Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaThailand

2 Chapter Investment Environment

-

-

1 Chapter Basic knowledge

2 Chapter Investment Environment

2.1 Strong Economic in Thailand

2.2 Trade Liberalization in Thailand

2.5 Advantages of Investment in Thailand

3 Chapter Incorporation

3.1 Characteristics of business base

3.4 Investigation of entry schemes for each business type

3.5 How to establish a regional headquarters

3.6 Establishment of business base

3.7 Company liquidation and withdrawal

4 Chapter M&A

4.2 General M&A regarding to Corporate Law

4.3 Summary of applicable Laws for M&A

4.4 Difficulty of business and corporate evaluation

4.5 Foreign Investment Restriction

4.8 Securities and Exchange Act B.E. 2535

5 Chapter Corporate Law

5.1 Types of Thailand Business Structures

5.2 Annual General Shareholders’ Meeting in Thailand

5.3 Director and Board of Director

5.6 Dividend and Legal Reserve

6 Chapter Accounting System

6.1 Overview of accounting system

6.2 Person Responsible for accounting record

6.4 Problem and accounting system

6.5 Disclosure system and disclosure practice

7 Chapter Tax

7.2 Several issues on domestic tax law

7.3 File a Tax Return and Payment

8 Chapter Labor

8.1 Labor environment in Thailand

8.3 Social security system in Thailand

8.4 Points to keep in mind while having Japanese people in Japan

9 Chapter Q&A

-

-

-

Strong Economic in Thailand

■GDP and Economic growth rate

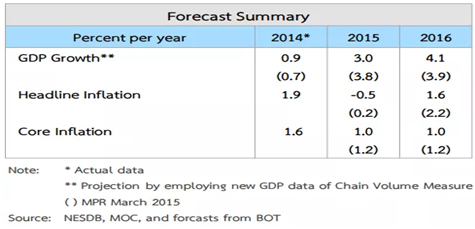

The Gross Domestic Product (GDP) in Thailand expanded 3.0 percent in the first quarter of 2015 over the same quarter of the previous year. GDP Annual Growth Rate in Thailand averaged 3.62 percent from 1994 until 2015, reaching an all time high of 19.10 percent in the fourth quarter of 2012 and a record low of -13.90 percent in the second quarter of 1998. GDP Annual Growth Rate in Thailand is reported by the Nesdb, Thailand.

.png)

.png)

Thailand is an export oriented emerging economy. As a result, manufacturing is the most important sector and accounts for 34 percent of GDP. Services constitute around 44 percent of GDP. Within services, the most important are wholesale and retail trade (13 percent of GDP); transport, storage and communication (7 percent of GDP); hotels and restaurants (5 percent of GDP) and public administration, defence and social security (4.5 percent of GDP). Agriculture also makes a significant contribution - around 13 percent of GDP. This rate was refreshed on July 30, 2015.■Expansion of domestic market and concerned inflationEven if Thailand’s GDP expanded by 3 percent from year earlier, however, it cannot meet market expectation due to the growth was boosted by the private spending and a surge in public investment. In contrast, the value of exportation was sharply low.On the expenditure side, private consumption rose 2.4 percent year on year, accelerating from a 2.1 percent growth in the previous quarter, as purchasing power of households increased. Gross fixed capital formation expanded by 10.7 percent, surging from a 3.2 percent growth in the December quarter, mainly due to a 37.8 percent expansion in public investment, both in construction and machinery. Private investment grew by 3.6 percent, moderating from a 4.1 percent in the preceding quarter. General government consumption rose by 2.5 percent, slowing from a 3.6 percent expansion in the last quarter of 2014 as an increase in purchases of goods and services (+14.7 percent) and fixed capital consumption (+5.3 percent) were unable to offset a decline in compensation of employees (-1.5 percent). Exports of goods and services grew 1.0 percent, slowing from a 4.9 percent growth in the preceding quarter, while imports increased by 2.3 percent.On the production side, the non-agricultural sector expanded by 4.1 percent, as compared to a 3.1 percent growth in the December quarter. In contrast, the agricultural sector declined by 4.8 percent, compared to a 3.2 percent fall in the preceding quarter, as yield of major crops fall. The growth of non-agriculture were seen for: the construction sector (+25.4 percent from +1.3 percent in Q4); hotels and restaurants (+13.5 percent from +3.3 percent); financial intermediation (+9.6 percent from +7.0 percent); electricity, gas and water supply (+3.8 percent from +8.6 percent); manufacturing (+2.3 percent from +1.4 percent); wholesale and retail trade, transport, storage and communication (+7.1 percent from +5.7 percent); repair of vehicles and personal household goods (+3.9 percent from +2.8 percent) and real estate (+2.8 percent from +2.6 percent). A decline in the agricultural sector was mainly contributed by a 5.3 percent fall in agriculture, hunting and forestry.On a quarter-over-quarter seasonally adjusted basis, the GDP increased 0.3 percent, significantly slowing from a revised 1.1 percent expansion in the previous period.Thailand government's economic-planning agency, NESDB, slashed its 2015 GDP growth estimate to a range of 3.0 to 4.0 percent from an earlier 3.5 to 4.5 percent. NESDB also lowered its export-value growth target to 0.2 percent from its previous estimate of 3.5 percent, mainly due to weak global economy and low agricultural prices.Thailand’s inflation rateThe inflation rate in Thailand was recorded by the Bureau of Trade and Economic Indices, Ministry of Commerce of Thailand at -1.07 percent in June of 2015. Inflation Rate in Thailand averaged 4.46 percent from 1977 until 2015, reaching all time high of 24.56 percent in June of 1980 and a record low of -4.38 percent in July of 2009..png)

.png)

■Current financial situation and related economics problemsThailand recorded a Government Budget deficit equal to 2.50 percent of the country's Gross Domestic Product in 2014. Government Budget in Thailand averaged -1.09 percent of GDP from 2003 until 2014, reaching an all time high of 2.50 percent of GDP in 2005 and a record low of -4.80 percent of GDP in 2009..png)

Government Budget is an itemized accounting of the payments received by government (taxes and other fees) and the payments made by government (purchases and transfer payments). A budget deficit occurs when the government spends more money than it takes in. The opposite of a budget deficit is a budget surplus.

By the way, Thailand Central Bank has revised the growth projection down to 3%, indicating that it has become more pessimistic about the country’s economic outlook. One of the key reason for cutting growth rate down to 3% is because of the poor exportation which expected to be -1.5 percent instead of 0.8 percent

The Thai economy is projected to recover more slowly than the previous projection mainly as a result of weaker-than-expected export growth while inflation is projected to decrease on the back of lower cost and demand pressure.

Major developments contributing to the MPC’s forecast revision include;

(1) Slower-than expected global economic recovery due to a slowdown in China and other Asian economies,

(2) A shift in global trade structure that has reduced benefit of global economic recovery on global trade growth.

(3) Higher public spending than previous assessment, especially public investment, and

(4) Increased global oil prices in the second quarter of 2015.

In light of the aforementioned economic assessment, the MPC lowered the growth projection for 2015, and judged that the risks around the central projection are skewed to the downside.

Moreover, On June 10, 2015, the MPC voted unanimously to maintain the policy rate at 1.50 percent per annum with the assessment that the earlier conduct of monetary policy has thus far eased monetary conditions, while the direction of exchange rate movement has become more conducive to the economic recovery.

Nevertheless, the Committee will closely monitor Thailand’s economic and financial developments and stand ready to utilize available policy space appropriately in order to ensure that monetary conditions are sufficiently accommodative to support the ongoing recovery. At the same time, the committee will carefully watch the possible buildup of financial imbalances that may arise during the prolonged period of low interest rates in order to maintain long-term financial stability.

So, it can be conclude that Thailand is going to recovery economic activity in a long term. Also, regarding to the government road map of Military Junta, they plans to set up an election on the middle of year 2016 which might made something better than the current situation.

-

-

-

Trade Liberalization in Thailand

Trade Liberalization in Thailand

Thailand accelerated trade liberalization in the early 1990s which the focused scheme at that time is ASEAN Free Trade Area (AFTA). Despite there was the Asian monetary crisis in 1997, Thai government still maintain its trade liberalization policy.

