Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaSingapore

3 Chapter How to Utilize Regional Headquarters

-

-

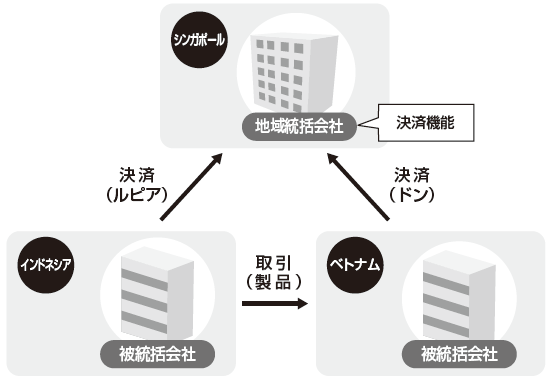

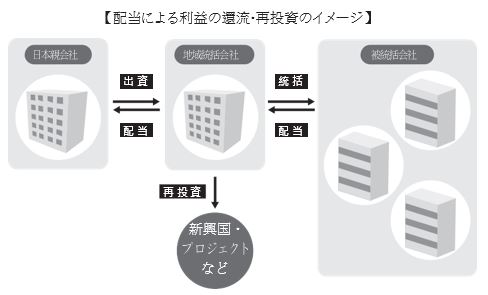

Example of utilization of efficiency by consolidating settlement functions

Currently, there are cases where many Japanese companies enter overseas market and establish multiple subsidiaries as bases of production and sales. However, as the number of subsidiaries increases, the number of transactions increases, making settlement complicated and difficult. Therefore, if a company whose headquarter is located in Japan develops several subsidiaries in Asia, by concentrating in the settlement function in the regional headquarters, it is possible to increase the efficiency of enormous transactions occurring at multiple sites and to mitigate foreign exchange rate risks.

-

Efficient use of settlement, utilization to reduce foreign exchange risk

If there are production bases and sales networks in several countries in the Asian region, and there is a mechanism to mutually complement the raw materials and parts among the group of companies, regional headquarters will make enormous transactions more efficient and currency risk mitigation will be seek. In that case, we will mediate all transactions (mutual procurement of parts and raw materials) among group of companies within the Asian region, and perform offsetting settlement.

Reduction of Foreign Exchange Risk by Three-Base Transactions

In the case where there is a flow of transactions from a group of companies based in Vietnam to a group of companies based in Indonesia, direct transactions are usually made between the two bases, this time the regional headquarters between the two bases will be utilized. The question is, how about in the case of dealing with three bases?

When trading is done between Indonesia and Vietnam, if a regional headquarters based in Singapore is set up between the two countries, usually foreign exchange risk will arise because the two subsidiaries in the two bases use their own currency. However, by placing a regional headquarters in between the two countries and transactions will be offset in the regional headquarters, it is possible to reduce foreign exchange risk. In this case, the regional headquarters will be used as a settlement base and actual product flow will be done between the two countries. Hence, there will be risk that the distribution route will change.

If all these enormous transactions are carried out separately among the operating subsidiaries of each country, concerns that profitability will decline due to the substantial amount of money spent on banking fees alone, as well as the risk of foreign exchange fluctuations may exist. Therefore, by establishing regional headquarters as an overseas holding company, it is possible to do such intermediary transactions.

From this point of view, Singapore and Hong Kong, where financial infrastructure is well established, are often selected as the founding country of the regional headquarters to consolidate settlement functions.

[Improvement in Efficiency of Settlement Functions Using Regional Headquarters]

【地域統括会社を活用した決済機能の効率化】

-

.png)