Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaThailand

9 Chapter Q&A

-

-

Q&A1

Q

I am considering establishing a corporation in Thailand in the future. We are considering establishing at a trading company and factory, and we have grasped conditions and establishment procedures in general. It is a place to report on future investment to the head office. Please tell me if there are points that are likely to be a blind spot when establishing a trading company or factory.

A

Since we are already summarizing conditions and establishment procedures, you know about capital controls.

There are the following points as well that misunderstanding that those who investigate capital regulation to some extent are often misunderstood.

Trading company: Wholesale and retail businesses can capitalize at 100% foreign capital with a capital of 100 million baht or more

Manufacturing industry: Manufacturing industry is not subject to negative list, so you can invest at foreign investment 100%

None of the above is a mistake.

However, on the other hand, it is insufficient as information, and that is in some cases it may be a legal trouble after establishment.

1. In wholesale and retail businesses, you can capitalize at 100% foreign capital by paid capital of 100 million baht or more.

However,

· Retailers with minimum capital of 100 million baht or more and minimum capital per store of 20 million baht or more

· Wholesale business with minimum capital of 100 million baht or more per store

It is an accurate definition, especially when deploying multiple stores, it is necessary to pay attention to the point that additional capital is required.

It is also worth noting that when conducting both retail and wholesale business, each will cost 100 million baht or more.

2. It is the so-called forecast production type manufacturing industry that 100% foreign investment can be made, the manufacturing industry in contract manufacturing and contract processing is regarded as a contracting business, widely as a service industry and it is possible to become a subject of negative list there is. Therefore, it is necessary to confirm beforehand whether manufacturing activities carried out by the company are stuck on the negative list.

In any case, I think that consideration should be taken not to be such a thing after the establishment.

-

Q&A2

QWe plan to set up a joint venture with a local company in Thailand. I think that I will make Thai director, but I am a bit worried if I am a trustworthy person. Is there any good way to do it?

AIn Thailand there are foreign investment restrictions, especially for the service industry, there are options such as applying for BOI, establishing with a local partner, etc.In the case of establishing as a joint venture with a local partner, in many cases we will take the partner Thai director as director. Japanese people often become directors, but it is also seen that they are not resident in Thailand.The Japanese director is in Japan, leaving all the business to the Thai director.I think that it is one management method, but I think that I often find myself a little uneasy about leaving everything.In Thailand you can limit the signature authority.For more than a certain amount of payment, you can not sign if you are not a Japanese director. In addition to delegating daily work, it is possible for Japanese people to make a decision on serious business decisions by making decisions in Japan.In addition, there are also a signature method in the signature method, but signature with a common name is necessary even for a small settlement etc, so we can not recommend it much because the speed of daily work is delayed. It is important to delegate authority to a certain extent and keep speed control and important decision-making control. -

Q&A3

QCurrently I would like to advance into industrial park in Thailand. There are many industrial parks in Thailand, but where is the industrial area where Japanese companies enter a lot?

ARayong, Chonburi, Ayutthaya, which are the major areas around Bangkok, are regions where many Japanese companies enter the market after Bangkok. -

Q&A4

QWhen establishing a company in Thailand, is it necessary to certify the document at the notary office or embassy as a procedure on the Japanese side?

ANotary of the Ministry of Foreign Affairs, certification is basically necessary. However, practical treatment varies depending on accounting firms, law firm offices, etc. Please consult us before proceeding. -

Q&A5

QI am planning to establish a joint venture company in Thailand, but how can I grant the signature right?

AIt is common to set requirement that it will not be effective unless there are multiple names of all or a part of the directors holding signing rights of each invested company. By doing so, you can equally grant signing rights to each investor. However, there is a disadvantage that the daily work also needs to be renamed, making it inefficient. In order to avoid such a situation, it is considered preferable to use properly such that it is possible to use a common name for certain things, a single signature for daily business things, and so on. -

Q&A6

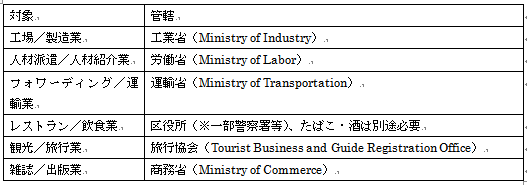

QThe registration of the company was completed and a foreign business license was obtained. When starting business operation, is there anything to be surprised about registration and registration of foreigner's license?