[Ref: http://www.ide.go.jp/English/Publish/Download/Apec/pdf/2000_c.pdf]

After that time, Thailand had reached a number of trade liberalization agreements with other countries as follows;

In the name of Thailand

1.) Thailand – India (ITFTA), Early Harvest Scheme on September 1st, 2006

2.) Thailand – Australia (TAFTA), effective date on January 1st, 2005

3.) Thailand – New Zealand (TNZCEP), effective date on July 1st, 2005

4.) Thailand – Japan (JTEPT), effective date on November 1st, 2007

5.) Thailand – Peru Early, Harvest Scheme on November 19th, 2005

6.) Thailand – Chili, signed on October 4th, 2013

In the name of ASEAN

1.) ASEAN – China (ACFTA), signed on November, 29th, 2004

2.) ASEAN – Japan (AJCEP), signed on April 11th, 2008

3.) ASEAN – South Korea (AKFTA), signed on February 27, 2009

4.) ASEAN – Australia-New Zealand (AANZFTA), signed on February 27th, 2009

5.) ASEAN – India (AIFTA), signed on August 13th, 2009

6.) BIMST-EM (Bangladesh, India, Myanmar, Sri Lanka and Thailand), signed on February 8th, 2004

[Ref: http://www.thaifta.com/engfta/Home/Agreements/tabid/168/Default.aspx]

Trade Value in Thailand

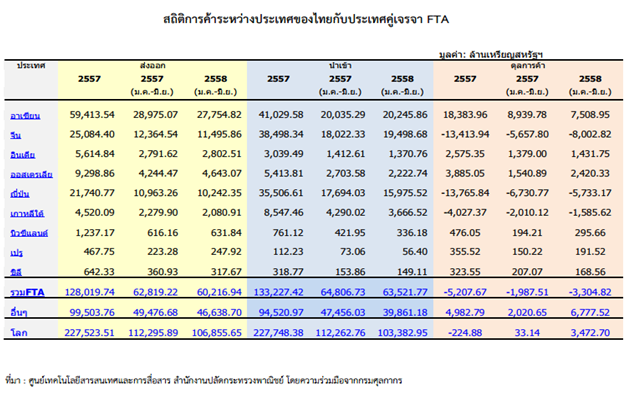

Total trade value in Thailand in period of January 2015 to June 2015 was at 210,238.59 US million dollars which decrease around 6.38 percent from the previous year. It can be categorized as follows; Total Export Value at 106,855.65 US million dollars which this part decrease from the previous year 4.84 percent and Total Import Value at 103,382.95 US million dollars which decrease to the same number of Export 4.84 percent. So, the value of surplus trade balance is 3472.70 US million dollars.

Trade Value between Thailand and FTA Dialogue Partners in 2015

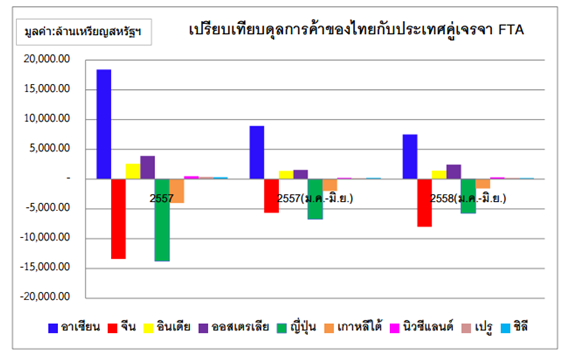

Total trade value of Thailand and Other FTA Dialogue partners in 2015 is 123,738.71 US million dollars which can be categorized to 60,216.94 US million dollars for Export and 63,521.77 US million dollars for import. So, it mean that the situation of Thailand now having the balance of trade deficit.

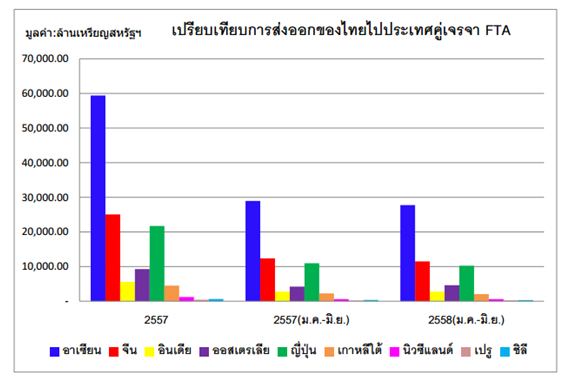

The exportation between Thailand and FTA Dialogue partners in 2558 (Jan-June)

As indicated above, it can be seen that Thailand mostly export to ASEAN which the value of exportation is approximately 27,745.82 US million dollars. This amount is lower than the previous year comparatively at 4.21 percent. China, the second target of Thailand’s exportation has the value at 11,495.96 US million dollars which definitely decrease from year 2013 and lower that the previous year around 7.03 percent. The third one is Japan which has the value on export at 10,242.35 US million dollars. Anyway, this value still lower than the previous year at 6.58 percent.

By the way, the situation on the value of importation between Thailand and FTA Dialogue partners in the period of January to June 2015 remains stable compare to the balance of trade with FTA Dialogue partners in 2015 which can be seen from a table below.Table of the trade balance between Thailand and FTA Dialogue partners

Thailand industrial competitiveness

Thailand is Southeast Asia’s second largest economy with a gross domestic product (GDP) of around USD 373 billion in 2014 (Slightly decrease from year 2013 at 385 billion).

With a free-market economy, the Kingdom has a strong domestic market and a growing middle class, with the private sector being the main engine of growth. The Thai economy is well integrated into the global marketplace, with exports accounting for over 70 per cent of the Kingdom’s GDP. Thailand also has a strong industrial sector (38.1 per cent of GDP) and a robust and growing services sector (25.7 per cent of GDP) centred on the tourism and financial services industries. Though traditionally an agrarian society and historically one of the world’s few net food exporters, the agricultural sector today accounts for approximately 8.3 per cent of the country’s GDP. Thailand continues to invest in new projects to maintain its growth.

Given the importance of exports to Thailand, it has been a leader in the region in terms of trade liberalization and facilitation with the rest of the world, starting with its Asian neighbors. Thailand is a key player in the Association of Southeast Asian Nations (ASEAN), enjoying a strategic location that provides easy access to a larger market of nearly 600 million people, which is expected to gain even more strength when the ASEAN vision of One Community materializes in 2015, making it a community of connectivity, a single market and production base. Furthermore, Thailand’s convenient access t o China and India, as well as to other East Asian countries such as Japan and the Republic of Korea, takes this huge consumer market to even bigger proportions.

.png)

In addition, Thailand’s friendly relations and expanding networks of free trade agreements with other countries have further opened up trade access to markets both within and outside the region. These, coupled with the Kingdom’s strategic positioning, have made the country a regional center for international travel and trade, as well as a hub for various industries, of which the most notable are the automotive industry and agro-industries. With a favorable investment climate, an entrepreneurial spirit and an open society, Thailand has been chosen by many businesses, media firms, as well as international organizations and non-governmental organizations as the base for their regional offices. Thailand has long been known for its open, free, and business-friendly market economy and sound macro-economic policies with fiscal and monetary prudence. To enhance the country’s competitiveness, the country has been streamlining its laws and regulations, improving its infrastructure, enlarging the pool of quality workforce and promoting research and development to promote a creative economy. Thailand therefore remains a favorite investment destination of choice for foreign investors looking for business opportunities both within Thailand and throughout Asia, attracting on average around USD 10 billion in net foreign direct investment every year.

In 2014, the World Economic Forum (WEF) ranked Thailand in terms of competitiveness, 6 places higher than the previous year (from 37 to 31). It also moved up 12 places in the macroeconomic environment pillar. Despite Thailand's constantly changing political dynamic, it has a firm economic foundation that proves its resiliency time and time again. Many long-time investors in Thailand have come to understand this unique aspect of the Thai economy. In a recent interview Honda Chairman, Fumihiko Ike, stated that he continues to be confident in Thailand's business sector.

-

-

-

Industry trades

Thailand’s Economics

The Gross Domestic Product or GDP in Quarter3 of 2014 expanded 0.6% from Quarter2 of 2014, which increased 0.4% from the previous quarter. But the 2014 Q3 gain was less than the 2.7% growth in Q3 of 2013. The Q3 quarter-on-quarter improvement was attributed to the increase in non-farm payroll, while the agriculture sector showed a decline. Domestic demand surged from household consumption of non-durable goods, and the service sector rebounded well after the political situation stabilized. In addition, non-farm payroll remained satisfactory and a declining inflation rate helped boost consumer confidence and spending, corresponding to the increase in the consumer consumption index as the overall economic outlook improved. There was more private investment in machinery. The net import and export of goods and services declined because total exports of goods and services decreased more than imports changed.

The GDP of the industrial sector in Q3 2014 dropped 0.7%, less than the 1.6% reduction in Q2 2014, but exceeding the 0.5% contraction Q3 2013. Contributing factors included lower output from the automobile sector and maintenance shutdowns of oil refineries that halted production. The electronics sector expanded because of an increase in exports. Meanwhile, the industrial sector also weakened because of the output decline in the food and beverage sector. The clothing apparel sector slumped as domestic demand decreased. Likewise, the raw materials industry contracted because of the maintenance shutdowns of some of the country’s oil refineries. Similarly, non-metals production fell in line with lower construction activity. Moreover, the capital goods and technology industries slipped because of a weakening in automobile manufacturing. However, the production of computers and electronics parts resumed expansion as market demand improved.

