

· Transaction unit operating income method (TNMM)

■ Operation of Independent Intercompany Price

We recommend creating and preserving documents that explain the reasons for calculating the appropriate independent intercompany price as necessary when considering the tax authorities, taking into account cost performance. In the above guidelines, the information to be documented is illustrated.

Supplemental guidelines have been announced in February 2009 concerning Group Loans, which are particularly prone to transfer pricing taxation, and the operation of interindividual company prices on inter-group services.

[Handling of group loan interest rate]

For companies in Singapore who lend to other affiliates with no interest or with interests lower than the market interest rate, they have been accepted by not permitting deduction of interest expenses incurred on loan companies so far.

However, with respect to loans who affiliated companies outside of Singapore from January 2011, it is now required to collect interest by independent company price. However, regarding lending to affiliated companies in Singapore, the same handling as before is still allowed.

[Handling consideration for inter-group service]

In the guideline, taking into consideration the current practice, assuming that routine services are provided only to group companies, we will accept the use of a markup rate of 5%. Routine services include accounting and auditing / tax work, general affairs / legal / payroll accounting / recruitment related work, receivables and receivables management / budget related work, computer support · database management etc.

-

-

-

PE Certified Taxation

■ Overview

Even if you do business overseas, there is a notion that if you do not have a permanent establishment (PE: Permanent Establishment) locally, the income earned will not be taxed locally.

PE refers to a certain place to conduct business overseas. Normally, branch office or agent etc. falls under. In the case of having PE, it is taxed on the income attributable to PE and it is necessary to declare tax payment in local country.

The scope of PE differs according to the national law of each country, but in the OECD model tax treaty it is defined as follows.

In addition, activities in the local country do not fall under PE when only so-called preparatory and supplementary activities such as market research and information provision are conducted.

[Branch PE]

Certain places to conduct projects such as business management sites, branches, offices, workplaces, factories, etc.

[Construction PE]

Those who will survive for a period of time exceeding a certain period at the construction site or construction or installation (OECD model tax treaty Article 5 (3)). Provision of services of supervision of construction, installation, assembly, other work or its work (Article 141 (1) (2) of the Corporation Tax Act).

[Agent PE]

It has subordinate agents that meet certain requirements (Article 141 (1) (3) of the Corporation Tax Law, Article 5 (5) of the OECD Model Tax Convention). However, excluding "independent agent" having an independent position such as an intermediary, wholesaler or the like.

■ Review of PE certified taxation

By consolidating the functions and risks of overseas subsidiaries into Asian headquarters of low tax rate countries, it is possible to reduce the effective tax rate on a consolidated basis. However, regarding changes in logistics form and aggregation of functions by the supply chain, Consideration of PE certification taxation is required.

As a case where PE affirmed taxation should be considered, when a local subsidiary of a foreign corporation acts as a proxy and sells to customers in the country of the country, when a foreign corporation pays sales commission to the local subsidiary, PE certification. There is a possibility that taxation will be done.

When a local subsidiary falls under the agent PE of a foreign corporation, how income subject to taxation is determined is determined by the local laws and regulations and the tax treaties of the customer and the local country. For sales commissions, it is also necessary to consider transfer pricing taxation.

-

-

-

Taxation of Country of Residence and Double Taxation by Source Taxation

In considering taxation in international transactions, there are many kinds of taxes in each country, but corporate tax and income tax are the center. And when imposing tax on income, there are the following two taxation principles;

[Taxation of country of residence]

Considering individuals and corporations in their own country, there is taxation right in the country of residence of individuals and corporations

[Source tax country tax]

Thinking about the reasons for income, countries with income have taxation rights.

(e.g. if a foreign subsidiary pays dividends, interest or royalties consideration to the parent company, the withholding country tax is imposed on the amount paid in the country where the subsidiary is located, and the parent company also taxes the residence country so that the same Double taxation will be incurred on income of.)

Also, due to the different judgment of source of income and the judgment of the place of residence for each country, double taxation will occur due to conflict of taxation rights when conducting international transactions.

■ External tax exemption

As a system for avoiding double taxation, foreign tax credit which deducts foreign tax paid in foreign country from payment tax amount in the country of residence or foreign tax exemption system not taxing foreign source income etc. are set up.

Taxation principles in Japan, Singapore and Hong Kong are as follows;

As Japan is taxed in the country of residence, it is taxed on the global income, but in principle Singapore and Hong Kong are source country taxes, therefore, in principle, only domestic source income is subject to taxation. Low-tax countries such as Singapore and Hong Kong often take the policy of withholding country taxation.

