Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaSingapore

5 Chapter Overseas Relocation of Head Office Functions

-

-

Overview

In the year 1970’s, overseas expansion of Japanese companies began with exports. The establishment of local subsidiaries in developing countries of Europe and America's aiming at the market thereafter, or the establishment of overseas affiliates in Asian countries as the production base for cost reduction increased. However, in recent years, the number of emerging countries such as BRICS in Brazil, Russia, India, China and South Africa has increased in the market. At present, sales in emerging countries are increasing, but it is expected that they will become regions where profit growth can be anticipated in the future. In other words, it is predicted that the source of revenue from Japanese manufacturing industry will shift from traditional Western developed countries to emerging countries. In addition, the number of overseas bases and overseas sales ratios of the entire corporate group will increase, and in the near future most Japanese companies will become multinational corporations and the overseas sales ratio will exceed the domestic sales ratio.

Companies that have headquarters in Japan will also become multinational corporations by establishing overseas affiliates that are production bases and sales bases in several countries. Many Japanese companies have their headquarters in Japan, but "What is the headquarters first?" Headquarters is the composition of the capital relationship of the entire corporate group, the company A that will become the parent company B is considered to be the head office. In general, it is a place to make management decisions and a place where there are functions of management department such as planning, personnel affairs, finance etc. to support it. However, recently, many companies have set up a central management base for each region, prompt business decision making, business strategy planning, human resource development, and financial efficiency, so do not necessarily need to put that function at the headquarters, Some discussion comes out.

In this way, the question "What is the function of the head office?" Comes up.

In the first place, the purpose of the company is "pursuit of profit" and for multinational companies it is "pursuit of profit" of the entire group, so we will try to keep the cost of the whole group as low as possible. Among them, the international taxation strategy is to minimize the cost of taxation essential for multinational enterprises.

Various things can be considered as means to reduce the taxable income of the entire group and to reduce the tax cost but it is most effective to consolidate the profits internally retained at the bases of each country at the base of the low tax rate country it is thought that it is.

Many enterprises have a group structure with Japanese subsidiaries as parent companies, and the parent company in Japan is returning profits from dividends etc. from overseas subsidiaries. However, from the perspective of the international tax strategy, the function of the headquarters is a place to consolidate profits, rather than putting it in a high tax rate country like in Japan, those who has headquartered in a low tax rate country need to pay the taxation cost of the entire group. I think that it can be reduced.

Low tax rate: The following methods are conceivable as a method of bringing profits to the country.

· Aggregate into low tax rate countries through dividends

· Transfer taxable income to low tax rate countries as interest income on loans by responding with funds demand of subsidiaries of each country by borrowing rather than capital increase

· Manipulate the transaction price of internal transactions and transfer taxable income to low tax rate countries

· Transfer intangible assets such as trademarks and patents to low tax rate countries to relocate to low tax rate as royalty income

· By transferring administrative functions to low tax rate countries, they transfer to low tax rate countries as service fee income for subsidiaries in each country

In fact, in order to carry out the above method, there are remittance restrictions, currency exchange, tax avoidance taxation of each country, etc., so we need to consider the risk beforehand. In particular, countermeasures are important because countries with low tax rates are expected to apply tax and haven countermeasure tax system. For transactions between corporate groups, it is necessarily to deal with transfer pricing taxation for transaction prices.

Organizational restructuring measures that companies move headquarters to low tax rate countries is one of the most important management strategy options related to resource allocation within companies, and depending on their arrangement, reduction of the tax payment amount of the entire group, I can hope for it. If there is a system or tax system suitable for realizing this, it is very natural to use it without being caught up by nationality from the essential character of the enterprise of profit pursuit.

-

Case of Overseas Relocation of Head Office

In the business activities of multinationals, the international taxation strategy to reduce the tax cost of the entire group is becoming more important. We will verify the cases where the head office function is actually transferred to a low tax rate country or if the profit is transferred to a low tax rate country.

■ Microsoft

Microsoft (Microsoft Corporation) produces and sells core software for PCs around the world, mainly Windows, and the revenues obtained from subsidiaries around the world finally aggregate into headquarters located in Redmond, Washington, USA It should be done. However, following the invitation of the Irish Government, Microsoft established a production facility in Ireland from 1985, transferring part of intangible assets relating to core software to the Irish subsidiary. As a result, part of taxable income originally generated in the United States will be relocated to Ireland, not Ireland's corporate tax (12.5%) instead of American corporate tax (35%), resulting in taxation. The burden was greatly reduced. If all the headquarters functions had been transferred, it would have been possible to further reduce the tax burden.

■ Seagate Technology

Seagate Technology (Seagate Technology, LLC.) Is a company that manufactures and sells hard disk drives (HDDs) and is always leading company on this particular field. In 1996, it absorbed Conner Peripherals, Inc. with another company in the same industry, it became the world's largest shares on the basis of shipment quantity in the HD market. In 2006, Maxtor Corporation acquired the 4th in the industry at that time did.