The National Economic and Social Development Board (NESDB) forecasted the Thai economy in 2014 will increase 1.0%, slowing from a 2.9% gain in 2013. The 2015 GDP is expected to expand 3.5-4.5%.

■Industry Structure in Thailand

Thailand’s industrial outlook for 2015: In 2015, Thailand’s industry should expand. Thai industry is forecasted to grow stemming from an improvement of the global economy and trade volume, recovery in foreign investment figures, production adjustment of the automotive industry in 2014, and decline of oil prices in the world market. The GDP is estimated to expand 2-3%, meanwhile, the manufacturing production index (MPI) should increase 3-4% in 2015.

Industry by Sector

Iron and steel industry: Production volume increased slightly 1.42% YoY, with a total output of 6,941,850 metric tons. Long-steel manufacturing expanded 3.05%, despite the prolonged political unrest. However, the private sector and the household sector had less confidence in investment and economy. Although political tensions eased during the middle of the year and a ruling government was established at the end of August, government infrastructure projects meant to stimulate production of long metal sector had not yet commenced until late 2015. Private construction remains the same. The flat steel sector climbed 2.64%, resulting from increases in coated steel (+10.18%), cold-rolled sheets (+4.18%), except hot-rolled sheets (-0.83%).

Production by the iron and steel industry should be stable in 2015 with a volume output of 6.19 million tons. The country’s demand is expected to be ranged between 0-3 %. Government infrastructure projects are an essential factor to increase demand for iron. Meanwhile, construction by the private sector slowed because consumers delayed purchases and investment in real estate.

Automotive industry: Production during the period January-October 2014 fell 25.86% when compared with the corresponding period in 2013, which recorded an output total of 1,568,300 units. The total production number of passenger cars was 614,276 units (-34.00%), 1-ton pickup trucks and pick-up passenger vehicles stood at 937,214 units (-17.60%), and commercial cars stood at 16,810 units (-64.48%). Production for exports was 944,509 units or 60.23% of total industry output. The lower output figure resulted from the country’s economic contraction and high levels of household debt. Meanwhile, automotive exports dropped resulting from the world’s economic slowdown.

According to the vehicle production plan for 2015, manufacturing is expected to increase 10% or an estimated output of 2,150,000 units, owing to 3.5-4.5% economic growth in the country and the economic improvement of trading countries. Production is expected to be in the 50-55% range for domestic sales and in the 45-50% range for exports.

Electrical appliances and electronics industry: The MPI was 278 points, a growth of 1.10% when compared with the previous year. Electronics went up 2.35% YoY, resulting from higher demand for communication gadgets. Electrical appliances decreased 0.14% YoY because purchasing power in the country declined during the first half of 2014 and consumers were more aware on spending. Nevertheless, the domestic market has improved in line with a restoration of consumer confidence in Q3 2014.

The E&E industry is expected to expand 1.2% in 2015 when compared to a year earlier. In fact, the electronics sector is predicted to grow 0.5-1%, resulting from greater demand for communication gadgets. However, the rate should not as high as the one recorded during the previous year. Meanwhile, the electrical appliances sector is expected to climb -2% from a year earlier, stemming from the improvement of both the domestic and overseas markets.

Chemical industry: Exports of chemicals for the 10-months period (January-October 2014) valued 220,053 million baht, a total of 21,514 million baht more than during the previous year. Products with the highest export value were chemical fertilizers (+38.99%), miscellaneous chemical products (+26.46%), and organic chemical products (+19.20%).

Chemical exports in 2015 are predicted to surge 6.02% from the previous year, owing to the recovery of the global economy, a clear direction of the government’s investment projects, the acceleration in approving investment promotion applications in the second half of 2014, and the official formation of ASEAN Economic Community (AEC).

Plastics industry: The export value of the industry in 2014 was 120,525 million baht. Products that increased in exports from a year earlier were monofilament, sanitary ware, and tubes or pipes (+101.13%), self-adhesive films (+24.85%), and belt conveyors or packages (+18.77%).

The export value of plastic products is expected to rise 10.01% or an estimated 132,577 million baht in 2015, stemming from the improving economies of major trading countries, such as Japan and the US, as well as the upcoming formation of the ASEAN Economic Community (AEC). In addition, the real estate sector is expected to expand, especially along the BTS Skytrain line, including the country’s borders.

Petrochemical industry: The petrochemical industry in 2014 was expected to experience an increase in export value of 3.56% and an increase in import value 0.28% from the previous year due to the economic expansion of the country, as well as in China and Japan. However, the economic recovery of the EU and US is fragile. Therefore, the industry’s manufacturers should adjust production plans that will suit both the domestic and world economies. For long-term adjustment, manufacturers should expand to new emerging markets through joint-venture partners, such as the CLMV countries (Cambodia, Laos, Myanmar, and Vietnam).

In 2015, the industry is predicted to develop according to the growth of related industries and the plastics industry. Besides, the country’s political stability is an important factor of concern.

Pulp paper, paper, and printing material industry: When compared with the previous year, the MPI of pulp paper grew 9.77%, owing to production of short fiber pulp and recycled pulp substituting imported long fiber pulp, along with the rising export volume of pulp paper. Paperboard, kraft paper, and corrugated fiberboard are expected to increase 6.58%, 5.12%, and 0.01%, respectively, because investors have regained confidence after the easing of political unrest and a new government with a clear direction since the second quarter. Moreover, the economy started to improve due to plans meant to stimulate consumption.

Production and exports of pulp paper, paper, and its products are predicted to escalate according to demand for packages from related industries in 2015. Economic improvement in Thailand, growing exports to the US, the EU, and China, and an expansion of investment in paper and package manufacturing both in the country and overseas are factors driving the industry to expand.

Ceramic industry: Production of floor and wall tiles was 163.62 million m2 in 2014, a drop of 1.18% YoY. Sanitary ware had an output of 7.31 million pieces, a decline of 2.66% YoY. The industry was affected by the first-time car buyer policy as consumers gave preference to owning cars over house repairs or improvements. Furthermore, political unrest during the previous year caused an investment contraction in the real estate sector which led to lower demand for ceramic products.

Manufacturing and sales in 2015 are likely to increase because of the government’s economic stimulus plans that encourage investment in infrastructure, such as construction of metro lines, establishing special economic zones in five border provinces (Tak, Mukdahan, Trat, Sa Kaeo, and Songkhla), and the inauguration of the AEC in 2015. These activities will attract more foreign investment and increase demand in real estate, and eventually promote the ceramic industry to grow.

Cement industry: Production of clinker was estimated at 41.59 million tons in 2014 and cement (excluding clinker) at 43.40 million tons. When compared with the previous year, the output of clinker increased 9.16% but the production of cement decreased 0.89%. The industry overall was growing even though consumption in the country did not expand as predicted, stemming from a contraction of the Thai economy and rising land prices. Therefore, entrepreneurs decided to delay expansion plans of construction projects.

The industry is predicted to grow in 2015, stemming from a rising demand of cement usage in the country, resulting from a clearer picture of the government’s infrastructure investment projects, particularly the new Skytrain lines. The private sector can invest more in real estate as land prices are not as high as land in the city or along the existing Skytrain lines.

Textile and garment industry: The industry improved in 2014, particularly wearing apparel. Thai garment manufacturers, especially sportswear producers, received purchase orders from major sporting leagues, leading to an increase in export value. On the other hand, production of textile fibers and fabrics are forecasted to drop. However, exports are expected to grow owing to demand from ASEAN markets and the reviving economies of the US and Japan. The industry gained more market share in Japan as Japan reduced orders from China in order to lessen economic risk.

In 2015, the manufacture of textiles and garments will continue to expand. The production and exports of the textile sector will be directed mainly to the ASEAN market. For garment sector, the government supports SMEs to relocate their production base to the CLMV countries (Cambodia, Laos, Myanmar, and Vietnam) in order to take advantage of abundant labor, low wages, and the generalized system of preferences (GSP) from the EU and the US. Moreover, economic expansion into other ASEAN countries will influence the domestic consumption volume of those countries.

Wood and wood furnishing industry: Production of wood furnishings in 2014 decreased according to the purchasing power of low-income consumers. Manufacturers focused on a specific product for niche markets in order to increase their product value instead of quantity. The manufacture of wood furnishings declined 3.13%, with a total output of 7.75 million pieces.

Production and sales of wood furnishings in 2015 are expected to climb resulting from an expansion of the real estate sector, leading to higher demand for home decoration products.

Pharmaceutical industry: The total output volume of medicines and pharmaceutical items was 28,252.02 tons in 2014, an increase of 6.58% YoY, due to a higher order volume from hospitals, clinics, and drug stores. Besides, the government had set reimbursement controls. Civil servants now are prescribed the cheapest medication available. Therefore, manufacturers increased their production of generic drugs in order to substitute costly imported medicines.

