Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaMongolia

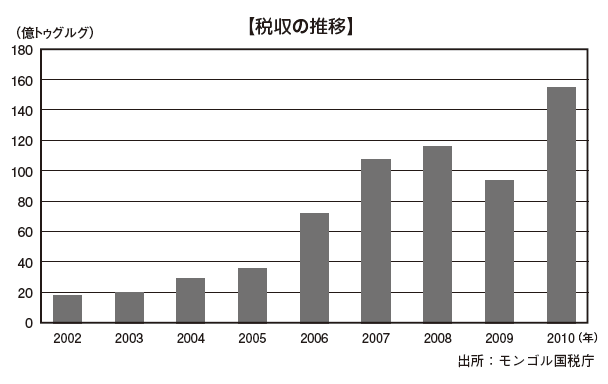

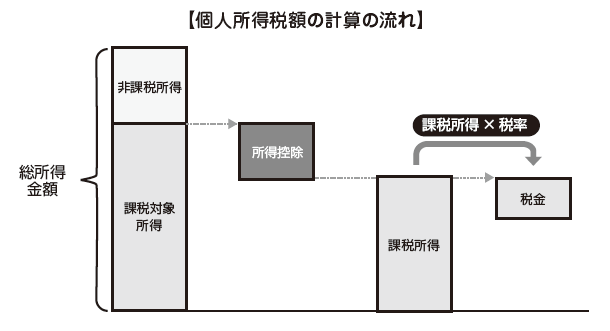

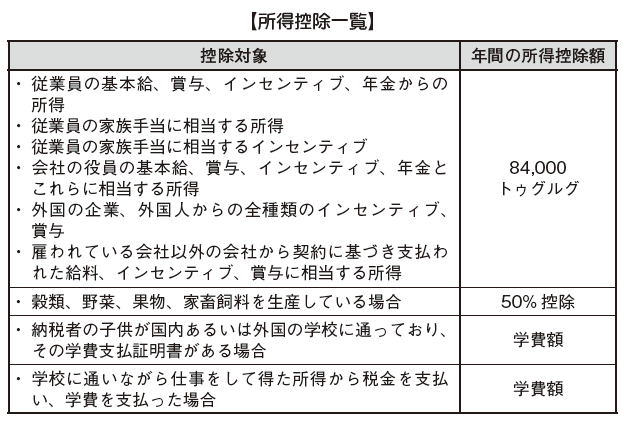

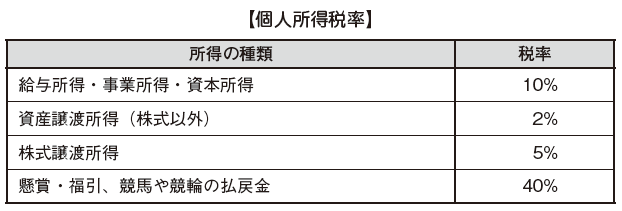

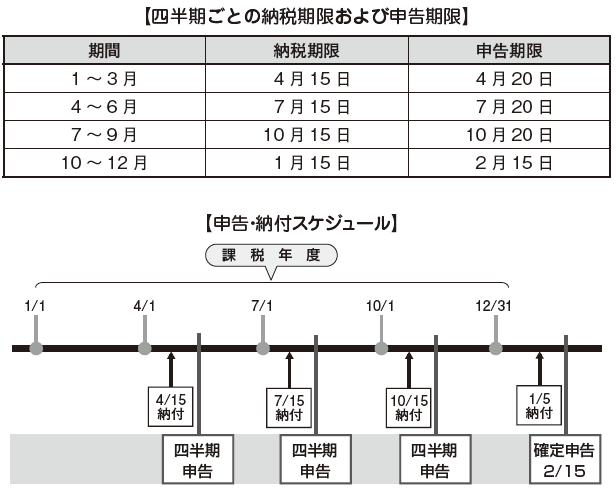

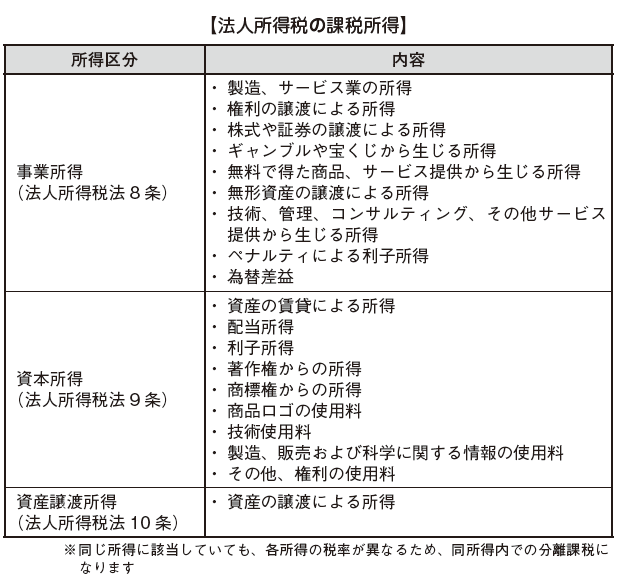

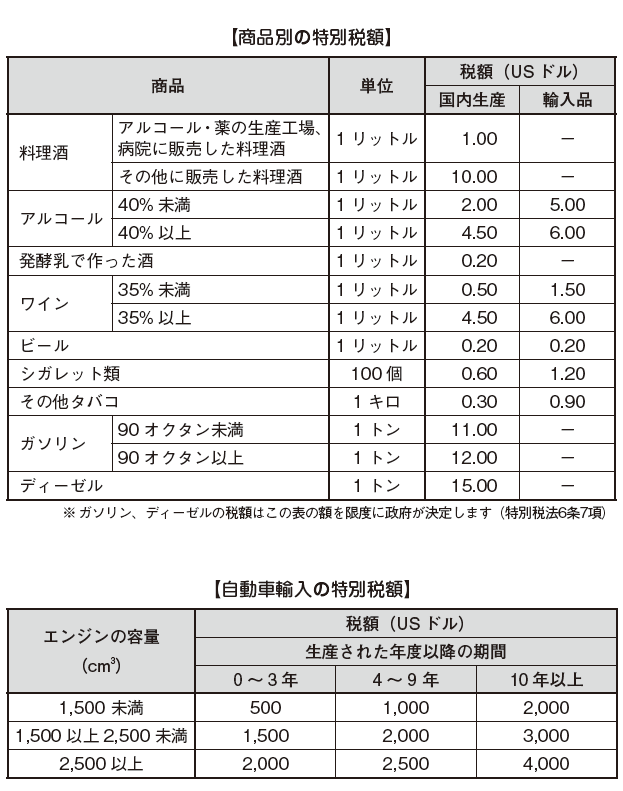

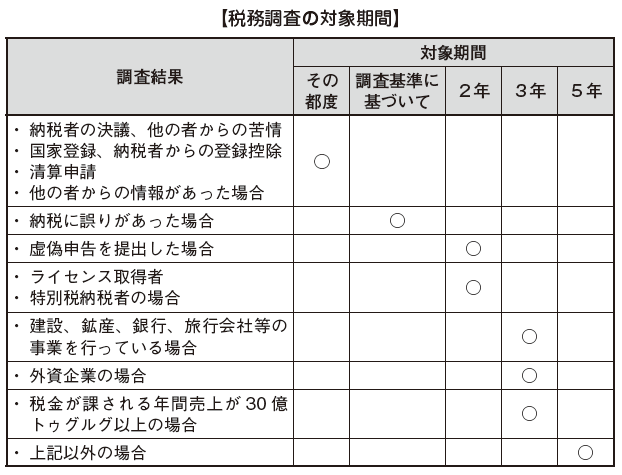

7 Chapter Tax

-

-

Tax treaty

A tax treaty is a process for avoiding double taxation and preventing tax evasion, etc.

It is an agreement (treaty) between countries, by the composition to be concluded between the houses. Since this treaty is an agreement between countries, the application will be applied in preference to the domestic law prescribed by each country. In other words, even if it is "taxed" under domestic law, it can be treated as "tax free" if it is said to be "tax free" in the tax treaty.

However, by applying the tax treaty, if it is become disadvantageous compared with the domestic law, it is possible to apply domestic law's priority, which is called "preservation closed".

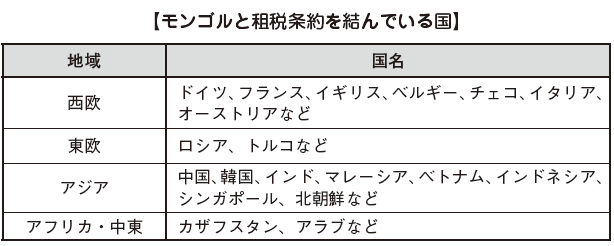

In Mongolia, we have concluded a tax treaty with about 30 countries, but we have not yet concluded a treaty with Japan.

