Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaThailand

7 Chapter Tax

-

-

File a Tax Return and Payment

SBT taxable period is a calendar month. SBT return (Form ภธ. 40) must be filed on a monthly basis regardless whether or not the business has income. SBT return and payment must be submitted to the District Revenue Office within 15 days of the following month. If taxpayer has more than one place of business, each place of business must file its return and make the payment separately unless there is an approval from the Director-General.Stamp dutyStamp duties are taxed on instruments and not on transactions or persons. For the purposes of stamp duty, an instrument is defined as any document chargeable with duty under the Revenue Code. The stamp duty rules are contained in Chapter VI of Title II of the Revenue Code.1. Persons liable to stamp duty1.1 Only instruments listed in the stamp duty schedule are subject to the stamp duty and the persons liable to pay stamp duty are those listed in column 3 of the schedule. They are, for example, the persons executing the instrument, the holders of the instrument or the beneficiary.1.2 If an instrument liable to duty is executed outside of Thailand, the first holder of theinstrument in Thailand shall pay the duty by stamping at the full amount and canceling within 30 days from the date of receiving the instrument. If he does not comply as such, the instrument shall not be deemed duty stamped.If he does not comply with the provisions of Paragraph 1, any holder of the instrument shall pay the duty by stamping at the full amount and canceling, and then he shall be able to submit the instrument for collection, endorsement, transfer or claiming of benefit.Any holder who acquires possession of the instrument in accordance with this Section before the expiration of the time limit specified in Paragraph 1 may pay the duty by stamping at the full amount and canceling, and he has the right of recourse against the previous holders.1.3 If a bill submitted for payment is not duty stamped, the recipient of the bill may pay the duty by stamping at the full amount and canceling, and may either have the right of recourse against the person liable to duty or deduct the amount of duty from the payment due.1. Instruments liable to stamp dutyThe instruments liable to stamp duty include, inter alia, transfers of land, a lease, stock transfers, debentures, mortgages, life assurance policies, annuities, power of attorney, promissory notes, letters of credit, travelers cheques.2. How to duty stamped"Duty stamped" means(1) in the case of an adhesive stamp, payment of duty is made by affixing a stamp on the paper, before or immediately when an instrument is executed, in an amount not less than the duty payable, and canceling such stamp; or(2) in the case of an impressed stamp, payment of duty is made by using a paper with an impressed stamp in an amount not less than the duty payable and canceling such stamp, or by submitting an instrument to an official to impress the stamp and paying an amount not less than the duty payable and canceling such stamp; or(3) in the case of payment by cash, payment of duty is made in cash in an amount not less than the duty payable in accordance with the provisions of this Chapter or in accordance with a regulation prescribed by the Director-General with the Minister’s approval.In stamping duty as prescribed under (1) and (2), the Director-General shall have the power to order the compliance in accordance with (3) instead1. Rate of Stamp DutyNature of Instrument/Transaction

Stamp Duty

1.Rental of land, building, other construction or floating house

For every 1,000 Baht or fraction thereof of the rent or key money or both for the entire lease period

1 Baht

2. Transfer of share, debenture, bond and certificate of debt issued by any company, association, body of persons or organization.

For every 1,000 Baht or fraction thereof of the paid-up value of shares, or of the nominal value of the instrument, whichever is greater.

1 Baht

3. Hire-purchase of property.

For every 1,000 baht or fraction thereof of the total value

1 Baht

4. Hire of work

For every 1,000 Baht or fraction thereof of the remuneration prescribed.

1 Baht

5. Loan of money or agreement for bank overdraft

For every 2,000 Baht or fraction thereof of the total amount of loan or the amount of bank overdraft agreed upon.Duty on the instrument of this nature calculating into an amount exceeding 10,000 Baht shall be payable in the amount of 10,000 Baht.

1 Baht

6. Insurance policy

(a) Insurance policy against loss

For every 250 baht or fraction thereof of the insurance premium.

(b) Life insurance policy

For every 2,000 baht or fraction thereof of the amount insured.

(c) Any other insurance policy

For every 2,000 baht or fraction thereof of the amount insured.

(d) Annuity policy

For every 2,000 baht or fraction thereof of the principal amount, or, if there is no principal amount, for every 2,000 baht or fraction thereof of 33 1/3 times the annual income.

(e)Insurance policy where reinsurance is made by an insurer to another person.

(f)Renewal of insurance policy

1 Baht

1 Baht1 Baht

1 Baht

1 Baht1 Baht

Half the rate for the original policy7. Authorization letter i.e., a letter appointing an agent, which is not in the form of instrument or contract including a letter appointing arbitrators:

(a) authorizing one or more persons to perform an act once only.

(b) authorizing one or more persons to jointly perform acts more than once.

(c) authorizing to perform acts more than once by authorizing several persons to perform acts separately; the instrument will be charged on the basis of each individual who is authorized.

10 Baht

30 Baht

30 Baht8. Proxy letter for voting at a meeting of a company

(a) Authorized for one meeting only

(b) Authorized for more than one meeting

20 Baht

100 Baht9. (1) Bill of exchange or similar instrument used like bill of exchange for each bill or instrument

(2) Promissory note or similar instrument used like promissory note for each note or instrument

3 Baht

3 Baht10. Bill of lading

2 Baht

11. (1) Share or debenture certificate, or certificate of debt issued by any company, association, body of persons or organization

(2) Bond of any government sold in ThailandFor every 100 baht or fraction thereof.

5 Baht

1 Baht12. Cheque or any written order used in lieu of cheque for each instrument

3 Baht

13. Receipt for interest bearing fixed deposit in a bank

5 Baht

14. Letter of credit

(a) Issued in Thailand

- For value less than 10,000 Baht

- For value of 10,000 Baht or over

(b) Issued abroad and payable in Thailand for each payment

20 Baht

30 Baht

20 Baht15. Traveler’s cheque

(a) For each cheque issued in Thailand

(b) For each cheque issued abroad but payable in Thailand

3 Baht

3 Baht16. Each goods’ receipt

issued in connection with carriage of goods by waterway, land and air, namely, an instrument signed by an official or cargo master of a transport vehicle which carries goods as specified in that receipt upon issuing the bill of lading1 Baht

17. Guarantee

(a) For an unlimited amount of money

(b) For an amount exceeding 1,000 baht

(c) For an amount exceeding1,000 baht but not exceeding 10,000 baht

(d) For an amount exceeding 10,000 baht

10 Baht

1 Baht

5 Baht

10 Baht18. Pawn broking

For every 2,000 baht or fraction thereof of the debt.

If the pawn broking does not limit the amount of debt.

1 Baht

1 Baht19. Warehouse receipt

1 Baht

20. Delivery order

1 Baht

21. Agency

(a) specific authorization

(b) general authorization

10 Baht

30 Bah22. Decision given by an arbitrator

(a)In the case where the dispute is concerned with the amount of money or price for every 1,000 baht or fraction thereof

(b)In the case where no amount of money or price is mentioned.

1 Baht

10 Baht23. Duplicate or counterfoil of an instrument,

namely, an instrument having the same contents as the original document or contract and signed by the person executing the instrument in the same manner as the original.

(a)If the duty payable for the original does not exceed 5 baht.

(b)If the duty exceeds 5 baht.

1 Baht

5 Baht24. Memorandum of association of a limited company submitted to the registrar.

200 Baht

25. Articles of association of a limited company submitted to the registrar.

200 Baht

26.New articles of association, copy of amended memorandum of association or articles of association submitted to the registrar.