Production and domestic sales in 2015 are projected to climb from the previous year due to more stringent reimbursement controls regarding welfare programs for civil servants. This resulted in a surge of output in order to substitute costly imported medicines by local manufacturers.

Rubber and rubber products industry: Primary processed rubber is expected to drop 3.67% in 2014 when compared with the previous year. Tires and inner tubes of cars, pickups, trucks, buses, tractors, motorcycles, and bicycles, including retreads, should decrease 4.74% YoY, due to the sluggish economy and the first-time car buyer scheme.

The rubber and rubber products industry, particularly the inner tubes sector, should expand along with the improvements of the automotive industry. Exports continue growing, especially rubber gloves and latex gloves, which are essential in both the medical and industrial sectors. Although exports to the US and EU markets are forecasted to be weak, ASEAN markets should experience a surge.

Footwear and leather products industry: The manufacture of footwear and leather products in 2014, as compared to the previous year, which includes tanning and dressing tanned leather and luggage, handbags, and saddler, are predicted to slump due to lower demand in the country. Moreover, demand for the manufacture of related products, such as car and motorcycle seats, contracted. Meanwhile, household debt levels remained high. Production of footwear was recovering from a year earlier (2013) as exports to the US and EU have improved. However, major manufacturers relocated production facilities to other countries where they were able to compete on cost. This had an impact upon the production structure and export value of the industry.

Production and exports of footwear in 2015 should increase compared with the previous year, stemming from the economic recovery in the US. Exports of travel bags and accessories and products of tanned and synthetic leather are expected to grow owing to more orders of automotive seats and furniture. As tourist numbers are predicted to improve in 2015, the sales volume of bags and shoes should increase accordingly.

Gems and jewelry industry: Production of gems and jewelry in 2014 should decline 27.40% from a year earlier, caused by a decline of purchase orders for genuine accessories from the US and the EU. Besides, manufacturers released products that were already in stock.

In 2015, output is predicted to contract when compared with the previous year as manufacturers will export products already in stock and only produce to restore stock volume.

Food industry: Output decreased 3.07% YoY in 2014, due to lower sugar volume. Production of food, excluding sugar, increased 1.70% from a year earlier, stemming from the recovery of the country’s economy and an improving consumer economic confidence index in the second half of 2014. A resurgent global economy, including the EU, China, and Japan, from the international debt crisis and subsequent recession led to an increase of exports.

Production is predicted to grow 0-5% in 2015, stemming from an improvement of the country’s economy and greater consumer confidence. Exports are forecasted to increase in the range of minus 2.5% to 2.5%. The global economy and major trading countries, such as the US, the EU, China, and Japan, have recovered from the international debt crisis and the ensuing recession.

■Automotive Industry

Production Domestic production in the first 10 months of 2014 (Jan-Oct) was 1,568,300 units, a 25.86% decline YoY. Passenger cars totaled 614,276 units, while pickup trucks, one-ton trucks and similar vehicles tallied 937,214 units, and commercial vehicles totaled 16,840 units, a decrease of 34%, 17.6% and 64.48%, respectively. Exports numbered 944,509 units, which is 60.23% of total production. Production of one-ton pickups and similar vehicles made up 63.39% of exports while passenger cars were 36.61%. The most popular cars for export were cars with engine sizes between 1,201-1,500cc. The next most popular were eco-cars and passenger cars with engine sizes between 1,501-1,800cc.

Sales Domestic sales in the first 10 months of 2014 (Jan-Oct) tallied 719,000 units, a decrease of 35.73% YoY, comprising 303,622 passenger cars, 303,293 pickup trucks and one-ton trucks, 39,986 commercial vehicles, and 72,099 PPVs (including SUVs). These were increases of 43.36%, 31.31%, 40.83% and 1.84% YoY, respectively.

Export Automobile exports in the first 10 months of 2014 (Jan-Oct) were 932,365 units (CBU), a 1.25% decrease, for a value of 440,151.74 million baht, an increase of 3.08% for the period.

From the Center of Information and Communication Technology, the Ministry of Commerce reported automobile exports in the first 10 months of 2014 totaled 160.721 billion baht, up 3.32% YoY. Major markets for passenger car exports were Australia, the Philippines and Indonesia, making up 19.69%, 15.31% and 11.89% of total exports, respectively. Exports to the Philippines increased 46.04%, but exports to Australia and Indonesia decreased 18.02% and 33.16%, respectively. Vans and pickup truck exports for the period totaled 11,484.94 million baht, a decrease of 5.19% YoY. Major export markets were Japan, Indonesia, and Australia, making up 55.69%, 15.99% and 7.25% of total exports, respectively. Exports of vans and pickup trucks to Indonesia and Australia increased 30,630.23% and 7.60%, respectively. But exports to Japan decreased 37.72%. Exports of buses and trucks in the first 10 months of 2014 totaled 279,154.09 million baht, an increase of 5.04% YoY. The main export markets for buses and trucks were Australia, Saudi Arabia, and Malaysia, making up 22.66%, 11.75% and 4.29% of total exports, respectively. Exports of buses and trucks to Saudi Arabia and Malaysia increased 11.50% and 26.45%, respectively. Exports to Australia decreased 2.62%.

Imports Thailand vehicle imports in the first 10 months of 2014 (Jan-Oct) of passenger cars, buses and trucks were valued at 35,180.70 million baht and 13,198.66 million baht, respectively. For the same period, imports of passenger cars increased by 9.67%, but buses and trucks decreased 16.51%. Important import markets during the first 10 months were Indonesia, Japan and Malaysia, making up 28.25%, 19.84% and 19.43% of total exports, respectively. Automobile imports from Indonesia and Malaysia increased 2.97% and 58.64%, respectively. But imports from Japan decreased 5.24%. Import markets for buses and trucks during the period were Japan, Singapore and Germany, making up 23.28%, 21.90% and 12.87% of total exports, respectively. Most imports of buses and trucks were from Japan and Germany, though imports from these markets decreased 25.19% and 46.80%, respectively. But imports of buses and trucks from Singapore increased 209%.

.png)

Source: Thai Autoparts Manufacturers Association

There are many other reasons why the Thai automotive industry is an attractive base for investors in automotive parts production. Of the more than 3,000 parts and components in a typical vehicle, a sizeable portion is still sought from overseas. Opportunities exist for foreign suppliers to manufacture electronic fuel injection systems, substrates for catalytic converters, CVTs, electronic stability controls and regenerative braking systems, among numerous other products. More R&D, design and testing centers are also needed, even though major players Yamaha, Bridgestone, Maxxis and Michelin are already operating such facilities in Thailand.

Hi-Tech Vehicle Parts and Components

Projects in high-tech vehicle parts and components manufacturing are considered priority activities by the Thailand Board of Investment (BOI), which means they are exempt from machinery import duties and from corporate income tax for eight years, regardless of location.

Six automotive activities (automatic transmissions, CVTs, traction motors for automobiles such as hybrid cars and fuel cells, electronic stability controls or ESCs, regenerative braking systems, and rubber tires for vehicles), are eligible for the BOI’s special incentives promoting sustainable development, if the investor submits an application by December 2012.

The incentives for these activities include a five-year 50% reduction of corporate income tax on net profit following the expiration of the corporate income tax holiday, a 10-year double deduction of transportation, electricity and water supply costs, deduction from net profit of 25% of investment in infrastructure installation and construction costs, in addition to normal capital depreciation. Projects can be located anywhere except Bangkok.

NGV Vehicles

The Ministry of Energy supports fuel-efficient transportation through a natural gas vehicle (NGV) initiative. This initiative includes the introduction of over 10,000 natural gas-powered taxicabs, natural gas subsidization through PTT Public Company Ltd., a reduced import duty on NGV tanks from 17% to 10% in 2012, and a reduced import duty on NGV control system parts and components from 35% to 10%.

Eco-Car Parts

Eco-car parts continue to receive incentives to promote the growth of the eco-car market locally and abroad. The incentives will be applied exclusively to materials that cannot be produced locally. Duty reduction will be granted up to 90% for two years with annual review. The measure is intended to help eco-car manufacturers by lowering their production costs and reducing their burden in sourcing parts that are not available locally or produced in Thailand. This measure also encourages more investment in eco-car parts production, providing the country with economies of scale and a greater competitive advantage in the global eco-car production business. Currently, there are five BOI-promoted companies for eco-car manufacturing: Nissan March, Honda Brio, Suzuki Swift and Mitsubishi Mirage, and Toyota which will launch its model in 2013.

Passenger Cars

Although Thailand has a strong focus on pickup trucks, passenger cars receive similar favorable treatment in manufacturing promotion. The requirement for the promotion of passenger car manufacturing includes a minimum capacity for the approved models of 100,000 units per year within five years and a minimum investment, exclusive of land cost and working capital, of US$500 million (THB 15 billion). Projects that meet these criteria are eligible for a five-year corporate income tax holiday and exemption from import duties on machinery, regardless of location.