AIn order to operate the business after establishment, it may be necessary to acquire a separate license depending on the type of industry. Unless these licenses are acquired, there is a risk that business operation will not proceed or business will be allowed without permission, so you need to confirm which license acquisition is required beforehand. Here is a list of the main licenses. Although the acquisition period of each of the above licenses is different, for example, it takes 1.5-2 months for food and drink.

Although the acquisition period of each of the above licenses is different, for example, it takes 1.5-2 months for food and drink. -

Q&A7

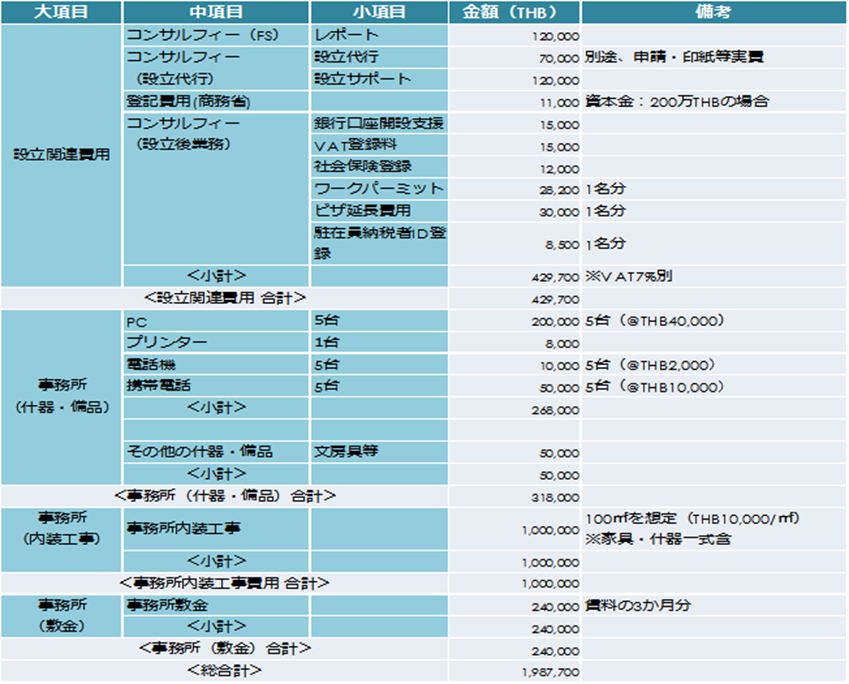

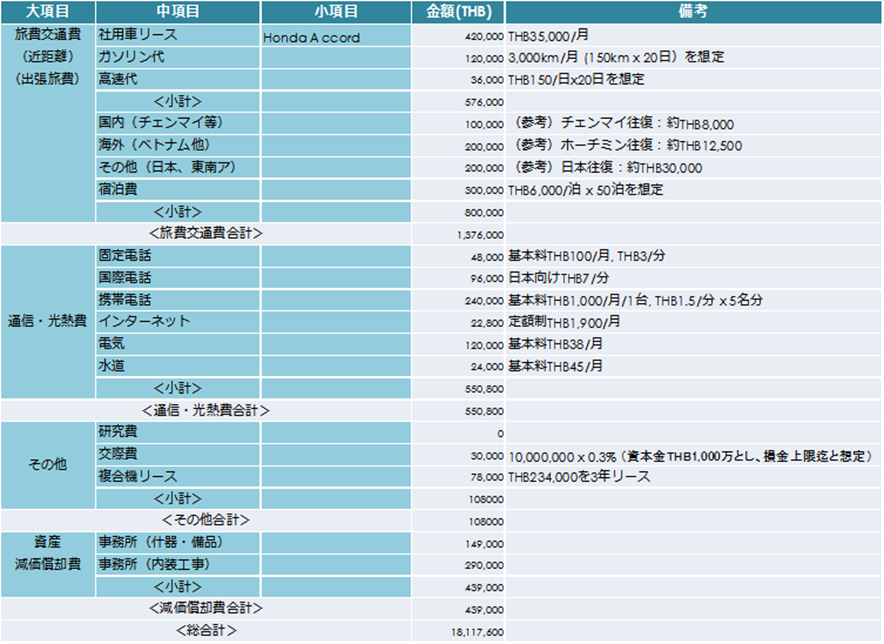

QI often hear that Japanese companies are easy to do business in Thailand, but in order to make it a starting point for considering in-house what kind of cost it will cost to start a business on the ground, Please tell me.

ADepending on the type of industry, this time I would like to estimate assuming the case of a trading company in Bangkok, the service industry. I think that you can check the market price based on this and calculate your own items etc.<Initial cost> <Running cost ①>

<Running cost ①> <Running cost ②>

<Running cost ②>

-

Q&A8

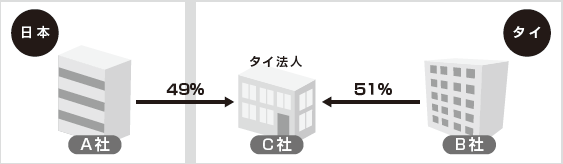

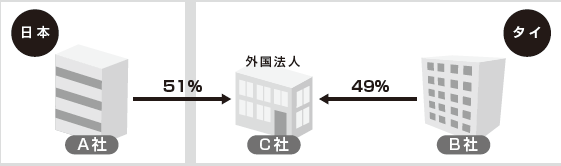

QWhen establishing a joint venture company C in Thailand where 49% of Japanese corporation A and 51% of Thai corporation B invests, will company C be subject to the regulation of the Foreign Business Act?AUnder the Foreign Business Law, if foreign capital accounts for 50% or