-

Foreign tax credit

■ Avoid double taxation

Taxes are imposed on the movement or consumption of human resources, goods, money and management resources. Similarly for international transactions, if you move or consume management resources, taxation associated with it will result in a tax-related relationship between internationally.

The problem here is that the tax imposed on the transfer or consumption of management resources between the international countries is taxed based on each country's own idea (tax law). In other words, due to differences in laws, there is a possibility that two countries will be taxed at the same time in one transaction.

In order to eliminate such double taxation, the provision of "foreign tax credit" is stipulated in each country's tax law.

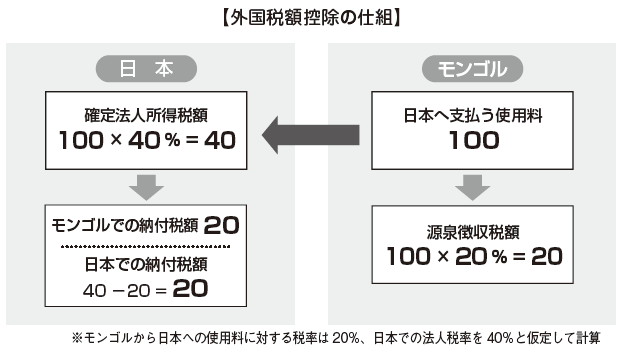

Foreign tax credit is a system established to prevent double taxation of international income by deducting taxes paid abroad to overseas income from the taxes of the country of residence. For example, this includes foreign income taxes paid by overseas branches, foreign source income tax withheld from payments such as royalties and interest received from overseas, dividends and so on. When such a tax amount occurs, double taxation occurs between the source country of income and the country of residence, so it can be adjusted according to the provision of foreign tax credit in the tax return of the country of residence.

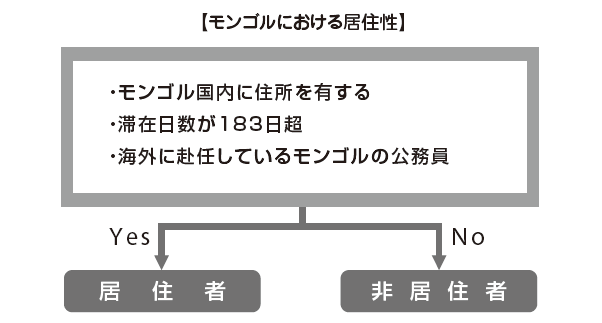

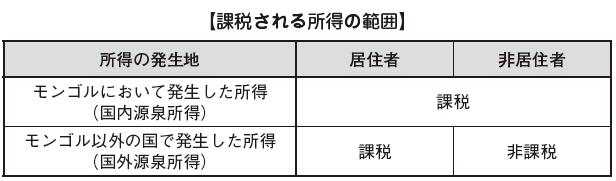

If double taxation occurs for residents of Mongolia, the overlapping tax amount will be deducted from the corporate income tax amount to be paid in Mongolia according to the provision of foreign tax credit (Article 19, 9 of the Income Tax Act).

-

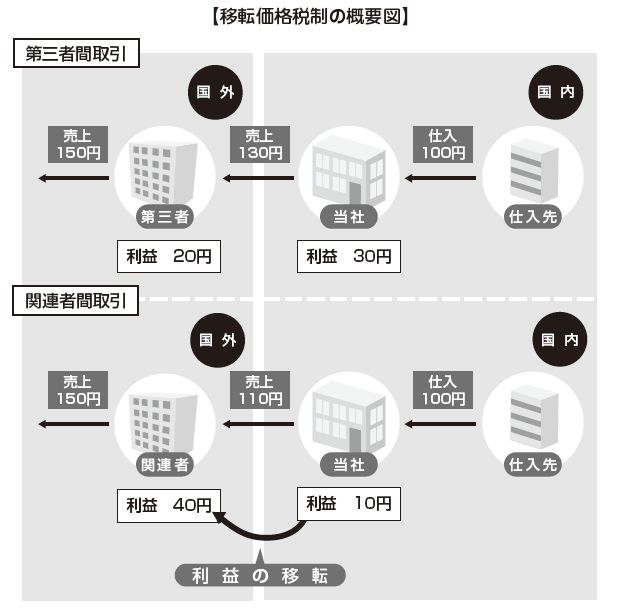

Transfer price taxation

Overview of transfer pricing taxation

With regards to the transactions among affiliates within the same company group, from the relevance, it is possible to freely decide the price pertaining to the transaction between companies. However, if you decide the transaction price freely for transactions with overseas affiliates, it is easy to transfer profits to other countries with a low tax rate. Then, each country will can’t keep its own taxation right, so we established a provision of transfer pricing taxation to prevent the transfer of profits to overseas (tax outflows abroad).