E85

The Ministry of Finance is offering three-year exemption on import duties of foreign auto parts used to make vehicles E85-ready. The ministry has also reduced the excise tax on cars using E85 to 22%, 27% and 32%, depending on engine size.

Big-Bike, 4-Stroke Engine Motorcycles (Over 500cc)

Under the new scheme, a minimum annual capacity will not be required, whereas previously it was set at 50,000 units/year. In addition, there are no restrictions on foreign ownership, compared to a minimum of 60% Thai ownership previously required. Regardless of the plant location, big-bike motorcycle manufacturing activities will be eligible for exemption from import duties on machinery. For projects that include engine manufacturing starting from machining key parts, such as cylinder heads and crankcases, the corporate income tax holiday may be extended for three to eight years, except for those located outside an industrial estate in BOI Zone 1.

Thailand’s electric industryElectrical and electronics industry in 2558 expected production will increase percentage 1-2 by electronic industry will increase 0.5-1 % according to the needs of the market group communication devices increases, and the electric power industry will increase 1-2 % because buying in the country. Increased with the growth of the economy. And the economic stimulus plan of government.

Electronics and Electrical IndustryTHAILAND: The World’s Electrical and Electronics Industry Investment Destination Constituting a nearly US$60 billion sector, Thailand’s electrical and electronics industry has thrived and expanded continuously for almost three decades. Throughout the years, the electrical and electronics industry has not only played an increasingly important role in the nation’s economy as a major export earner, but has also positioned Thailand as the regional leader in Southeast Asia. Recognizing the sustainable development of the electrical and electronics industry as a priority for the Kingdom, the Thai Government has launched proactive investment policies and measures, which have attracted investments from many multinational companies and led the industry to prosperity in Thailand. In 2011, the electrical and electronics industry contributed almost 24% of Thailand’s annual export revenues, generating US$55 billion. Major export destinations were ASEAN (17%), the EU (14%), China (14%), the US (13%), Hong Kong (12%), and Japan (11%). According to the Thailand Electrical and Electronics Institute, Thailand’s electrical appliance industry is predicted to increase 5%-7% in 2012, while Thailand’s electronics industry is forecasted to expand about 10%12% in 2012.

Thailand’s Electrical and Electronics Industry Exports, 2007-2011 60 20 2007 Billion US$ 40 0 2008 2009 2010 2011 Year Electronics Electrical Appliance Source: Thai Electrical and Electronics Institute

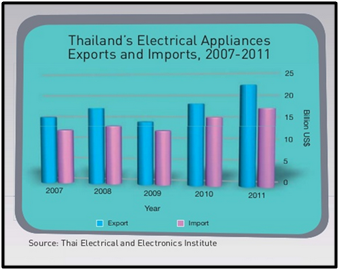

Electrical Appliance Industry Thailand is ASEAN’s largest production base in the electrical appliances sector, and is the world’s 2nd largest producer of air conditioning units and 4th largest producer of refrigerators. In 2011, Thailand’s electrical appliance exports were valued at US$22.1 billion, 9% higher than the previous year. On the other hand, imports increased by 10% to a total of US$18 billion from 2010 to 2011.

Thailand’s Electrical Appliances Exports and Imports, 2007-2011 25 20 10 5 0 2007 2008 2009 2010 Year Export Import Source: Thai Electrical and Electronics Institute 2011 Billion US$ 15The Thai electrical appliance industry has been experiencing steady growth in the past few years, and this trend is expected to continue in the coming years. Thailand’s robust manufacturing base and well-developed infrastructure, including an efficient road and ports system, make Thailand an ideal place for electrical and electronics operations. Currently, almost all of the major electrical appliance manufacturers are represented in Thailand. The Kingdom is not only a regional leader, but also a leader on a global level as Japanese, Korean, European and American multinational companies manufacture electrical appliances in Thailand. With over 800 electrical appliance factories across the country, Thailand has attracted numerous world-renowned foreign and joint-venture companies from across the globe. Japanese manufacturers constitute half of the industry: JVC, Sony, Orion, Nikon, Pioneer, Panasonic, Canon, Sharp, Hitachi, Mitsubishi, Toshiba, TDK, NEC, Stanley, Rohm, Alps Electric, Epson, Alpine, Minebea, NHK, Seiko, Sanyo and Fujitsu, among many others are represented in Thailand. Additional prominent international investors include Tatung and Acer from Taiwan; LG and Samsung from South Korea; Western Digital, Seagate, Hutchinson, Honeywell, Carrier, Emerson and Spansion from the US; as well as Europe’s Electrolux, Philips, Stiebel Eltron, Schneider, BHS, ABB and Fasco.

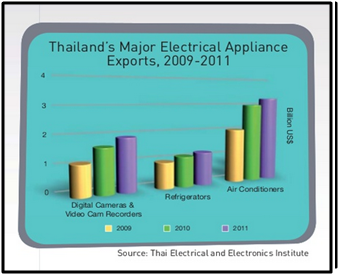

Thailand’s Major Electrical Appliance Exports, 2009-2011 4 Billion US$ 3 2 1 Air Conditioners 0 Refrigerators Digital Cameras & Video Cam Recorders 2009 2010 2011 Source: Thai Electrical and Electronics Institute

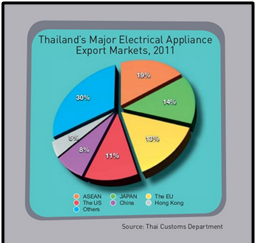

Based on the export values in 2011, Thailand’s major electrical appliance products were air conditioners, refrigerators, and digital cameras & video camera recorders. Air conditioners, which accounted for 15% of the electrical appliance industry, had the highest export value in the industry; while the export of refrigerators and digital cameras & video camera recorders increased by 10% and 12%, respectively, from 2010. The major export destinations for Thailand’s electrical appliances in 2011 were ASEAN (19%), Japan (14%), the EU (13%), the US (11%), China (6%), and Hong Kong (5%). ASEAN was the largest market for Thailand’s electrical appliances, with orders worth US$4.3 billion in 2011, a 13% growth from the previous year; followed by exports to Japan, which had an export value of US$3.2 billion, an increase of 10% from 2010.

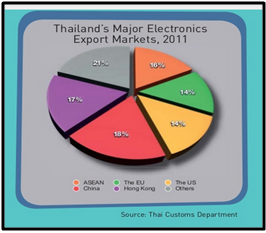

Thailand’s Major Electrical Appliance Export Markets, 2011 19% 30% 14% e 5% 13% 8% a 11% ASEAN The US Others w JAPAN China The EU Hong Kong Source: Thai Customs Department

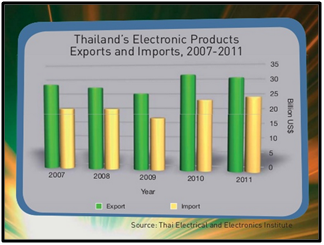

Electronics Industry The electronics industry is one of Thailand’s most prominent industries within the manufacturing sector. In 2011, Thailand’s overall trade in the electronics industry alone was worth approximately US$56 billion, an increase of 10% from 2007. Its export revenues accounted for nearly US$31 billion.

Thailand’s Electronic Products Exports and Imports, 2007-2011 35 30 25 15 Billion US$ 20 10 5 0 2007 2008 2009 2010 2011 Year Export Import Source: Thai Electrical and Electronics Institute In 2011, Thailand’s main electronics exports were hard disk drives (HDD) and integrated circuits (IC), which accounted for approximately 34% and 26% of total electronics exports, respectively. Thailand is ranked as the world’s number #1 HDD and components manufacturing base, commanding 40%-45% share of the worldwide HDD production. Major HDD producers – Western Digital, Seagate, Hitachi GST and Toshiba – have production bases in Thailand. The country holds a similarly remarkable reputation in the IC and semiconductor industries, and boasts one of the largest assembly bases for these products in Southeast Asia. Considering the increase in global demand for high-technology consumer electronics, including computers, flat panel displays, tablets, gaming consoles, and wireless devices, Thailand is the ultimate investment destination for the sector. Electronics investors will undoubtedly be able to benefit from this strong growth in demand, as well as the comprehensive support from the government of this global hub, in the electronics world. Thailand’s roster of manufacturers in this fast-growing sector is marked with numerous world-class companies, including Fujitsu from Japan, LG Electronics from Korea, Seagate from the US, and Philips Electronics from the Netherlands. These companies have established facilities for a diverse scope of purposes, from production and assembly to testing and R&D. s Parallel to the rocketing demand for computers and mobile phones, the total value of Thailand’s exported electronics amounted to approximately US$31 billion in 2011. The primary markets for these exports were China (18%), Hong Kong (17%), ASEAN (16%), the EU (14%) and the US (14%).

