Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaSingapore

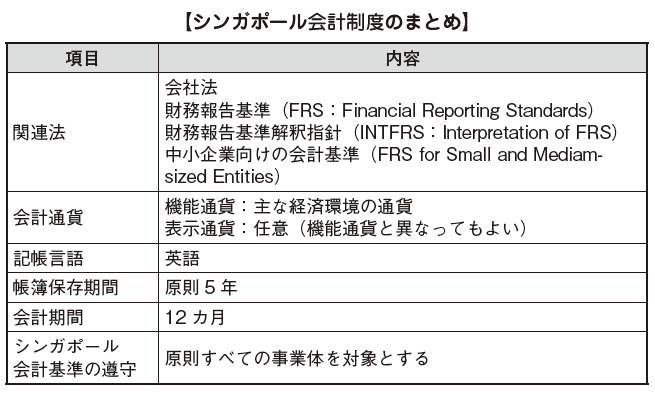

7 Chapter Accounting

-

-

Audit System

In the case of Japan, certified public accountant audits are not enforced on small companies other than listed companies and large companies.

Meanwhile, the accounting system of Singapore is regulated under UK law. Therefore, in principle, branches of all companies and foreign companies shall be audited by a certified public accountant. Singapore is subject to auditing by the accounting auditor based on the Company Law.

In Singapore, based on Article 207 of the Corporate Law, they shall appoint a certified public accountant as an accounting auditor within three months after the establishment of the company and have to receive an audit of the financial statements once each year. In other words, all companies are forced to conduct external accounting audits called certified public accountants. Also, in the case of branch offices, audits of certified public accountants are required.

However, with regard to the audit, as a special exception, companies with shareholders of not more than 20 individual shareholders, and those with sales of less than S $ 5 million per year or dormant companies shall be exempted from the audit. In other words, if the shareholder is not a corporate shareholder or a dormant company, an audit is required.

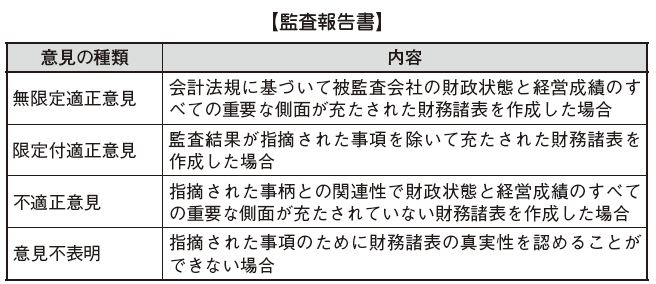

■ Content of audit

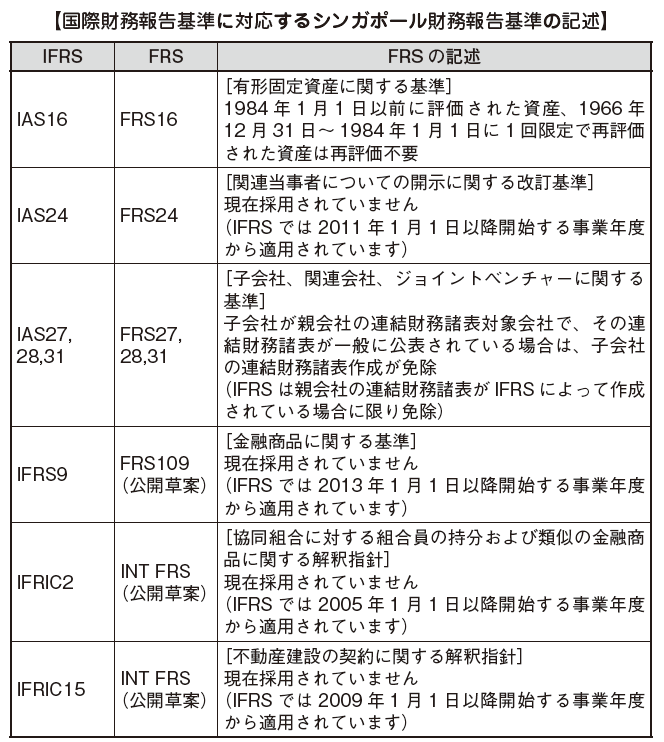

Four types of reports are expected for Singapore's audit report, as well as Japan's audit standards and international auditing standards.

[Forced installation of audit committee]

With the Asian economic crisis that occurred in 1997, Singapore has undergone various reforms on corporate governance of listed companies. In one of them, the Corporate Governance Council was set up in early 2010, and governance regulations have been reexamined. In Singapore's Corporate Law, the establishment of a board of directors is not enforced, but in the case of listed companies it is generally considered that a board of directors has been established, so the establishment of an audit committee in the Corporate Law (Article 201B) is compulsory.

According to the Corporate Law, as in Japan, independence is required to be maintained, and in cooperation with the accounting auditor, the audit plan and internal audit procedures are examined and the company's audit report and financial statements Balance sheet · profit and loss statement). The duties of the Audit Committee under the Companies Act do not include business audits, etc., and can be said to be only the function of accounting audit.

Meanwhile, the newly established governance regulations strengthen the obligation to monitor the accounting auditor, including the cost performance audit of the accounting audit, the necessity of considering whether the internal control is appropriate, etc. It is obliged the range of it is enlarged.

[From Singapore certified public accountant to Chartered Accountant]

In June 2013, the Singapore Accountancy Commission (SAC: Singapore Accountancy Commission) reviewed the educational system of accountants and introduced the Qualification Program (QP). The purpose of introduction is to improve the professional skills of accountants and to support overseas expansion. Also, due to this change, they changed the name of certified public accountant to Chartered Accountant (CA).

Traditionally, college graduates who have taken accounting sciences or accounting related qualification holders are recognized as certified public accountants only after three years of practical experience and intensive 5-day training and examination provided by the Institute of Certified Public Accountants of Singapore.

Under the new system, they can apply for a Chartered Accountant only if they are a college degree holder and have over 3 years of practical experience at Accredited Training Organization (ATO) as a training institution and have 6 courses (It is limited to those who took the examination in 5 courses).

There are currently about 30 accredited accounting firms, but the Singapore Certified Public Accountants Association seems to be planning to increase this number.

The certified public accountant (approximately 18,000) who was registered at the same time as the Singapore CPA is automatically exempt from application of the new system, and as of July 1, the same day as the name of the Chartered Accountant was changed.

The Singapore Accounting Committee has an agreement to mutually recognize membership with the Institute of Chartered Accountants in England and Wales (ICAEW), and since Chartered Accountants can engage in accounting work in the UK, the results shall substantial increase in the number of supported countries.

-