A tax treaty that adjusts the taxation authority by bilateral agreement with the aim of preventing as much as possible the conflict of the taxation right of each country (formally, "Avoiding double taxation on taxes on income and prevention of tax evasion Convention ") has been concluded by many countries.

In utilizing the Asian Regional Headquarters, the international taxation strategy is to avoid such double taxation becomes important. You may also need to consider whether you have a tax treaty with more countries, especially in the countries of Asian region.

2 1 1 2 1 1 As of January 5, Singapore has a tax treaty with 73 countries including most Asian countries and has advantages from the viewpoint of avoiding double taxation.

-

-

-

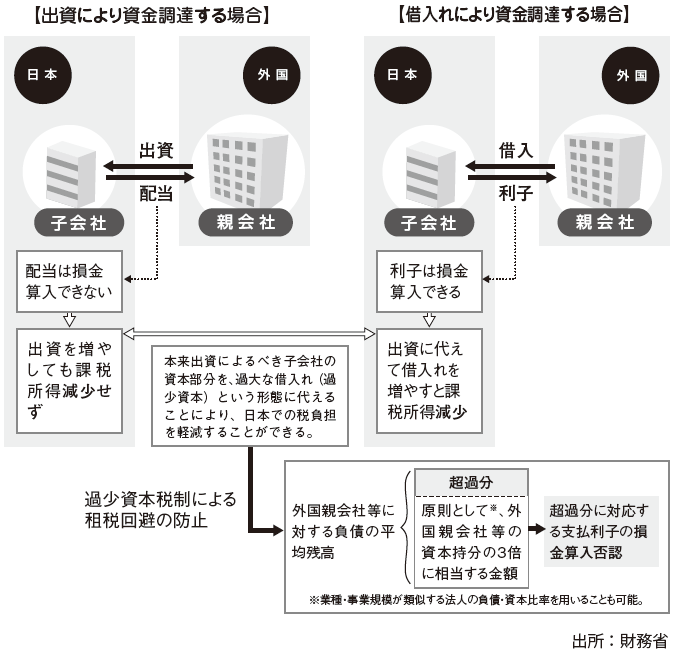

Tenuous capital tax system

The under capital tax system is a system that prevents tax avoidance practices that relocates Japanese income to overseas by putting capital of Japanese subsidiary into under capital.

Although there is no undercapitalization taxation system in Singapore and Hong Kong, if you transfer the Japanese headquarters function to overseas low tax rate countries and raise funds for a Japanese company as a subsidiary, it is necessary to consider the under capital tax system .

When establishing a regional headquarters in a low tax rate country and concentrating funds management of operating companies in Asia as a finance company, it is necessary to consider the presence or absence of under capital taxation and its content based on each country to be supervised.

(e.g. when a corporation procures funds, it may be direct financing or indirect financing such as borrowing. From the viewpoint of taxation, interest expenses such as borrowings are deducted, but since dividends are not allowed to include deductible, procurement by indirect finance may reduce taxable income.)

Also, if a parent company in Japan establishes a subsidiary in Japan, even if there is a transaction of interest with this parent company, it will not be discussed much. This is because if the subsidiary raises funds by borrowing from the parent company and interest expense is deducted, the parent company records interest income and taxes it.

However, in the transaction of interest between the parent company of the foreign corporation of the low tax rate country and the Japanese subsidiary, the income will be relocated to the low tax rate country. In other words, for foreign companies in countries with low tax rates that reduce Japanese income and record interest income by increasing the amount of borrowing as a method of raising funds of subsidiaries in Japan, except for withholding tax in Japan Do not charge taxes.

Therefore, when paying interest on debt, etc. to a foreign corporation that is an affiliated company, if the average debt outstanding on liabilities to that foreign corporation, etc. exceeds three times the share of the capital of a foreign corporation, etc., the debt interest to be paid etc. The amount corresponding to the portion beyond that amount cannot be included in the amount of the deductible (Article 66 (5) (1) of the Treaty Act).

-

-

-

References

[1] 新日本アーンストアンドヤング税理士法人編『アジア各国の法人税法ハンドブ ック』大蔵財務協会、2008 年

[2] 新日本アーンストアンドヤング税理士法人編『クロスボーダー M&A の税務戦 略』中央経済社、2009 年

[3] PWC 編『国際税務ハンドブック〈第 2 版〉』中央経済社、2013 年

-