50 Baht

27. Partnership contract

(a) Contract on the establishment of a partnership

(b) Amendment of the contract on the establishment of a partnership

100 Baht

50 Baht28.Receipt only as specified below:

(a) Receipt issued for government lottery prizes;

(b) Receipt issued in connection with a transfer of, or creation of any right in, an immovable property, if the juristic act which gives rise to such receipt is registered under the law;

(c) Receipt issued in connection with a sale, sale with right of redemption, hire-purchase or transfer of ownership in a vehicle, only if the vehicle is registered under the law governing such vehicle. If the receipt under (a) (b) (c) has an amount of 200 Baht or more: for every 200 Baht or fraction thereof.1 Baht

-

Surcharge

5.1 Where an instrument is not duly stamped, the person liable to duty or the holder of the instrument or the beneficiary thereunder shall be entitled to present the instrument to the tax official for payment of duty who shall allow payment of the duty, subject to the following provisions:(a) Where the instrument not duly stamped is an instrument executed in Thailand and is presented to tax official for payment of duty within 15 days from the day when the instrument was required to be duly stamped, payment of duty shall be allowed merely at the rates set forth in the Stamp Duty Schedule.(b) In other cases, payment of duty shall be allowed, but a surcharge shall be imposed as follows:(1) If it appears to the tax official that no more than 90 days have passed since the days when the instrument was required to be duly stamped, there shall be imposed a surcharge of twice the amount of duty or of 4 Baht, whichever is higher.(2) If it appears to the official that more than 90 days have passed since the day when the instrument was required to be duly stamped, there shall be imposed a surcharge of five times the amount of the duty or of 10 Baht, whichever is higher.If, in consequence of the inspection conducted by the official or of the charge preferred or information furnished by any person, whether or not a government official, it appears that:(a) a receipt required to be issued under the Revenue Code has not been issued, the tax official shall have the power to charge the full amount of duty, and in addition, to impose a surcharge of six times the amount of the duty or of 25 Baht, whichever is higher.(b) an instrument has not been duly stamped because(1) no stamp has been affixed, the tax official shall have the power to charge the full amount of duty and, in addition, to impose a surcharge of six times the amount of the duty or of 25 Baht, whichever is higher.(2) the amount of the stamps affixed is less than the amount of duty payable, the tax official shall have the power to charge the deficiency and, in addition, to impose a surcharge of six times the amount of the deficiency or of 25 Baht, whichever is higher.(3) in all other cases, the competent official shall have the power to impose a surcharge equal to the amount of duty payable or 25 Baht, whichever is higher.5.2 Punishment(1) Whoever liable to duty or required to cancel stamps fails or refuses to pay the duty or to cancel the stamps shall be punished with a fine not exceeding 500 Baht.(2) Whoever, with a view to evading payment of duty, issued a receipt of less than 10 Baht for the value received of 10 Baht or over, or divides the value received, or, with a view to evading compliance with the legal provisions on the stamp duty, willfully falsifies any instrument, shall be guilty and punished with a fine not exceeding 200 Baht.(3) Whoever intentionally puts a false date of cancellation of a stamp shall be punished with a fine not exceeding 500 Baht or imprisonment not exceeding three months or both.(4) Whoever fails to prepare or keep records of the daily total of money or price, or fails to issue a receipt immediately on demand in pursuance, or issues a receipt not stamped in the correct amount, shall be punished with a fine not exceeding 500 Baht.(5) Whoever by himself or in conspiracy with another person prevents issuance of a receipt, or fails to issue a receipt immediately upon receiving payment of money or price or issues a receipt showing an amount less than that of the money or price actually received, shall be punished with a fine not exceeding 500 Baht or imprisonment not exceeding one month or both.(6) Whoever knowing fails to extend facilities to the tax official or tax inspector in the performance of his duty, or seizure of any instruments or documents, or disobeys the summons issued by the tax official or tax inspector or refuses to give answers when questioned, or contravenes the provisions on issuing receipts or invoices or procedural directions issued by the Director-General of the Revenue Department shall be guilty and punished with a fine no exceeding 500 Baht.(7) Whoever, with fraudulent intention, has in possession a stamp known to be forged or deals in stamps which have been used or declared out of use by Ministerial Regulations shall be guilty and punished with a fine not exceeding 5,000 Baht or imprisonment not exceeding three years or both.Petroleum Income Tax (PT)Petroleum Income Tax (PT) is a direct tax, levied annually (for each accounting period of 12 months duration) on net profit of a “petroleum taxpayer”, who is carrying out the business of petroleum exploration and production. It is also levied on the disposal of profits outside of Thailand. The rules and regulations for Petroleum Income Tax are covered under Petroleum Income Tax Act and other related law. The rates, penalties, surcharge, etc. are different from that of Corporate Income tax.An accounting period is normally 12 months. The Director General may grant permission for more or less than 12 months, if appropriately justified. The first accounting period shall begin on the day that the company makes its first sale or disposal of petroleum subject to royalty. This day is considered as the beginning date of the accounting period. An accounting period may be shorter than 12 months for the following case:a)if the company takes any day as the closing date of the first accounting period:b)if the company ceases its petroleum business, the date of dissolution shall be the closing date of the accounting period:c)if the company changes the closing date of an accounting period with the approval of the Director-General.In the case the company transfers any rights under a concession prior to the beginning date of the first accounting period, this date of transfer shall be treated as the beginning and closing date of the accounting period.1. Tax basedThe term ‘petroleum taxpayer’ covers anybody who:(1)

holds a concession under petroleum law or has a joint interest in it; or

(2)

purchases crude oil produced by any concessionaire, all of which is intended for export.

A concession under petroleum law (to be obtained from Department of Mineral Resources) is required only for exploration and production of petroleum products (including crude oil, natural gas and liquid natural gas). Downstream industries including refining are not covered under Petroleum Income Tax Act. The tax is characterized by the presence of very few taxpayers.There are 2 important amendments to the Petroleum Income Tax Act (in the years B.E. 2522 and B.E. 2532) creating 3 different versions. Each Petroleum Taxpayer is covered under one or more of the three versions (referred as status of taxpayer). Filing requirement is that taxpayer should submit one return per TIN per period per status. In case a taxpayer has to file returns under more than one status, he has to do so treating each status as a separate company. (in matters of allowances, adjusting of carried forward loss, etc.)The important differences in tax calculation/remittance between the three versions of the Act are as follows:Act 2514 (status 1)

Only annual return. No need for half year return. Interest not allowed as expense. Royalty allowed as tax credit. No levy of special remuneratory benefit tax. High tax rate of 50%

Act 2522 (status 2)

Only annual return. No need for half year return. Interest allowed as expense. (but a high withholding tax of 50% on interest paid is levied. Royalty allowed as expense. No levy of special remuneratory benefit tax. Low tax rate of 35% High profit remittance tax of 23.08%

Act 2532 (status 3)

Annual and half yearly returns required. Interest not allowed as expense. Royalty allowed as expense. Additional levy of special remuneratory benefit tax. High tax rate of 50%

All Petroleum Taxpayers are required to pay withholding tax @ 50 % on profits on transfers (transfer proceeds less loss carried forward) when petroleum property or right is transferred and if the total amount of such income is not definitely determinable.While calculating net profit, following items are included as revenue:(1)

Gross Income from sale of petroleum;

(2)

Value of petroleum disposed of;

(3)

Value of petroleum delivered as payment of royalty in kind;

(4)

Gross income arising from a transfer of any property or right related to petroleum business,

if the total amount of such gross income is definitely determinable;

(5)

Any other income arising from conducting petroleum business.

The following are deductible expenses:

(1)

Ordinary and necessary expenses

(2)

Interest remitted and withholding tax paid

(3)

Value of royalty paid to the Thai Government

(4)

Value of special remuneratory benefit tax paid to Thai Government.