In 2000, we also sold the software division to Veritas (Veritas Software, Corp.) led by investment funds and abolished listing in the New York Stock Exchange in 2000. As a result, Seagate Technology has separated the software division and strengthened its financial standing.

In line with this re-organization, we registered the headquarters relocation to the Cayman Islands, which is a tax and haven country, and then re-listed on the New York Stock Exchange in December 2002. Currently head office is located in the Cayman Islands and in 2009 Form 10-K submitted to the US Securities and Exchange Commission, the head office location is "PO Box 309 GT Ugland House, South Church Street George Town, Cayman Islands", the tax jurisdiction is written as "Cayman Island".

■ DFS

DFS (DFS Group, Limited) operates DFS Galleria one of the large-scale duty free shop chain. We are holding a holding company in Bermuda, an American corporation that established its head office in Hong Kong and its principal business activities in the form of partnership.

■ Sunstar

Sunstar, Inc., known for brushing teeth etc., moved its headquarters from Japan to Switzerland in 2009.

As a method, first, we purchased 52% of our own shares through MBO (Management Buy-Out), together with the shares held by the founder was 83.53% and was delisted.

In this method, we established a special purpose company in Japan and purchased shares. It is a case close to a triangular merger as it is a trading of shares in the company, shareholders, special purpose company. In the case of a triangular merger, it is also possible to exchange for shares of the parent company, but in this case we purchased more than (2/3) of the stock in cash, so we were able to make the tender offer successful. -

Example Head Office Overseas Relocation Scheme

Regarding on the overseas relocation of head office functions, major companies in the world actually do it, but various schemes have been taken regarding on the practical procedures. On the other hand, if you simply move stocks etc., you will be pointed out by the tax authorities as "tax evasion acts", which could result in an unexpected tax burden.

We will examine the method of relocating the headquarters to overseas and the company law and tax law on organizational restructuring that should be taken into account at that time.

In order to transfer the head office functions of a Japanese company to a foreign company, the following two steps are required.

(1) transfer shareholders of a Japanese company to a shareholder of a foreign company and make Japanese company a wholly owned subsidiary of a foreign company

(2) transfer assets etc. of the Japanese company to a foreign company

Regarding the above (1), if the Japanese company is an unlisted company and the number of its shareholders is small, the following scheme can be considered.

① The shareholder of the Japanese company A company establishes the foreign company B and then the foreign company B buys all the shares of the Japanese company A company

② The shareholder of the Japanese company A will invest all the shares of company A in kind and establish the foreign company B

However, in case #2, it is difficult to fulfill the requirement for qualified in-kind investment, because the investment is spot in the foreign company, taxation transfer taxation will occur.

■ Provisions under the Company Law in Japan

Under the current Corporate Law, when absorption type organization restructuring (absorbing merger, absorption split, stock exchange) is conducted, it is permitted to deliver property other than shares of surviving company etc. to shareholders of a dismissed company etc. (Companies Act 7 7 9 9 1 2, 751 1 1 2 3, 751 1 2 3, 758 4 - 5, 768 1 2, 770 1 1 2 3). In the former Commercial Law, consideration for mergers, etc. was generally restricted to shares of surviving company etc. In principle, due to the amendment of the Companies Act in 2007, a merger in which cash is delivered as consideration for the merger and shares of the parent company are issued. It is now possible to do a triangular merger.

Along with the revision of this company law, even in the case of delivering certain parent company shares as a consideration for merger etc. in the reform of the tax system in fiscal 2007, we do not recognize gains or losses on transferring of transferred assets as qualified organization reorganization (corporate tax law Article 2, 12, 8, 11, 16 of the Act), the Order for Enforcement of the Corporation Tax Law (hereinafter referred to as "Legal Order" Article 4, paragraph 2, 1, 5, 14)), and for shareholders of companies to be merged, It is said that we do not recognize the gains on transfer of shares (Act of 6 1 2 2 ④ 9, Instruction 119 7).

Organizational restructuring such as acquisitions and mergers of companies is an act of increasing corporate value by increasing profits by companies. As the reorganization of the company increased the options for consideration by the amendment of the Company Law, the efficiency and flexibility of international organizational restructuring had increased.