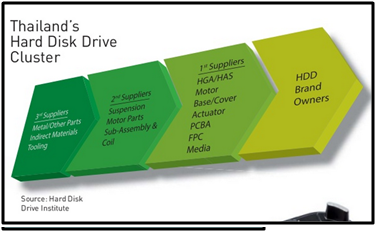

Thailand’s Major Electronics Export Markets, 2011 21% 16% 14% 17% 14% 18% ASEAN China C T c t a The EU Hong Kong The US Others Source: Thai Customs Department As a result of the sustained growth in electronics production and exports, an increase in electronic imports was also observed, especially for semiconductors, discreet components and electronics subcomponents. The total value of electronics imported into Thailand in 2011 was approximately US$25 billion. Hard Disk Drives (HDD) The HDD industry has long held paramount significance for the country, as Thailand has supplied nearly half of the world’s HDDs since 2005. In 2011, Thailand’s total computer components exports (including HDD) were valued at US$17 billion. Thailand’s HDD exports alone totaled US$10 billion in 2011, represented 62% of total computer component exports. This industry will continue to profit from the forecasted 7.7% growth of global HDD shipment in 2012. The competitiveness of Thailand’s HDD industry is derived from a deep network of world class supporting industries manufacturing most of the parts and subcomponents utilized in the assembly of final HDDs.Concentrated in the country’s central and northeastern regions near Bangkok, Thailand’s HDD cluster development program gives companies the ideal combination of efficiency, cost-savings and readily-available expertise. Within the various clusters, HDD producers in Thailand are divided into different tiers, as illustrated below:

“Data creation is expected to grow by 44 times in the next decade, but storage capacity for that will increase by about 30 times. Thus, this gap adds up to a very significant demand for digital storage.” -John Coyne, President and CEO of Western Digital Corporation-

“Data creation is expected to grow by 44 times in the next decade, but storage capacity for that will increase by about 30 times. Thus, this gap adds up to a very significant demand for digital storage.” -John Coyne, President and CEO of Western Digital Corporation-

Key Players in HDD Assembly and Components in Thailand: HDD-Part Producers: • Alps Electric • Hutchinson Technology •Magnacomp Precision • Minebea • NHK• Nidec•Nitto Denko HDD Producers:• Hitachi• Seagate• Toshiba• Western DigitalIntegrated Circuits (IC) Integrated Circuits is Thailand’s largest electronics import and its second largest electronics export. Ranking in order of importance, the major export markets for Thailand’s ICs in 2011 are: Hong Kong, Singapore, Japan and China. Considering the rising demand for electrical apparatuses and electronics of all types, the IC industry will certainly prosper. This segment of the electronics market features excellent business opportunities for prospective investors, as there currently exists a trade deficit in the sector. According to Thai Electrical and Electronics Institute, the value of ICs imported into Thailand over the last decade is greater than that of any other electronics import. In 2011 alone Thailand imported US$10 billion worth of ICs.

Key Players in the IC cluster in Thailand: IC Design:• Rohm LSI• Silicon Craft Technology Lead Frame:• Rohm Mechatech• SumikoLeadFrame• TSP-T• Yamakin

Testing:• Microchip•Maxim IntegratedAssembly:• Circuit Electronics• Hana Semiconductor• Microchip• NXP• Spansion• MillenniumMicrotech • Oki• Rohm Integrated System• Sanyo Semiconductor • Sony Device Technology• Stars Microelectronics• Stats ChipPAC • Thai NJR• Toshiba Semiconductor• UTAC Thai• Vigilant Technology

Opportunities

HDD and IC As the world’s largest HDDs and components producer, Thailand’s suppliers benefit from first class industrial clusters. In fact, almost all of the major world players in the HDD manufacturing industries can be found within a 250-kilometer radius of Bangkok. Over the past years, Thailand has proven itself to be an extremely attractive location for the assembly and testing of HDDs, ICs and electronic subcomponents, such as printed circuit boards (PCBs). Although the electronics market in Thailand is mature and well-developed, there remain areas with high market potential that manufacturers considering to expand their market can explore. For example, many key components of the upstream electronic value chain, including semiconductor devices, ICs, and discrete components such as diodes and transistors, are still currently imported from abroad, primarily from Korea, Japan, Taiwan, and Singapore. Manufactures can easily capture a new market and generate a new source of profit, as they look into manufacturing the above components locally in the country. In addition, IC design and related activities offers a burgeoning field of opportunity, particularly in wafer design, where there is currently little or no domestic production. The government extends generous support to relevant organizations and institutes by organizing human resource development training programs and conducting research on their behalf.

RFID Thailand is at the forefront of cutting-edge technologies, with radio-frequency identification (RFID) being no exception. The RFID market in Thailand isCurrently valued at about US$26.1 million, and has great potential to become a major production center in Asia, especially for inlay and coil parts used in RFID. In 2010, the value of the entire worldwide RFID market was approximately US$6.4 billion, and is projected to grow at a CAGR of 19.5% through 2014. Across the globe, the Radio Frequency Identification (RFID) industry has in recent years experienced unprecedented growth in almost every sector in which the technology is used.

Automotive Electronics With the ubiquitous presence of automobiles and car owners’ ongoing quest for sophisticated gadgets and electronic applications in vehicles, the automotive electronics industry represents a market brimming with potential and opportunities. The global market for automotive electronics is projected to reach US$243.7 billion by 2015, registering a CAGR of 6.4% during the period 2006-2015.Various sectors across the industry are anticipated to undergo strong volume growth, especially for side-impact airbags in the passive restraint market. Within the automotive electronics market, the most rapid growth will be experienced in the area of entertainment. In addition, demand for sophisticated driver-assistance systems such as collision avoidance, night vision, and lane departure has been growing. With its many advantages, Thailand is extremely attractive for system and component suppliers, as companies seek to enhance cooperation between companies and cope with cost pressures. Capturing a spot on the list of the world’s top fifteen automobile manufacturing countries, Thailand is striving to enter the top ten. This has been a strong driving force behind the development of all relevant supporting industries, including automotive electronics and parts. At the same time, the global demand for OEM automotive electronics is projected to grow 12.3% annually, escalating to US$174 billion in 2014.

Why Thailand Thailand offers a number of unique advantages for electrical appliance and electronics producers. These include:

Competitive workforce: Currently, over 400,000 people are employed in Thailand’s electrical and electronics sector. Indeed, the well-qualified, but extremely affordable workforce is a considerable attraction for many investors. Over 60 public and private engineering institutes across the country are accredited by the Council of Engineers. In addition, Thailand offers 152,000 certified engineers, with a new inflow of approximately 20,000 engineering graduates joining the workforce each year. Advancing the competitiveness and technical capabilities of the workforce has always been a main focus of the Thai Government. To ensure an adequate supply of qualified personnel for the industry, the BOI and the Ministry of Education have implemented a Human Resources Development Plan. Additionally, Thailand offers several other resources for technical training, including: • The Thai Microelectronics Center (TMEC), established by the Ministry of Science and Technology in 1998; • The Western Digital HDD Technology Training Institute (HTTI), an institution established through the cooperative efforts of Thailand’s National Electronics and Computer Technology Center (NECTEC) and Western Digital; and • NECTEC’s Industry/University Cooperative Research Centers in 3 areas: 1. HDD Advanced Manufacturing – The Institute of Field Robotics (FIBO), King Mongkut’s University of Technology Thonburi 2. HDD Components – The Engineering Faculty, KhonKaen University 3. Data Storage Technology and Application – King Mongkut Institute of Technology Ladkrabang

Access to markets: The Free Trade Agreements between Thailand and various countries, such as Australia, New Zealand, India, Japan and members of ASEAN, gives Thailand, and its foreign investors, a considerable advantage in reaching out to the different markets in the vibrant electronics industry. Under the ASEAN Free Trade Agreements (AFTA), most parts and finished electronics exported throughout ASEAN have been tariff-free since 2010. The establishment of the ASEAN Economic Community (AEC) in 2015 will only further enhance Thailand’s attractiveness. The AEC will serve as a massive single market that is fully integrated into the global economy with equitable economic development. The 10 member states of ASEAN collectively offer close to 600 million consumers. The AEC will open new doors to manufacturers by transforming ASEAN into a region with free movement of goods, capital, services, investment and workforce.

Excellent logistics systems: Thailand boasts world-class infrastructure, including state-of-the-art ports, airports and communication facilities. Suvarnabhumi International Airport and Laem Chabang Deep Sea Port offer manufacturers the transportation foundation they need for their export operations. The 225 km of inter-city motorways – currently in expansion – linking Bangkok to other regions of the country, also facilitate overall domestic transportation. In addition, Thailand is a hub of transportation in the Southeast Asia region; the perfect route through the east-west and north-south corridor that can distribute products to nearby countries including Laos, Cambodia, Vietnam, Myanmar, Malaysia, Singapore and also southern China from the north and northeast of the Kingdom.