(5)

Capital expenditure allowance (in the nature of depreciation)

(6)

Net losses carried forward over the last 10 years

(7)

Bad debts

(8)

Donation not exceeding 1% of profit

(9)

Contribution to provident fund / pension fund

1. Tax basedTax rate is linked to the status of taxpayer. At present, the tax rates are as follows:Petroleum Income Tax(a) Petroleum Income Tax RatesAct B.E 2514 (status 1)

50%

Act B.E 2522 (status 2)

35%

Act B.E 2532 (status 3)

50%

Disposal of profits

23.08%

(b) Withholding Tax RatesFor transfer of petroleumProperty or rights

50%

(Specifically for income gained from transfer which may be able to specify certain total amount)

Payment of interest

50%

Payment of dividend

23.08%

Payment of interest

15%

Payments for other services Depends on service1. Tax paymentPetroleum companies are required to submit their annual return within 5 months from the date of closing of their accounting period. Payment of tax has to be made at the time of filing of the return.Return for profit remittance has to be submitted within 7 days from the date of remittance.In addition to the annual tax payment, petroleum companies falling under status 3 are required to submit half year return (based on estimate of profit. Under this system, the petroleum company has to estimate its annual profit and pay half of the amount of tax calculated on such basis within two months after the end of first six months of its accounting period. The estimated tax payment is creditable against the annual tax liabilities of the company3.1.2.2 Local taxA. PROPERTY TAXESProperty tax is imposed and collected annually. There are two kinds of property tax inThailand: House and Land Tax and Local Development Tax. Owners of land and/or buildingsmay be subject to either House and Land Tax or Local Development Tax.1. House and Land TaxHouse and Land Tax is imposed on owners of a house, building, structure or land that is rented or otherwise put to commercial use. Taxable property under the House and Land Tax includes houses not occupied by the owner, industrial and commercial buildings and landused in connection therewith. The tax rate is 12.5% of the assessed annual letting value of the property.2. Local Development TaxLocal Development Tax is imposed on a person who either owns land or possesses land. The tax rate varies according to the estimated land value. An appraisal will be conducted by the local authorities. Allowances are granted for land utilized for personal dwellings, the raising of livestock, and the cultivation of crops by the owner. The extent of the allowances permissible to any land depends on the location of the land.B. SIGNBOARD TAXThis tax is levied on signboards which show names, symbols or marks of business or advertisements. The rates specified in the Signboard Tax Act are computed based on signboard size and type of display (e.g., language, picture, or sign) shown in signboard, ranging from Baht 3 to Baht 40 per 500 square centimeters (but not less than Baht 200 per signboard).3.1.3 Direct Tax and Indirect Tax3.1.3.1 Direct Tax· Personal Income TaxPersonal Income Tax (PIT) is a direct tax levied on income of a person. A person means an individual, an ordinary partnership, a non-juristic body of person and an undivided estate. In general, a person liable to PIT has to compute his tax liability, file tax return and pay tax, if any, accordingly on a calendar year basis.· Corporate Income TaxCorporate Income Tax (CIT) is a direct tax levied on a juristic company or partnership carrying on business in Thailand or not carrying on business in Thailand but deriving certain types of income from Thailand.· Petroleum Income Tax (PT)Petroleum Income Tax (PT) is a direct tax, levied annually (for each accounting period of 12 months duration) on net profit of a “petroleum taxpayer”, who is carrying out the business of petroleum exploration and production. It is also levied on the disposal of profits outside of Thailand. The rules and regulations for Petroleum Income Tax are covered under Petroleum Income Tax Act and other related law. The rates, penalties, surcharge, etc. are different from that of Corporate Income tax.(Please see further detail in 3.1.2 for direct tax in Thailand)1.1.3.2 Indirect Taxa) Value added tax VAT applies to all retailers, wholesalers, manufacturers, importers, producers and others providing direct services, unless exempt under the Revenue Code. All other firms must register and adopt the VAT system. Firms with turnover not in excess of THB 1.8 million per year are exempt, as are certain other business activities, including the sale and import of raw agricultural products and related goods; the sale and import of newspapers, magazines and textbooks; and basic services, such as health and educational services, domestic transport and the leasing of immovable property. Goods exempt from import duty and destined for export-processing zones are included in this category, along with research and technical services, labor contracts, auditing and legal services. The standard VAT rate is 10%, which has been reduced to 7% until 30 September 2015 and which has two components: the standard 6.3% VAT and the municipal tax of 0.7%. The municipal tax is collected at the provincial level. A 0% VAT applies on a range of activities, including the export of goods and services wholly used outside Thailand. The 0% VAT rate also applies to the export of goods or services, i.e. any services rendered in Thailand and used abroad. VAT is payable by the 15th day of the month following the month in which VAT is collected. If a self-assessment of VAT output is required on the payment of certain income to nonresidents (primarily services or royalties used in Thailand), VAT is payable on the seventh day of the month following the month of the payment. A company that is exempt still must pay VAT on services and products it purchases, but is not entitled to a VAT refund. Such a company does not have to collect VAT on its sales or file monthly VAT forms. An exempt company, however, may do so voluntarily and thus be entitled to a VAT refund if registered for VAT purposes. Certain businesses are excluded from VAT; instead, they pay Specific Business Tax (see under 5.8, below). The VAT registrant may request VAT consolidation of headquarters and branches.b) Capital taxNonec) Real estate taxReal estate tax The municipalities levy a house and land tax and a local development tax. The house and land tax is imposed annually on the owners of a house, building structure or land that is rented or otherwise put to commercial use, at a rate of 12.5% of the actual or assessed annual rental value of the property. The local development tax, also an annual tax, is imposed on the owner of land or the person in possession of the land, with the rate depending on the appraised value of the property, as assessed by the local authorities. The rate typically ranges from 0.25% to 0.95%.1. Transfer tax Stamp duty may apply (see also Specific Business Tax below).2. Stamp duty the municipalities levy a house and land tax and a local development tax.The house and land tax is imposed annually on the owners of a house, building structure or land that is rented or otherwise put to commercial use, at a rate of 12.5% of the actual or assessed annual rental value of the property. The local development tax, also an annual tax, is imposed on the owner of land or the person in possession of the land, with the rate depending on the appraised value of the property, as assessed by the local authorities. The rate typically ranges from 0.25% to 0.95%. Stamp duty applies to any instrument, as set out in the Revenue Code. In the absence of stamp duty, such an instrument is not admissible in court. The stamp duty is necessary for the issuance of new instruments or for additions to the value of an instrument, such as an increase in funds lent under a loan agreement. Stamp duty applies on a range of documents, e.g. 0.1% on leases, the hire of work, transfers of shares/debentures, loans (capped at THB 10,000), etc.3. Customs and excise duties when a shipment arrives in Thailand, importers arerequired to file a goods declaration and supporting documents for the imports with a Customs officer at the port of entry. Imported cargo cannot legally enter into Thailand until after the shipment has arrived within the port of entry, delivery of the merchandise has been authorized by Customs, and applicable taxes and duties have been paid. It is the responsibility of an importer to arrange for examination and release of the imported cargo. In addition, depending on the nature of the imports, and regardless of value, the importers may need to obtain a permit to facilitate clearance of the imports. For certain goods requiring a permit, the relevant permit-issuing agencies should be contacted before importation. The excise tax system has been adjusted to complement the VAT system. For products subject to both taxes, the Revenue Department collects the VAT and the Excise Department collects the excise tax. Products subject to both taxes include cars, perfume, alcoholic beverages, tobacco, playing cards, air conditioners that do not exceed 72,000 BTU per hour and petroleum products. Excise taxes take the form of an ad valorem duty (a percentage of the price of the goods) or a specific charge (based on the quantity or weight of the goods). The excise tax calculation structure is expected to be amended to change the basis from “ex- factory” prices to state-recommended retail prices in the future.d) Environmental taxes Thailand does not have specific environmental tax, although certain environment-related tax measures take the form of tax privileges, such as additional deductions.e) Other taxes· Specific Business Tax Specific Business Tax applies to banking or similar transactions (regardless of whether the business operator is an individual or a company), the sale of immovable property in a profit- seeking manner and to certain businesses, such as factoring, pledges and repos. Specific Business Tax applies to the gross proceeds from the transfer of immovable property at a rate of 3.3% (including a municipal tax of 10%), a withholding tax of 1% of the gross proceeds from the transfer and a transfer fee of 2% of the appraisal value. An exemption from the tax is available in certain cases involving the whole or partial transfer of a business. A 2.75% rate applies to life insurers and pawnbrokers. A 3% rate applies to financial institutions and businesses of a similar nature; however, some transactions (e.g. interest income on debt instruments) are taxed at a rate of 0.1%. A person or entity subject to Specific Business Tax must register within 30 days from the date of commencing business and file a monthly Specific Business Tax return, regardless of whether the business generates income.· Signboard tax Signboard tax is collected by reference to the size and types of fonts of each signboard. The tax is assessed by the tax officer.(Please see further detail in 3.1.2 for indirect tax in Thailand)1.1.4 Thai tax law3.1.4.1 Internal revenue lawThe Revenue Code of Thailand. Translation from Thai script statutory tax laws of Thailand under the REVENUE CODE organizing among others personal income tax, corporate (company) income tax, tax on gifts, income tax, tax liability, tax calculation, VAT (Value Added Tax), stamp duty, withholding tax, tax assessment, appeal, tax rates, tax calculation, return of taxes. Its implementing government body is theThe content of internal revenue law of Thailand including general provision and 6 chapters are as follows;Chapter 1··Chapter 2··Chapter 3···Chapter 4·············Chapter 5·Chapter 6···(Please see further detail in 3.1.2)3.1.4.2 Edict/ Ministerial ordinance and notification/ Notification of bureau of internal revenueUnless the internal revenue law of Thailand mention in 3.1.4.1, there were a lot of notifications issued by other law of Thailand as follows;R.D.