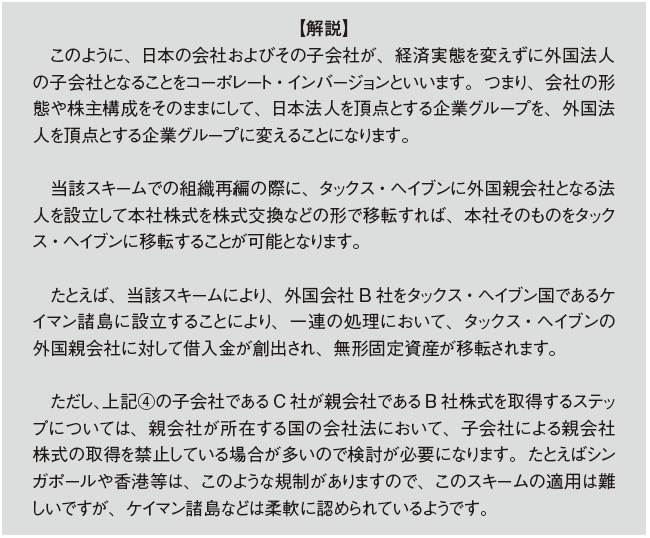

[Relocation by triangular merger]

By the triangular merger method, you can relocate the Japanese headquarters to foreign countries with the following scheme..png) Company B founded ... ①

Company B founded ... ①.png) Company B acquires all shares of treasury stock (shares of company B) ... ②

Company B acquires all shares of treasury stock (shares of company B) ... ②.png) Company B established company C ... ③

Company B established company C ... ③.png) Company C acquires company B shares ... ④

Company C acquires company B shares ... ④.png) B company shares to A shareholder ... ⑤

B company shares to A shareholder ... ⑤.png)

.png)

Final form (completed form) ... ⑦

.png)

■Deferred taxation

If organization reorganization by triangular merger is qualified organization restructuring, deferment of taxation will be carried out at the time of realignment, without recognizing gains or losses on transfer of transferred assets or shareholders of the merged corporation etc., gains on transfer of shares. Therefore, we need to consider whether we meet the requirements for qualified organization restructuring.

Regarding the organizational restructuring of cross-border by triangular merger, in cases where shares of foreign parent company are issued to non-resident or foreign corporate shareholders by a certain organization reorganization from the viewpoint of international taxation properly, deferral of taxation is said that tax is imposed when new shares are issued without admitting.

[Special Provisions on Scope of Qualified Merger (Treaty Article 68 2 - 3 1) etc.]

A triangular merger of a domestic corporation within a corporate group that has a "specific control relationship" between a merger corporation and a corporation to be merged, for which the shares of "specified light taxable foreign corporation" are delivered Merger) are excluded from the scope of merger that is considered qualified merger.

Therefore, in this case, gains on transfer of transferred assets will be recognized.

Specifically, the "specific control relationship" is regarded as the following relation.

· Just before the merger, one of the two domestic corporations owns directly or indirectly more than 50% of the other issued shares etc.

· The relationship between the two domestic corporations in cases where more than 50% of the respective issued shares, etc. are directly or indirectly owned by the same person immediately before the merger etc.

· "Specific light taxable foreign corporation" means a foreign corporation that falls under the following.

· A foreign corporation having a head office etc. in a country where there is no tax imposed on income of a corporation

· In any of the business years that started within 2 years before the start date of the business year of the foreign corporation including the date on which the merger within the specified group is carried out, with respect to the income for that business year. A foreign corporation whose tax amount to be imposed was less than 25% of the amount of the income (Article 68 2 - 3 5 of 1), (Article 39 34 - 3 5)

Provided, however, that the foreign corporation falls under all requirements of the same exemption requirement in the so-called tax / haven countermeasure tax system, that is, (1) business standards, (2) substantive standards, (3) management control standards, (4) non- related person standards or the country of country standard In the case, it is decided that it does not fall under the "specific light taxable foreign corporation" (Article 39 34-34 ⑦).

[Taxation of shareholders in the case of a specific merger etc.]

In the event that shares of "Specific Light Taxable Foreign Corporation" are delivered as consideration for merger etc., shareholders will be taxed on transfer income etc. concerning the transfer of old shares.

Individual shareholder's taxation (Article 37-14-3) ①②③⑤

A resident or a non-resident shareholder having a permanent establishment (PE: Permanent Establishment) in the country, as a consideration due to a merger or the carried out by a domestic corporation that issued an old stock, issuance of a merger corporation etc. immediately before the merger. We will receive the shares of foreign corporation holding all of the shares etc. In the event, the shares that have been delivered fall under the shares of a specified light taxable foreign corporation, tax will be levied on the transfer income etc. of the transfer of the old shares.

In addition, nonresidents who do not have PEs in the country are taxed in the same case when the income from transfer of old shares falls under domestic source income.

Taxation of corporate shareholders (Article 68-3-3 ① ~ ③, 61 § 2 ② ④ ⑨)

Corporate shareholders will receive shares of foreign corporations holding all of the issued shares etc. of the merger corporation etc. as compensation for the merger etc. done by the domestic corporation that issued the old stock immediately before the merger etc. In the event, the shares that have been delivered fall under the shares of a specified light taxable foreign corporation, it is decided that gains or losses on the transfer will be recorded as if the assignment was made by the market price of the old shares.

-