more of the total capital, the company is defined as a "foreign corporation" and is subject to regulation. In this case, the foreign capital ratio of Company C is less than 50%, so it does not fall under the definition of "Foreign Corporation" and Company C will not be subject to the Foreign Business Act.

-

Q&A9

QI am planning to establish a joint venture company C in Thailand, which owns 51% of Japan A company and 49% of Thai B company. In this case, is Company C subject to the regulation of the Foreign Business Act?AAs explained in ①, entering foreign capital of 50% or more is subject to regulation. In this case foreign capital will be 50% or more, so it is deemed to be a "foreign corporation" and Company C will be subject to the Foreign Business Act.

-

Q&A10

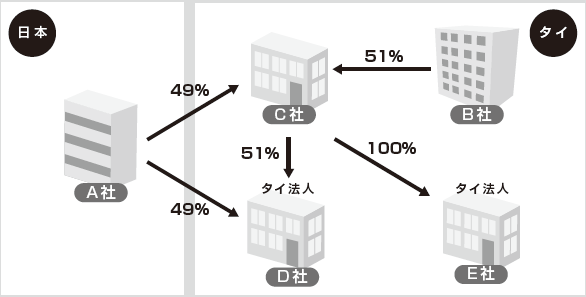

QWe have established a joint venture company C in the scheme of case 1). In addition, Company C wants to establish a new company in Thailand with (1) a joint venture company D of 51% C, a joint venture company D 49% Japan A, and a company E of 100% owned company C). Will D and E companies be subject to the regulation of the Foreign Business Act in the cases of (1) and (2) above?AFirst of all, as for case (1), company C is regarded as "Thai corporation" as in case 1). Therefore, company D will become a joint venture company of Japan A company 49%, Thail C company 51%, it will be considered as "Thai corporation" and will not be subject to regulation.Also in case (2), Company E is established as a 100% investment by Company C regarded as "Thai corporation", so it is regarded as "Thai corporation" and is not subject to regulation.