= Royal Decree

M.R.

= Ministerial Regulation

R.CT.

= Ruling of the Commission of Taxation

N.MF.

= Notification of the Ministry of Finance

N.RD.

= Notification of the Revenue Department

N.DG.

= Notification of the Director-General of Revenue Department

N.DG.IT.

= Notification of the Director-General of Revenue Department on Income Tax

N.DG.VAT

= Notification of the Director-General of Revenue Department on Value Added Tax

N.DG.SBT.

= Notification of the Director-General of Revenue Department on Specific Business Tax

N.DG.SD.

= Notification of the Director-General of Revenue Department on Stamp Duty

The example for revenue law under the power of other law;i. Royal Decree Regarding Reduction and Exemption from Revenue Taxes (No.405) B.E. 2545ii. The Ministerial Regulation No. 186 (1991) defines Bad Debts that are eligible to be written off and the procedure to write them off ฃiii. MR. No. 310 (B.E. 2558) Issue under the Revenue Code Governing Exemption of Revenue Taxes (Exempt from income for the amount paid to purchase certain type of goods during the 25th to 31st of December 2558)iv. Royal Decree Issued under the Revenue Code Governing Exemption from Revenue Taxes (No. 596) B.E. 2559 ( issues to exempt income tax, VAT, SBT, and Stamp Duty for donations made to a certain entity in order to support sports.)v. Ministerial Notification: Currency Exchange as of 31st December B.E. 2558vi. Notification of the Director-General of Revenue on Income Tax (No. 262) Subject: The rules, procedures, and conditions for the reduction of the rate of income tax of a juristic company or partnership located in the Special Economic Zone, etc.3.1.4.1 RulingIn Thailand, both Revenue Department tax auditors and taxpayers use the Tax Ruling system to determine an issue. That is, both Revenue Department tax auditors and taxpayers request the Revenue Department's tax lawyers for a Ruling on an issue and the taxpayer's tax liability for that issue, and the vast majority of both (again) accept the Ruling as a form of "judgment".International businesses should note that Tax Rulings are not "judgments",but are in fact the opinions of the Revenue Department tax lawyers ... similar to opinions rendered by lawyers in the private sector. But whilst the legal status of Tax Rulings are only opinions, as they are opinions of Revenue Department tax lawyers (rather than opinions of private sector lawyers), for those cases that you believe the Revenue Department's tax auditors have determined an issue wrongly, they can be very powerful tools to use for defending tax audit investigation cases.Example for Tax Ruling Thailand for Thailand Export Services VAT Latest Ruling, Tax Advantage Article | October 2012

In April 2012, I alerted foreigners to Thailand's Supreme Court Ruling No 6710/2554, which ruled in favor of the Revenue Department and against a Thailand company providing goods sourcing, inspection and quality assurance services to customers in a foreign country (i.e. export services - services that are performed in Thailand and consumed in a foreign country). That Supreme Court Tax Ruling was publicly criticized by many tax academics and Tax Court Judges. The criticism was over the Supreme Court's interpretation of the consumption part of the 0% VAT rule for export services. And now the Thailand Revenue Department's lawyers have now issued a favorable tax ruling in relation to a Thailand company's export services, as follows:

Tax Ruling No Gor Khor 0702/Por/5147 Dated 21 June 2555Similarly to the Supreme Court Case, a Thailand company performed the following services in Thailand:1. Goods sourcing services;2. Goods inspection services;3. Goods quality assurance services; and4. Goods export checking services.And similarly again to the Supreme Court Case, the Thailand company provided all of the output from its services to customers in a foreign country.

The Thailand Revenue Department's lawyers ruled that as the Thailandcompany is sending its services reports to customers outside of Thailand, regardless of whether the customers may use those services reports for subsequent ordering of goods from Thailand or not, the Thailand company has the right to apply the export rate of 0% VAT to the services under Section 80/1(2) of the Revenue Code and the Director-General's Notification on VAT (No 105).This Tax Ruling seems to be almost opposite the Supreme Court's Ruling, and only time will tell if this latest Tax Ruling is a sign of new Thailand Revenue Department thinking. Even if it isn't, and the Revenue Area audit officers are still challenging you over your export services, you could use this Tax Ruling to defend your position. This Tax Advantage Article is general information only. It should not be used to determine any matter without consulting with an experienced Thailand tax advisor3.2 Personal Income TaxPersonal Income Tax (PIT) is a direct tax levied on income of a person.A person means:· an individual· an ordinary partnership· a non-juristic body of person and· an undivided estate.Taxable PersonsTaxpayers can be classified into 2 groups include “resident” and “non-resident”.3.2.1 Judgment of residents and taxable income3.2.1.1 Definition of residents“Residents” means any person staying in Thailand for a period or periods aggregating more than 180 days in any tax (calendar) year. A resident of Thailand is liable to pay tax on income from sources in Thailand as well as on the portion of income from foreign sources that is brought into Thailand.“A non-resident” means any person that has an income from sources in Thailand. A non-resident will be subjected to tax only on income from sources in Thailand.3.2.1.2 Taxable IncomeTaxable income is the amount of income that is used to calculate an individual's or a company's income tax due. Taxable income is generally described as gross income or adjusted gross income minus any deductions, exemptions or other adjustments that are allowable in that tax year.3.2.1.3 Definition of residents in Japanese tax lawIn determining the residency of a company for tax purposes, Japan utilizes the ‘place of head office or main office’ concept, not the ‘effective place of management’ concept. A Japanese company is defined as a company whose head office or main office is located in Japan in the tax law.3.2.2 Calculation of amount of tax in Thailand3.2.2.1 Total net income1. Income chargeable to the PIT is called “assessable income”. The term covers income both in cash and in kind. Therefore, any benefits provided by an employer or other persons, such as a rent-free house or the amount of tax paid by the employer on behalf of the employee, is also treated as assessable income of the employee for the purpose of PIT. Assessable income is divided into 8 categories as follows :

1) income from personal services rendered to employers;2) income by virtue of jobs, positions or services rendered;3) income from goodwill, copyright, franchise, other rights, annuity or income in the nature of yearly payments derived from a will or any other juristic Act or judgment of the Court;4) income in the nature of dividends, interest on deposits with banks in Thailand, shares of profits or other benefits from a juristic company, juristic partnership, or mutual fund, payments received as a result of the reduction of capital, a bonus, an increased capital holdings, gains from amalgamation, acquisition or dissolution of juristic companies or partnerships, and gains from transferring of shares or partnership holdings;5) income from letting of property and from breaches of contracts, installment sales or hire-purchase contracts;6) income from liberal professions;7) income from construction and other contracts of work;8) income from business, commerce, agriculture, industry, transport or any other activity not specified earlier.3.2.2.2 Tax deductionCertain deductions and allowances are allowed in the calculation of the taxable income. Taxpayer shall make deductions from assessable income before the allowances are granted. Therefore, taxable income is calculated by:

TAXABLE INCOME = Assessable Income - deductions - allowances

Deductions allowed for the calculation of PIT:Type of Income

Deduction

a. Income from employment

40% but not exceeding 60,000 baht

b. Income received from copyright

40% but not exceeding 60,000 baht

c. Income from letting out of property on hire

1) Building and wharves

30%

2) Agricultural land

20%

3) All other types of land

15%

4) Vehicles

30

5) Any other type of property

10%

d. Income from liberal professions

30% except for the medical profession where 60% is allowed

e. Income derived from contract of work whereby the contractor provides essential materials besides tools

actual expense or 70%

f. Income derived from business, commerce, agriculture, industry, transport, or any other activities not specified in a. to e.

actual expense or 65% - 85% depending on the types of income

Allowances (Exemptions) allowed for the calculation of PIT:Types of Allowances

Amount

Personal allowance

Single taxpayer

30,000 baht for the taxpayer

Undivided estate

30,000 baht for the taxpayer’s spouse

Non-juristic partnership or body of persons

30,000 baht for each partner but not exceeding 60,000 baht in total

Spouse allowance

30,000 baht

Child allowance (child under 25 years of age and studying at educational institution, or a minor, or an adjusted incompetent or quasi-incompetent person)

15,000 baht each

(limited to three children)Education (additional allowance for child studying in educational institution in Thailand)

2,000 baht each child

Parents allowance

30,000 baht for each of taxpayer’s and spouse’s parents if such parent is above 60 years old and earns less than 30,000 baht

Life insurance premium paid by taxpayer or spouse

Amount actually paid but not exceeding 100,000 baht each

Approved provident fund contributions paid by taxpayer or spouse

Amount actually paid at the rate not more than 15% of wage, but not exceeding 500,000 baht

Long term equity fund

Amount actually paid at the rate not more than 15% of wage, but not exceeding 500,000 baht

Home mortgage interest

Amount actually paid but not exceeding 100,000 baht

Social insurance contributions paid by taxpayer or spouse

Amount actually paid each

Charitable contributions

Amount actually donated but not exceeding 10% of the income after standard deductions and the above allowances

3.2.2.3 Calculation of tax payment

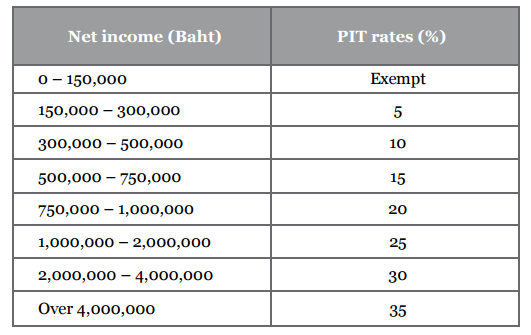

In computing tax liability by using the net income method, a taxpayer has to bring into account all assessable income arising in a tax year. The next step is to deduct from assessable income deductible expenses. Allowances are then to be deducted in accordance with the taxpayer’s circumstances. The last step is to subtract any qualified charitable contribution within the limit specified by law. Then, the tax rates, which are progressive, will be applied to any income left from all deductions.item 1.Salaries wages etc. (including exempted income) Enter the amount of your salaries and wages that you received in 2012.item 2. Less exempted income. Enter the amount from B. item 7item 3. Balance (item 1. minus item 2.) Enter the result of item 1 minus item 2.item 4. Less expense Enter the result of 40% of item 3 or 60,000 Baht whichever is lower.item 5.Balance (item 3. minus item 4.) Enter the result of item 3 minus item 4.item 6. Less allowances. Enter the amount of total allowances that you are entitled to claimitem 7.Balance (item 5. minus item 6.) Enter the result of item 5 minus item 6. A.item 8. Less contribution to education (twice the amount of actual donation made but not exceeding 10% of item 7.)If you have donated to support qualified educational projects, you may be entitled to a deduction. The qualified amount shall be filled in this line. A qualified donation to support educational projects is subject to the following conditions:a. The donation must be used:· To obtain or construct a building, a land, or a building with land for an educational institution for educational purposes, or· To obtain educational equipment, textbooks, media, educational technology, and any other equipment as prescribed by the Minister of Finance, or· To recruit professors, teachers, academic experts, or· To provide an education scholarship, an invention scholarship, a development scholarship, or a research scholarship for school students, undergraduate students, or graduate students.b. The donation must be made to:· Institutions under the royal projects, or· Institutions founded under the policy to enhance the quality of educational institutions, or· Institutions for underprivileged or disabled children, or· Educational institutions listed under the Notification of the Ministry of Education. Please contact your local revenue office or revenue branch office for more information.A qualified amount of deduction is:a. Twice the actual amount you donated.b. The maximum amount is 10% of No. 10 item 3.If you are claiming for this deduction, evidence from the educational institution(s) must be retained in order to prove your donationitem 9. Balance (of item 7. minus item 8.) Enter the result of item 7 minus item 8.item 10. Less Charitable Donations (actual amount donated but not exceeding 10% of item 9)If you have made a charitable donation, you may be entitled to a deduction.A qualified charitable donation must be made to one of the following institutions:a. Temples,b. Thai Red Cross Society,c. Hospitals (public only),d. Educational institutions (public or private),e. Government agencies,f. Charitable institutions, government employees welfare, or funds, etc. as prescribed by the Ministry of Finance.The qualified amount is:· The actual amount you donated.· The maximum amount is10 % of item 9.item 11.Net income (item 9. minus item 10.) Enter the result of item 9 minus item 10. This is your ‚net income‛. The progressive tax rate will be applied to the net income to determine your income tax.item 12. Tax computed from net income from item 11. Enter the result of your tax after the computation of tax on net incomeitem 13. Less tax exemption for first-time home buyer.If you have never owned a residence and you bought either a house with land or a condominium for the first time in 2012, you are entitled to a tax exemption subject to following conditions:a. The price of the first residence you bought is not more than 5,000,000 Baht.b. You paid for the residence and the residence is transferred during 2012.c. Your maximum amount of tax exemption is equal to 10% of the purchase price.d. You have to claim this tax exemption within 5 taxable years from the date of transfer. Additionally, the tax exemption must be divided by 5 and you have to claim the exemption for 5 years.e. You have never owned a residence before.f. You must own the residence for at least 5 years counting from the date of transfer.g. The residence has never been transferred (wholly or partly) to anyone.h. You have never claimed for:· A deduction for residence mortgage interest in No.9 item 11.· An exemption for income from sale of a residence for the purpose of buying a new residence according to Ministerial Regulation No. 241 (B.E.2546).· An exemption for income paid for a residence according to Ministerial Regulation No. 271 (B.E.2552).Example: You bought a new condominium worth 3,000,000 Baht as your first residence in 1 December 2012. Your entitlement is 300,000 Baht (10% of 3,000,000 Baht). You can claim a tax exemption of 60,000 Baht for 5 years. You can choose to start claiming for your tax exemption in your tax return for the year 2012 – 2016. If you choose to Page 12 of 35 start claiming for your tax exemption in 2012, the tax exemption of 60,000 Baht must be applied in 2012, 2013, 2014, 2015 and 2016. If in any year, the amount of your tax payable is less than 60,000 Baht, you do not get a refund.item 14.Balance (tax payable if item 12. more than item 13.) Enter of balance of item 12.minus item 13.only if the result is above 0.item 15. Withholding tax credit and tax credit for tax paid. When you received income during a tax year, the law requires the payer to withhold income tax for some types of income. In some countries, this is called ‚pay as you go‛ or ‚pay as you earn‛. In Thailand, it is called ‚withholding tax‛. The payer is also required to issue you a withholding tax certificate similar to this picture. If the payer refused to issue a withholding tax certificate, the payer is subject to a criminal penalty. You may have received many withholding tax certificates if you have received income from different payers. You will have to provide documents to the Revenue Department to prove the amount of withholding tax.item 16. Tax payable or tax overpaid Enter the result of item 14. minus item 15. Then check the box that applies to you. Check the box ‚Payable‛ if the result is higher than zero. Check the box ‚Overpaid‛ if the result is below zero.item 17. Add additional tax payable Enter the amount (if any).item 18.Less overpaid tax Enter the amount (if any).item 19.Less (tax paid in PND91) If this is your additional filing, enter the amount of tax paid from previous filing of PND91item 20. Additional tax payable/ overpaid tax Check the box that applies to you and enter the amount of additional tax payable or overpaid tax.item 21 Add surcharge (if any) Enter the amount of surcharge that you are liable to pay (if any).item 22.Total additional tax payable/ overpaid tax Check the box that applies to you and enter the amount of additional tax payable or overpaid tax. You are now at the final step of tax computation. The amount filled in this line is the actual amount of tax you have to pay or the actual amount of refund you may request.3.2.3 Declaration and payment3.2.3.1 Final income tax returnTaxpayer can lodge tax return over the internet using electronic filing, our standard processing time is 15 days. However, your tax return may take longer to process due to various circumstances, the Revenue Department would like to inform as follows.