Development of electronics clusters: In an effort to promote productivity and efficiency in the industry, the government has been proactive in encouraging the development of electronic clusters. Proximity between firms and their input suppliers within the clusters enhances communication and facilitates flow of goods. At the same time, clustering helps to reduce logistics costs through improved supply chain management. Manufacturers also benefit from shared core technological innovations and human resource development programs.

“Thailand is a good operating base for us due to being the center of the Indochinese peninsula. Here we have quick access to export markets in surrounding countries. Additionally, Thailand’s infrastructure is well established. A lot of suppliers have already shifted their production here.” -Mr. Hirotaka Murakami, CEO of the Panasonic Group of Companies in Thailand-

Developed Network of Supporting Organizations Government and organizations supporting the growth and competitiveness of the electrical and electronics industry in Thailand include:

The Electrical and Electronics Institute (EEI): Founded in 1998, the EEI is an autonomous institute under the Ministry of Industry Industrial Development Foundation. It promotes and supports the development and export of electrical and electronic products, as well as serves as a center of information for the industry.

The Hard Disk Drive Program: The Hard Disk Drive Program is operated under the cooperation of the National Electronics and Computer Technology Center (NECTEC), the National Science and Technology Development Agency (NSTDA), the International Drive Equipment and Manufacturers Association (IDEMA), the Electrical and Electronics Institute (EEI), the Asian Institute of Technology (AIT), Institute of Field Robotics (FIBO) and the Board of Investment of Thailand (BOI). Other supporters include Seagate and Western Digital. The key aim is to enhance the HDD cluster and strengthen the industry in Thailand through the development of: 1. Human resources; 2. Technology in four major branches: Material & Metrology, ESD/EOS & Contamination, Automation, and High Precision Mold/Die; 3. Supply chain of supporting industries; and 4. Policy and investment incentives.

The National Electronics and Computer Technology Center (NECTEC): NECTEC, an organization under the National Science and Technology Development Agency (NSTDA), is mainly responsible for undertaking, supporting and promoting the development of electronics and computer technologies through research and development activities. NECTEC also provides linkages among research communities and industries through the established industrial clusters.

Research Centers:

The Thailand Science Park (TSP), operated by the National Science and Technology Development Agency (NSTDA), serves as the hub for industrial R&D activities of private sectors. It is also home to national research centers, such as NECTEC, and is equipped with cutting-edge facilities.

Board of Investment (BOI)

Incentives

Thailand Board of Investment offers a wide range of fiscal and non-tax incentives for investments based on location. Tax-based incentives include exemption or reduction of import duties on machinery and raw materials, and corporate income tax exemption and reduction. Non-tax incentives include permission to bring in foreign workers, own land and take or remit foreign currency abroad. Under the BOI’s program of Investment Promotion for Sustainable Development, projects in 12 electronics and electrical industry activities that apply for BOI incentives prior to the end of 2012 for any location except Bangkok are eligible for a special package of incentives, including • Exemption of import duties on machinery • Corporate income tax exemption 8 years with no cap • 50% reduction of corporate income tax for 5 years from the expiry date • Double deduction of public utility costs for 10 years • Deduction from net profit of 25% of the investment in infrastructure installation and construction cost in addition to normal capital depreciation for 10 yearsThe BOI also has a special promotional package for projects in activities related to production of all electronics, electrical appliances, and parts. Approved projects in these activities are entitled to receive following rights and benefits. • Exemption of import duty for machinery all zones throughout the period of the promoted status. • Exemption from corporate income tax as follows; - 5-years corporate income tax exemption if the projects located in zone 1 - 6-years corporate income tax exemption if the projects located in zone 2 - 7-years corporate income tax exemption if the projects located in promoted Industrial zone or Industrial Estate - 8-years corporate income tax exemption if the projects located in zone 3 • Investment in replacement machinery using higher technology used in the production of Integrated Circuit (IC), HDD and parts, are regarded as the part of investment promoted projects. • Those applying for investment promotion must submit applications according to the criteria specified by the Office of the Board of Investment, as well as a specified plan for raw materials and parts usage.

-

-

-

Investment Environment

This chapter indicates the environment of doing investment in Thailand which many details were being summarized in many topics as bellows;

■Business Environment in 2015

First of all, the difficulty of doing business in Thailand can be seen in the aggregate ranking on the ease of doing business based on indicator sets that measure and benchmark regulations applying to domestic small to medium-size businesses through their life cycle. Economies are ranked from 1 to 189 by the ease of doing business ranking.

This year 2015's report presents results for 2 aggregate measures: the distance to frontier score and the ease of doing business ranking. The ranking of economies is determined by sorting the aggregate distance to frontier (DTF) scores. The distance to frontier score benchmarks economies with respect to regulatory practice, showing the absolute distance to the best performance in each Doing Business indicator.

An economy’s distance to frontier score is indicated on a scale from 0 to 100, where 0 represents the worst performance and 100 the frontier. The 10 topics which have been brought to consider are starting a business, dealing with construction permits, getting electricity, registering property, getting credit, protecting minority investors, paying taxes, trading across borders, enforcing contracts and resolving insolvency.

The average score of ease of doing business ranking and the distance of frontier score of Thailand year 2015 can be seen as follows;

The average score of ease of doing business ranking and the distance of frontier score of Thailand year 2015 can be seen as follows;.png)

“Thailand continues its efforts to reduce the cost and time of doing business. This, combined with reforms aimed at improving skills and promoting greater competition in the services sector, would promote greater investment and improve business operations,” (Kirida Bhaopichitr, World Bank Senior Economist for Thailand.)

Thailand also made its paying taxes less costly by reducing the corporate profit tax to 20%.

“Government agencies in Thailand have been collaborating to promote a friendly business environment,” (Annette Dixon, World Bank Country Director for Thailand.) “This, along with other measures such as improving the quality of education and promoting innovation, will help Thailand attract investors and remain competitive.”

The ranking in each topic indicator for the ease of doing business in Thailand can be seen by figure bellows; (Scale: Rank 189 center, Rank 1 outer edge)

.png) The ranking of distance to frontier scores -Thailand.

The ranking of distance to frontier scores -Thailand..png)

In order to reach the conclusion, it is needed to compare Thailand with others countries. It is better to compare with the neighbor countries of Thailand such as Indonesia, Lao, Myanmar and Philipphines. The summarized is as bellows;

The table above shows that business environment in Thailand is quite good comparing with the other neighbor countries. Malaysia and Singapore are the most competitive economic countries with Thailand. By the way, this table did not include Vietnam which has becomes one of competitive country as well.

■Foreign Direct Investment

Foreign direct investment has been an important element of Thailand's economic development process and the country is an important FDI destination. In terms of investment, the country offers an attractive and modern legal framework and its economy benefits from the regional dynamism. According to the UNCTAD World Investment Report 2014, since 2012 Thailand has been among the 8 priority destinations for foreign investment for the period 2014-2016. It is the 7th largest FDI recipient in East and South-East Asia. After having slowed down due to the unfavorable international context, FDI flows have again been rising, despite a series of natural disasters and political instability. In anticipation of the new investment policy and after political stability had been restored in the second half of 2014, demands recorded by the Board of Investment reached record levels; the number of registered projects increased by 73% and their value by 117% compared to 2013. In 2015, the government's new seven-year strategy to stimulate investment should further encourage FDI.

.png)

The trend of Foreign Direct Investment (FDI) in Thailand during the past years is clearly that the trend was increasing from 2008 to 2013. Even though, the politic situation in Thailand was not well in 2014, however, it had less effected to FDI. The trend of FDI in Thailand can be seen as bellows; (currency scale: THB Million)

By the way, the number of projected that got approved by BOI in 2014 was lower than the previous year. This is because the amendment of approval process of BOI, so that many projects still on the process of approval. However, BOI said they are trying to approve the submitted projects soon in order to regain the confidence of investor.

.png) The overview of Thailand Foreign Direct Investment is as below;

The overview of Thailand Foreign Direct Investment is as below;.png)

This table indicates that Thailand is recovering of its business attraction. The result of FDI is quite good after the political confliction in the first quarter of 2015 the amount of investment was up to 2,616.02 USD million. For now, the status of FDI in Thailand dropped to 1,665.01 USD million.

■Foreign Direct Investment inflows of Thailand s’ neighbor countries

In the past decade, the FDI of neighbor countries of Thailand such as Vietnam, Myanmar, Laos and Cambodia were far behind from Thailand. By the way, it can be seen that in past year, all of these countries had a greatly developing. It is evidence by many Japanese companies are now shift theirs investment to Vietnam which Thailand and China become less attractive due to the regulation that fix the minimum salary and also the politic problem that has effected to the investment from foreign investor.

Vietnam

In 2013, Japanese capital flow to China dropped to $6.50 billion, less than half the $13.48 billion Japanese investment China attracted in 2012. Similarly in Thailand, in 2011 Japanese investment amounted to $7 billion, while in 2013 that number dropped to $2.5 billion, according to the Business Times, a Vietnamese newspaper.