-

Q&A11

Q

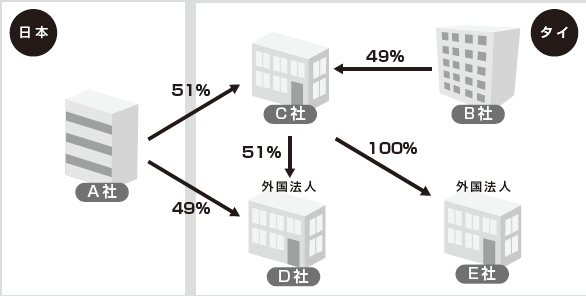

We established a joint venture company C in the scheme of case 2). In addition, Company C wants to establish a new company in Thailand with (1) a joint venture company D of 51% C, a joint venture company A 49% of Japan A, and an E company 100% owned by ⑵ C company. In the cases of (1) and (2) above, will it be subject to the regulation of the Foreign Business Act?

A

First of all, as for case (1), company C is deemed to be a "foreign corporation" as in case 2). Therefore, Company D will be a joint venture company of Japan A Company 49% Japan C Company 51%, it will be regarded as "100% foreign corporation" and subject to regulation.

Also in case (2), Company E is established as a 100% investment by Company C regarded as a "foreign corporation", so it is considered as "100% foreign corporation" and subject to regulation.

-

Q&A12

QI have a subsidiary in Thailand, but I am considering whether to make a capital increase or borrow from a parent company. What are the merits and demerits of each?

AIn Thailand there are no special restrictions on parent-child loans. Therefore, if a local subsidiary in Thailand raises funds, it may be possible to increase capital from the parent company, borrow from the parent company, or borrow from a local financial institution. In consideration of each merit and demerit, it is necessary to decide the procurement method.png)

-

Q&A13

QWe have been a company that has been encouraged by BOI until now, but it is included in the business to be abolished according to the new BOI encouragement. There are various benefits for BOI encouragement, but will these benefits be maintained?

A.Basically it is to be maintained about non taxable benefits. Specifically, it has the following benefits.· Land ownership· 100% foreign capital contribution· Relaxation of requirements for obtaining work permitsHowever, as stated above, it is limited to the benefits under "Non taxation". Tax exemption for corporate income tax and exemption from import duties on exported raw materials is not applicable, so pay attention. -

Q&A14

QAs a requirement of BOI, there is a condition to add value of 20% or more, but how do you calculate the added value ratio in the application?

AThe calculation formula of the value added rate is as follows.Value added = [(ex-factory price of the product) - (raw material cost) - (utility cost)] / (ex-factory price of the product) * 100

The value-added rate is a criterion, but it does not depend on that alone. The process of production and processing is also emphasized, and production and processing processes need to be done in Thailand. Therefore, only attaching the seal, it will not be accepted by addition of value added by granting patent or trademark right.As a background, promotion of employment is also necessary, which may not be satisfied in the above.Even in the definition of manufacturing, it seems that it does not become a manufacturing industry, such as attaching a seal as described above. In reality, we need to import raw materials into Thailand, leaving production and processing process, and produce or process in Thailand. -

Q&A15

QIs Thailand a domestic corporation (Thai capital 51% or more) possible to acquire land and condominium?

ARegarding land and condominiums, it is possible to acquire it in Thai domestic corporation (Thai capital 51% or more and majority shareholders are Thai citizens or Thai domestic corporations) and BOI companies. Foreign corporations or individuals with foreign nationals can only acquire condominiums. For houses etc., foreign corporations and BOI enterprises can not be acquired, but Thai domestic capital enterprises are available for purchase.In addition, service apartments are handled in the same way as condominiums if the ownership of each room or facility can be distinguished. -

Q&A16

QWhat taxes and fees are involved in obtaining land?

ASpecific business tax and stamp duty will be charged as tax related to land acquisition.Similar to VAT, the specific business tax is paid by the payor in addition to the purchase price, and the receiving side declares / pays the tax. Specified business tax on real estate will be 3.3% of purchase price.In addition, the stamp duty will be 0.001% of the purchase price.On the other hand, the fee to the government at the time of land purchase will be 2% of the purchase price or value. Usually we calculate by purchase price. Since this fee is capitalized together with the normal purchase price, it will be processed on land accounting in the land (in case of expenses it will be Government fee).

-

.png)

.png)

.png)