1. Processing Time-

Your tax return is approved by the processing program, the RD will send you refund cheque within 15 days.

-

Your tax return is not approved by the processing program, the RD will not be able to refund your tax within 15 days as essential documents will be required for further assessment.

-

You relodged your tax return, the RD will not be able to refund your tax within 15 days.

1. Checking the progress of your tax return onlineYou can check the progress of your tax return online at www.rd.go.th>> “What’s news”>> “request for PND90, 91 tax refund status” (available only in Thai language)Taxpayer can cash cheque at Finance Division, 7th floor, 90 Revenue Department Building, Paholyothin 7 Rd., Samsen Nai, Payathai, Bangkok, if you reside in Bangkok. If you reside in other province, please cash you cheque at, Administration Section, Area Revenue Office.Document required are as follows;1)

Personal ID card, or passport with its copy

2)

letter of establishing non-juristic body of person, in case of non-juristic body of person

3)

authorization letter (if authorize someone else to perform the request), agent’s personal ID card and its copy.

For certain categories of income, the payer of income has to withhold tax at source, file tax return (Form PIT 1, 2 or 3 as the case may be) and submit the amount of tax withheld to the District Revenue Office. The tax withheld shall then be credited against tax liability of a taxpayer at the time of filing PIT return. The following are the withholding tax rates on some categories of income:Types of income

(baht)Withholding tax rate

(baht)1. Employment income

5 - 37 %

2. Rents and prizes

5 %

3. Ship rental charges

1 %

4. Service and professional fees

3 %

5. Public entertainer remuneration

- Thai resident

- non resident

5 %

5 - 37 %6. Advertising fees

2 %

3.2.3.3 tax paymentTaxpayer is liable to file Personal Income Tax return and make a payment to the Revenue Department within the last day of March following the taxable year. Taxpayer, who derives income specified in Income from letting out of property on hire / Income from liberal professions or Income derived from business, commerce, agriculture, industry, transport, or any other activities not specified in a. to e. during the first six months of the taxable year is also required to file half - yearly return and make a payment to the Revenue Department within the last day of September of that taxable year. Any withholding tax or half-yearly tax which has been paid to the Revenue Department can be used as a credit against the tax liability at the end of the year.3.3 Corporate income taxesCorporate income Tax (CIT) is a direct tax levied on a juristic company or partnership carrying ob business in Thailand or not carrying on business in Thailand but deriving certain types of income from Thailand.3.3.1 Taxable companies1.1 A company or a juristic partnership incorporated under Thai law.1.2 A company or a juristic partnership incorporated under foreign law1.3 A business operating in a commercial or profitable manner by a foreign government, organization of a foreign government or any other juristic person established under a foreign law.1.4 Joint venture1.5 A foundation or association carrying on revenue generating business, but does not include the foundation or association as prescribed by the Minister in accordance with Section 47 (7) (b) under Revenue Code3.3.2 Taxable yearThai and foreign companies carrying on business in Thailand are required to file their tax returns (Form CIT 50) within one hundred and fifty (150) days from the closing date of their accounting periods. Tax payment must be submitted together with the tax returns. Any company disposing funds representing profits out of Thailand is also required to pay tax on the sum so disposed within seven days from the disposal date (Form CIT 54).In addition to the annual tax payment, any company subject to CIT on net profits is also required to make tax prepayment (Form CIT 51). A company is obliged to estimate its annual net profit as well as its tax liability and pay half of the estimated tax amount within two months after the end of the first six months of its accounting period. The prepaid tax is creditable against its annual tax liability.As regards to income paid to foreign company not carrying on business in Thailand, the foreign company is subject to tax at a flat rate in which the payer shall withhold tax at source at the time of payment. The payer must file the return (Form CIT 54) and make the payment to the Revenue Department within seven days of the following month in which the payment is made.3.3.3 calculation of taxable income3.3.3.1 Tax-free incomeThe following categories of taxpayers are exempt from CIT:- Companies granted exemption from tax for a period of time by the Board of Investment under the Investment Promotion Act (1977);- Specified foundations or organizations; and- Foreign organizations under mutual agreements or diplomatic3.3.3.2 Amount of profits/lossIn the calculation of CIT of a company carrying on business in Thailand, it is calculated from the company's net profit on the accrual basis. A company shall take into account all revenue arising from or in consequence of the business carried on in an accounting period and deducting therefrom all expenses in accordance with the condition prescribed by the Revenue Code. As for dividend income, one-half of the dividends received by Thai companies from any other Thai companies may be excluded from the taxable income. However, the full amount may be excluded from taxable income if the recipient is a company listed in the Stock Exchange of Thailand or the recipient owns at least 25% of the distributing company's capital interest, provided that the distributing company does not own a direct or indirect capital interest in the recipient company. The exclusion of dividends is applied only if the shares are acquired not less than 3 months before receiving the dividends and are not disposed of within 3 months after receiving the dividends.Net losses may be carried forward for five accounting periods for offset against future profits from all sources. There is no provision for loss carry-back. Each company’s losses are dealt with separately. There is no form of group relief or relief by consolidation. A change in shareholding of a company does not affect its tax losses.3.3.4 Calculation of amount of taxIn calculating CIT, deductible expenses are as follows:1. Ordinary and necessary expenses. However, the deductible amount of the following expenses is allowed at a special rate:

- 200% deduction of Research and Development expense,

- 200% deduction of job training expense,

- 200% deduction of expenditure on the provision of equipmentfor the disabled;