Vietnam, on the other hand, experienced the opposite trend. Foreign investment increased from just $169 million in 2010 to $4.45 billion in 2013, including a number of high-profile projects backed by Japanese companies like the $2.8 billion Nghi Son petrochemical oil refinery, the $650 million Bridgestone’s project, and the $175 million Panasonic Industrial Devices project.

The graph below indicates FDI of Vietnam in the past years. It shows that Vietnam FDI is quite higher if comparing with Thailand. However, the trend of its FDI dropped in some periods. As mentioned above, Japanese companies shift investment to Vietnam, so it increased its FDI dramatically.

.png)

Singapore

Foreign Direct Investment in Singapore decreased to 16,161.12 USD Million in the first quarter of 2015 from 17,287.40 USD Million in the fourth quarter of 2014. Foreign Direct Investment in Singapore averaged 7,371.95 USD Million from 1995 until 2015, reaching an all time high of 17,287.40 USD Million in the fourth quarter of 2014 and a record low of -3,135.37 USD Million in the second quarter of 2003. So, it obvious that Singapore had much higher amount of FDI than Thailand did. The reason is that Singapore is now has a high quality labor force, even though the cost of wage is higher comparing with Thailand.

.png) The ease of business ranking of Singapore is much higher due to many reasons. Singapore has been the developed country for many years. Also it has good infrastructure such as transportation, logistic systems, other utilities and facilities which necessary for establish a new business. However, there is some sector that Singapore cannot provide a good service if comparing to Thailand such as Automotive sector which will be discussed in next topic later.MalaysiaRegarding to the ease of business ranking and the distance to frontier (DIF), it can be said that both countries are competing in a same level. However, in the past two year, Malaysia Foreign Direct Investment dropped dramatically since 2013 and keeps staying at the low investment rate as the graph below;

The ease of business ranking of Singapore is much higher due to many reasons. Singapore has been the developed country for many years. Also it has good infrastructure such as transportation, logistic systems, other utilities and facilities which necessary for establish a new business. However, there is some sector that Singapore cannot provide a good service if comparing to Thailand such as Automotive sector which will be discussed in next topic later.MalaysiaRegarding to the ease of business ranking and the distance to frontier (DIF), it can be said that both countries are competing in a same level. However, in the past two year, Malaysia Foreign Direct Investment dropped dramatically since 2013 and keeps staying at the low investment rate as the graph below;.png)

The graph shows the latest FDI on July 2015, the amount was 2,894.72 USD million which stays in the same level as Thailand.

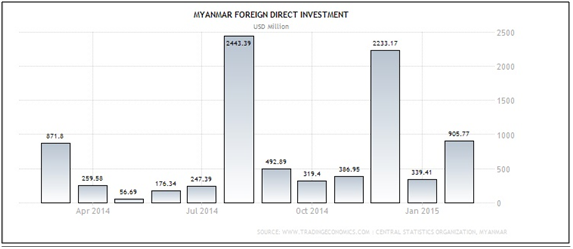

Myanmar

Myanmar is one of developing country which had just opened its country for foreign investment in the beginning of 2013. It has got good feedback from foreign investors that seeking opportunity to invest in Myanmar.

The trend of FDI increased a lot in the last quarter of 2014 and the first quarter of 2015 up to 2,233.17 and 905.77 USD million. By the way, it is a good sign to Myanmar. Although, there is some burden that Myanmar is ranked as the most difficult country for starting a business as mentioned in the ease of doing business ranking above

Indonesia

It is interesting that the trend of Malaysia FDI keeps increasing dramatically since 2012 and up to 6,290 USD million in 2015. According to the UNCTAD 2014 World Investment Report, Indonesia is one of the three most attractive destinations for multinational companies for 2014-2016, ahead of India and Brazil. In terms of FDI inflows, Indonesia was ranked 4th among East-Asian countries, after China, Hong Kong and Singapore.■Foreign Investment inflows in each industry.According to the Bank of Thailand statistic 2014, it show that top three industries are A. Manufacture of motor vehicle, trailer and semi-trailer, B. Financial and Insurance activities, C. Real estate activities and D. Wholesale and retail trade, repairing of motor vehicles and motorcycles as the table below;Also, the projects of foreign investment which have been applied to get promotion from Board of Investment (BOI) of Thailand shows that a project relating to Metal product and Machinery is the most attractive sector for investing in Thailand

It is interesting that the trend of Malaysia FDI keeps increasing dramatically since 2012 and up to 6,290 USD million in 2015. According to the UNCTAD 2014 World Investment Report, Indonesia is one of the three most attractive destinations for multinational companies for 2014-2016, ahead of India and Brazil. In terms of FDI inflows, Indonesia was ranked 4th among East-Asian countries, after China, Hong Kong and Singapore.■Foreign Investment inflows in each industry.According to the Bank of Thailand statistic 2014, it show that top three industries are A. Manufacture of motor vehicle, trailer and semi-trailer, B. Financial and Insurance activities, C. Real estate activities and D. Wholesale and retail trade, repairing of motor vehicles and motorcycles as the table below;Also, the projects of foreign investment which have been applied to get promotion from Board of Investment (BOI) of Thailand shows that a project relating to Metal product and Machinery is the most attractive sector for investing in Thailand.png)

A trend of foreign company, Japanese company for example, show a result in the same way. Moreover, it can be seen that Japanese companies invest in this project most such as Toyota, Honda and so on.

A trend of foreign company, Japanese company for example, show a result in the same way. Moreover, it can be seen that Japanese companies invest in this project most such as Toyota, Honda and so on..png)

It can be conclude that the industries relating to machinery is the most interesting for foreign investors. This is because when a company investing in Machinery sector which materials can be found in Thailand. So that, it can reduce the cost of the Company. Also, mostly industries locate near border of Thailand or next a port of shipment to reduce the cost of transportation.

-

-

-

Advantages of Investment in Thailand

■Cheap and Quality labor force

Wages

Under the proposed change, Provincial Wage Committees will consider the economic development and cost of living for each province and will make submissions in respect of the appropriate minimum wage for each province. The Wage Committee will consider the Provincial Wage Committees’ submissions at its October 2015 meeting and set the new 2016 provincial minimum wages, subject to no provincial minimum wage being set lower than 300 Baht. Public information on the proposed changes indicates that a Guideline will be determined and issued by the Wage Committee to standardize the process of making minimum wage determinations in the future.

.png)

.png)

Quality of labor force

■Manufacturing base of Asia

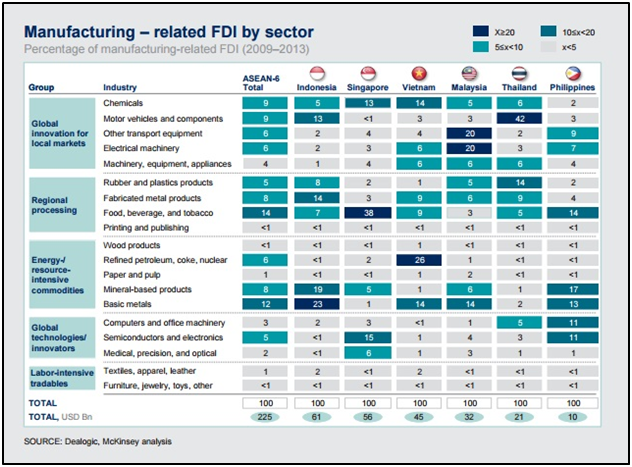

.png) According to the table above, it can be seen that Thailand is the largest manufacturing base for Motor vehicles and components. As mentioned before, the main investor who came to invest in this manufacturing most is Japanese investors.

According to the table above, it can be seen that Thailand is the largest manufacturing base for Motor vehicles and components. As mentioned before, the main investor who came to invest in this manufacturing most is Japanese investors.Motor vehicle and components manufacturing

Chemicals

Food, beverage, and tobacco

■Fulfilled Infrastructure

Therefore, it can be concluded that Thailand is the manufacturing hub for motor vehicles and components in the ASEAN region, and the automotive industry accounted for 42 percent of Thailand’s FDI from 2009 to 2013. Thailand has built a thriving ecosystem of manufacturers and assemblers, including BMW, Ford, Honda, Mazda, Mitsubishi, Nissan, and Toyota. Its long history of automotive manufacturing coupled with strong government support has created a relatively low-cost but skilled workforce in the sector. Moreover, it has built a robust cluster of local suppliers and supporting vehicle component industries. In fact, greenfield investment in tire manufacturing generated most of the FDI in Thailand’s rubber and plastics industry. Although growth has stalled in 2014 in the wake of Thailand’s political unrest, the industry enjoys solid long-term prospects as incomes rise and consumers across the region can afford cars for the first time.

■Investment Issue in Thailand

■Investment Issue in Thailand

-