2. Interest, except interest on capital reserves or funds of the company;

3. Taxes, except for Corporate Income Tax and Value Added Tax paid to the Thai government;

4. Net losses carried forward from the last five accounting periods;5. Bad debts;6. Wear and tear;

7. Donations of up to 2% of net profits8. Provident fund contributions;9. Entertainment expenses up to 0.3% of gross receipt but not exceeding 10 million baht;10. Further tax deduction for donations made to public education institutions, and also for any expenses used for the maintenance of public parks, public playgrounds, and/or sports grounds;11. Depreciation: Provided that in no case shall the deduction exceed the following percentage of cost as shown below. However, if a company adopts an accounting method, which the depreciation rates vary from year to year, the company is allowed to do so provided that the number of years over which an asset depreciated shall not be less than 100 divided by the percentage prescribed below.3.3.5 Method of declaration and payment3.3.5.1 Interim tax returnThe system is one of self-assessment. A company prepares and files its tax returns by the due dates and at the same time pays the taxes calculated to be due. The tax year for a company is its accounting period, which must be of 12months’ duration. However, it may be less than 12 months in the case of the first accounting period after incorporation, the accounting period of dissolution or after approval for a change in the accounting period has been received from the Revenue Department and the Business Development Department. CIT is paid twice in each year. A half-year return must be filed within two months after the end of the first six months of an accounting period. The tax to be paid is computed on one-half of the estimated profit for the full accounting period except for listed companies, banks, certain other financial institutions and other companies under prescribed conditions, where the tax is based on the actual net profit for the first six months. The annual tax return must be filed within 150 days from the closing date of an accounting period and credit is given for the amount of tax paid at the half-year.In addition, Thai companies can use foreign tax paid on business income or dividends received as a credit against the corporate income tax liability. The credit cannot exceed the amount of Thai tax on the income.Credit is also given for any Thai withholding tax that has been deducted at source (as mentioned above) and for the half-year tax paid.Withholding tax on foreign paymentsThere are two types of final withholding taxes imposed on the remittance of income or profits to foreign companies:Remittance of income in the form of:- brokerage, fees for services 15%- royalties 15%- interest 15%- dividends 10%- capital gains 15%- rental of property 15%- liberal professions 15%**These withholding taxes may be reduced or exempt under double tax treaties.-Remittance of branch profits is subject to 10 percent withholding tax.3.4 VATValue Added Tax (VAT) has been implemented in Thailand since 1992 replacing Business Tax (BT). VAT is an indirect tax imposed on the value added of each stage of production and distribution.3.4.1 Taxable companiesMany countries impose corporate tax, also called corporation tax or company tax, on the income or capital of some types of legal entities. A similar tax may be imposed at state or lower levels. The taxes may also be referred to as income tax or capital tax. Entities treated as partnerships are generally not taxed at the entity level. Most countries tax all corporations doing business in the country on income from that country. Many countries tax all income of corporations organized in the country.Company income subject to tax is often determined much like taxable income for individuals. Generally, the tax is imposed on net profits. In some jurisdictions, rules for taxing companies may differ significantly from rules for taxing individuals. Certain corporate acts, like reorganizations, may not be taxed. Some types of entities may be exempt from tax.Many countries tax corporate entities on income and also tax the owners when the corporation pays a dividend. Where the owners are taxed, a withholding tax may be imposed. Generally, these taxes on owners are not referred to as corporate tax.3.4.2 Tax placeA supply that does not fall into any of the specialized categories will fall within the scope of the normal tax point rules. These comprise of what are often referred to as the basic and actual tax points. To apply the actual tax point rules it is first necessary to establish if and when the basic tax point occurred.In most cases the basic tax point for a supply of goods occurs on their removal. This normally means the time of delivery by the supplier or collection by the buyer. However, some goods are supplied in situ. This will always be the case where the goods themselves are immovable. It also applies where, for example, the goods are the subject of a multiple or chain supply with delivery/collection only occurring in relation, say, to the last supply. An example of this is where goods are supplied via a finance company. For supplies that do not involve removal of the goods, the basic tax point occurs when they are made available to the customer.The basic tax point for a supply of services is when the services are performed. This normally means the point in time when the services have been completed apart from any outstanding invoicing to the customer. For more information about basic tax points.3.4.3 Method to calculate VATVAT liability = Output Tax - Input Tax"Output Tax" is a tax collected or collectible by VAT registered person from his customers when goods or services are supplied."Input Tax" is a tax charged by another registered person on any purchase of goods or provision of services. The term also includes any tax charged on imported goods.3.4.4 Tax-freeThe distinction between zero-rated and exempted goods or services is that the suppliers of zero-rated goods and services charge VAT at the rate of 0 percent, or in effect no VAT at all, on their output ,and these suppliers are able to claim all input taxes that are paid which are related to the supply. Suppliers of exempt goods and services are not charged VAT on their output, and they cannot claim any input taxes that they have already paid.3.1.4.1Businesses subject to 0 percent VAT include:i. export of goodsii. services rendered in Thailand and utilized outside Thailand in accordance with rules, procedures and conditions prescribed by the Director-Generaliii. aircraft or sea-vessels engaging in international transportationiv. supply of goods and services to government agencies or state-owned enterprises under foreign-aid programsv. supply of goods and services to the United Nations and its agencies as well as embassies, consulate-general and consulatesvi. supply of goods and services between bonded warehouses or between enterprises located in EPZs.3.1.4.2VAT Exemptions Businesses exempt from VAT include:i. small entrepreneurs whose annual turnover is less than 1.8 million bahtii. sales and imports of unprocessed agricultural products and related goods such as fertilizers, animal feeds, pesticides, etc.iii. sales and imports of newspapers, magazines, and textbooksiv. certain basic services such as:a. transportation (domestic and international transportation by way of land)b. healthcare services provided by government and private hospitals as well as clinicsc. educational services provided by government and private schools and other recognized educational institutions.d. goods exempted from import duties under the Industrial Estate law imported into an Export Processing Zones (EPZs) and under Chapter 4 of the Customs Tariff Act.3.4.5 Tax rateThe standard VAT rate is a flat rate of 7 percent. VAT is levied by the seller on the buyer. The 7 percent VAT rate on gross receipts is effective until 30 September 2012 but could increase to the normal rate of 10 percent thereafter.3.4.5.1 Tax-freeZero Percent Rate - Certain activities are liable to VAT at the rate of zero percent. Those activities include:• export of goods;• services rendered in Thailand and utilized outside Thailand in accordance with rule, procedure and condition prescribed by the Director- General;• aircraft or sea-vessels engaging in international transportation;• supply of goods and services to government agencies or state-owned enterprises under foreign-aid program;• supply of goods and services to the United Nations and its agencies as well as embassies, consulate-general and consulates;• supply of goods and services between bonded warehouses or between enterprises located in EPZs.3.4.6 Procedures of declaration and paymentAll registered VAT operators are required to account for VAT return forms on a monthly basis. Any VAT due is liable to be paid on or before the 15th day of the following month and registrants are also required to file VAT returns for self-assessed VAT within 30 days from the date the tax liability arises.All registered VAT operators have to show below detail on a tax invoicei. name, address, tax payer identification numberii. name, address of purchaseriii. serial number of invoiceiv. name, type, quantity and value of goods, servicesv. VAT computed and shown separatelyvi. date of issue.3.4.7 Tax InvoiceThailand VAT – Tax InvoiceIf your business in Thailand is registered in the VAT system, you and your Thai accountant need to pay attention to the tax invoice you receive from vendors.When you buy goods from someone who is also registered in the VAT system, they need to issue a tax invoice right when the goods are delivered. The “tax invoice” may or may not be on the same paper as “invoice” or “delivery note” or “receipt”. If they are not registered in the VAT system, they cannot issue a tax invoice and must not collect VAT from you.When you buy services, the vendors do not need to issue a tax invoice until you pay them. If you get a credit term on the transaction, they may send you an “invoice” to let you know how much you owe them. When they get paid, they need to issue a receipt and a tax invoice, which could be on the same paper.A tax invoice must at least contain the following particulars-(1) the word “tax invoice” at a prominent place;(2) the name, address and taxpayer identification number of the business issuing the tax invoice;(3) the name and address of the purchaser of goods or service;(4) serial number of the tax invoice;(5) description, type, category, quantity and value of goods or services(6) the amount of value added tax calculated on the value of goods or services which is clearly separated from the value of goods or services;(7) the date of issuance;(8) any other particulars as prescribed by the Director-General of the Revenue Department.Please make sure there is no correction made anywhere in the tax invoice even if someone has initialed it. THAI ACCOUNTANT recommends you ask the issuer to issue a new one for you if there are any mistakes on the tax invoice.3.5 Other taxes3.5.1 Special business taxBusinesses in Thailand that provide goods and services are generally subject to the Value Added Tax (VAT), which is an indirect tax and is levied against the value received or receivable from the supply of goods and services. However, certain types of businesses under the Revenue Code are subject to the Specific Business Tax (SBT), rather than the VAT. The SBT is imposed on certain businesses, such as financial services, where the difference between the production costs and the value added are not as clear as in other types of businesses. The SBT and VAT were both mandated in 1992 to replace the older Business Tax.Section 91/5 of the Revenue Code outlines the tax bases for the SBT, which differs depending on the type of business and may be either: gross receipts, interests, discounts, service fees, other fees, profits from buying and selling bills of exchange and foreign currency. The tax applies to all receivables that result from business activity, whether derived from within Thailand or outside the country.Section 91/2 subjects the following types of businesses are subject to the SBT:Type of business according to Section 91/2

Tax bases according to Section 91/5

Tax rate according to Section 91/6

Commercial Banking

(a) Interest, discounts, fees, services, gross profits from buying, selling or receiving bills of exchange or debt notes

(a) 3.0%

(b) gross profits from exchanging, buying and selling foreign currency, from issuing any bills of exchange or debt notes, and from transferring money to a foreign country

(b) 3.0%

Finance, securities and credit foncier

(a) Interest, discounts, fees, services, gross profits from buying, selling or receiving bills of exchange or debt notes

(a) 3.0%

(b) gross profits from exchanging, buying and selling foreign currency, from issuing any bills of exchange or debt notes, and from transferring money to a foreign country

(b) 3.0%

Life insurance

Interests, fees, services

2.5%

Pawnshop business

Interests, fees, and money, assets, compensation, or any valuable interest received or receivable from selling overdue pawned property

2.5%

Business with regular transactions similar to commercial banking

(a) Interest, discounts, fees, services, gross profits from buying, selling or receiving bills of exchange or debt notes

(a) 3.0%

(b) gross profits from exchanging, buying and selling foreign currency, from issuing any bills of exchange or debt notes, and from transferring money to a foreign country

(b) 3.0%

Sale of immovable property or real estate in a commercial or profitable manner

Gross receipts

3.0%

Sale of securities in a securities market

Gross receipts

0.1% Currently under exemption

Any other business prescribed by royal decree

According to royal decree

According to royal decree

There is a municipality tax of 10% imposed in addition to SBT.3.5.2 Petroleum income taxPetroleum Income Tax (PT) is a direct tax, levied annually (for each accounting period of 12 months duration) on net profit of a “petroleum taxpayer”, who is carrying out the business of petroleum exploration and production. It is also levied on the disposal of profits outside of Thailand. The rules and regulations for Petroleum Income Tax are covered under Petroleum Income Tax Act and other related law. The rates, penalties, surcharge, etc. are different from that of Corporate Income tax.An accounting period is normally 12 months. The Director General may grant permission for more or less than 12 months, if appropriately justified. The first accounting period shall begin on the day that the company makes its first sale or disposal of petroleum subject to royalty. This day is considered as the beginning date of the accounting period. An accounting period may be shorter than 12 months for the following case:a) if the company takes any day as the closing date of the first accounting period:b) if the company ceases its petroleum business, the date of dissolution shall be the closing date of the accounting period:c) if the company changes the closing date of an accounting period with the approval of the Director-General.In the case the company transfers any rights under a concession prior to the beginning date of the first accounting period, this date of transfer shall be treated as the beginning and closing date of the accounting period.§ Tax BaseThe term ‘petroleum taxpayer’ covers anybody who:(1) holds a concession under petroleum law or has a joint interest in it; or(2) purchases crude oil produced by any concessionaire, all of which is intended for export.A concession under petroleum law (to be obtained from Department of Mineral Resources) is required only for exploration and production of petroleum products (including crude oil, natural gas and liquid natural gas). Downstream industries including refining are not covered under Petroleum Income Tax Act. The tax is characterized by the presence of very few taxpayers.There are 2 important amendments to the Petroleum Income Tax Act (in the years B.E. 2522 and B.E. 2532) creating 3 different versions. Each Petroleum Taxpayer is covered under one or more of the three versions (referred as status of taxpayer). Filing requirement is that taxpayer should submit one return per TIN per period per status. In case a taxpayer has to file returns under more than one status, he has to do so treating each status as a separate company. (in matters of allowances, adjusting of carried forward loss, etc.)The important differences in tax calculation/remittance between the three versions of the Act are as follows:Act 2514 (status 1)

Only annual return. No need for half year return. Interest not allowed as expense. Royalty allowed as tax credit. No levy of special remuneratory benefit tax. High tax rate of 50%

Act 2522 (status 2)

Only annual return. No need for half year return. Interest allowed as expense. (but a high withholding tax of 50% on interest paid is levied. Royalty allowed as expense. No levy of special remuneratory benefit tax. Low tax rate of 35% High profit remittance tax of 23.08%

Act 2532 (status 3)

Annual and half yearly returns required. Interest not allowed as expense. Royalty allowed as expense. Additional levy of special remuneratory benefit tax. High tax rate of 50%

All Petroleum Taxpayers are required to pay withholding tax @ 50 % on profits on transfers (transfer proceeds less loss carried forward) when petroleum property or right is transferred and if the total amount of such income is not definitely determinable.While calculating net profit, following items are included as revenue:(1) Gross Income from sale of petroleum;(2) Value of petroleum disposed of;(3) Value of petroleum delivered as payment of royalty in kind;(4) Gross income arising from a transfer of any property or right related to petroleum business, if the total amount of such gross income is definitely determinable;(5) Any other income arising from conducting petroleum business.The following are deductible expenses:(1) Ordinary and necessary expenses(2) Interest remitted and withholding tax paid(3) Value of royalty paid to the Thai Government(4) Value of special remuneratory benefit tax paid to Thai Government.(5) Capital expenditure allowance (in the nature of depreciation)(6) Net losses carried forward over the last 10 years(7) Bad debts(8) Donation not exceeding 1% of profit(9) Contribution to provident fund / pension fund§ Tax ratesTax rate is linked to the status of taxpayer. At present, the tax rates are as follows:Petroleum Income Tax(a) Petroleum Income Tax RatesAct B.E 2514 (status 1) 50%Act B.E 2522 (status 2) 35%Act B.E 2532 (status 3) 50%Disposal of profits 23.08%(b) Withholding Tax RatesFor transfer of petroleumProperty or rights 50% (Specifically for income gained from transfer which may be able to specify certain total amount)Payment of interest 50%Payment of dividend 23.08%Payment of interest 15%Payments for other services Depends on service§ Tax paymentPetroleum companies are required to submit their annual return within 5 months from the date of closing of their accounting period. Payment of tax has to be made at the time of filing of the return.Return for profit remittance has to be submitted within 7 days from the date of remittance.In addition to the annual tax payment, petroleum companies falling under status 3 are required to submit half year return (based on estimate of profit. Under this system, the petroleum company has to estimate its annual profit and pay half of the amount of tax calculated on such basis within two months after the end of first six months of its accounting period. The estimated tax payment is creditable against the annual tax liabilities of the company3.5.3 Stamp taxStamp duties are taxed on instruments and not on transactions or persons. For the purposes of stamp duty, an instrument is defined as any document chargeable with duty under the Revenue Code. The stamp duty rules are contained in Chapter VI of Title II of the Revenue Code.

Rates of stamp duty are given in the schedule attached to the Chapter VI of Title II of the Revenue Code. The rates of duty range from 1 Baht to 200 Baht. A sample of stamp duty rates on some selected instrument is as follows:Nature of Instrument/Transaction

Stamp Duty

1. Rental of land, building, other construction or floating house

For every 1,000 Baht or fraction thereof of the rent or key money or both for the entire lease period

1 Baht

2. Transfer of share, debenture, bond and certificate of debt issued by any company, association, body of persons or organization.

For every 1,000 Baht or fraction thereof of the paid-up value of shares, or of the nominal value of the instrument, whichever is greater.

1 Baht

3. Hire-purchase of property.

For every 1,000 baht or fraction thereof of the total value

1 Baht

4. Hire of work

For every 1,000 Baht or fraction thereof of the remuneration prescribed.

1 Baht

5. Loan of money or agreement for bank overdraft

For every 2,000 Baht or fraction thereof of the total amount of loan or the amount of bank overdraft agreed upon.Duty on the instrument of this nature calculating into an amount exceeding 10,000 Baht shall be payable in the amount of 10,000 Baht.

1 Baht

6. Insurance policy

(a) Insurance policy against loss

For every 250 baht or fraction thereof of the insurance premium.

(b) Life insurance policy

For every 2,000 baht or fraction thereof of the amount insured.

(c) Any other insurance policy

For every 2,000 baht or fraction thereof of the amount insured.

(d) Annuity policy

For every 2,000 baht or fraction thereof of the principal amount, or, if there is no principal amount, for every 2,000 baht or fraction thereof of 33 1/3 times the annual income.

(e)Insurance policy where reinsurance is made by an insurer to another person.

(f)Renewal of insurance policy

1 Baht

1 Baht1 Baht

1 Baht

1 Baht1 Baht

Half the rate for the original policy7. Authorization letter i.e., a letter appointing an agent, which is not in the form of instrument or contract including a letter appointing arbitrators:

(a) authorizing one or more persons to perform an act once only.

(b) authorizing one or more persons to jointly perform acts more than once.