In other words, transfer pricing taxation is aimed at achieving appropriate international taxation by recalculating the transaction price among affiliates into the transaction price (interdependent enterprise price) between third parties.

In practice, taxpayers are not asked whether they intend to avoid taxes, so it is very important to prepare in advance for indications of transfer pricing and to consider risk prevention measures in advance.

■ Overview of Mongolia transfer pricing

In Mongolia, there is no tax law on transfer pricing taxation, so it is necessary to pay attention to transfer pricing taxation mainly in Japan side. However, as international investment in Mongolia will expand in the future, it is fully conceivable that transfer pricing taxation will be developed in Mongolia. -

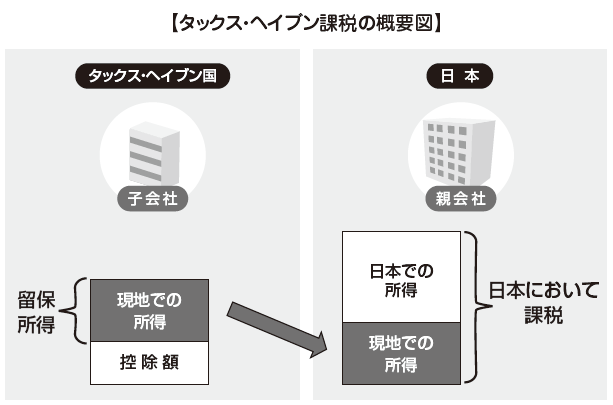

Transactions via tax · haven

The Cayman Islands, Bermuda Islands, Luxembourg, Cyprus, Singapore and Hong Kong, etc. are called Tax Haven (Tax Haven) and enjoy great benefits in terms of taxation by bringing profits to these countries It is possible to do.

In Mongolia investment, it is possible to think that it is not a direct investment from Japan, but a case where it is managed as a subsidiary company through regional headquarters (RHQ: Regional Headquarters) and managed. By establishing a central office in Tax · Haven, it is possible to retain the profits aggregated from each subsidiary by taking advantage of the maximum tax benefits.

However, if this RHQ is approved by the tax authorities as a "paper company without actual" at the Japanese side, the profits retained at the RHQ are added to the income of the Japanese side and the Japanese corporate tax will be imposed. We called this "tax and haven tax system".

■ Tax · Haven tax system

The tax · haven tax system (total subsidiary taxation system) stipulated in the Japanese Corporate Tax Law means that a domestic corporation has a specified foreign subsidiary company (a foreign affiliated company located in a light tax country), the specified foreign subsidiary Etc., the amount corresponding to the ownership ratio of the subsidiary shares owned by the domestic corporation is regarded as the profit of the domestic corporation, etc., and it is a system that intends to add tax together in Japan.

In other words, in Japan, tax is taxed in Japan regarding the profits retained abroad by recognizing "money" in taxation despite accounting "revenue" is not recognized.

Applicable to this taxation system is a foreign resident or domestic corporation that directly or indirectly holds more than 50% of its shares (together with a decision to exclude voting rights, shares without the right to distribute dividends) It is a company that is a subsidiary company and located in a country / region where tax exemption for corporate income or tax burden ratio is 20% or less.

Among them, if you are a resident or a domestic corporation holding directly or indirectly 10% or more of the shares of a specified foreign subsidiary, etc., the tax incentive will be applied to the amount of retained income of such foreign subsidiary.

In other words, a company that is located in Tax Haven, owns more than 10% of its shares in the same family, and more than 50% of its capital is Japanese equity.

However, all companies that meet the above requirement are not subject to taxation. It is not applied when falling under the following criteria because it is avoided that the enterprise's normal overseas investment business activities are obstructed by conducting the combined taxation.

· Business Criteria * 1 ... The contents of the business is not holding of shares or bonds, provision of rights such as know-how, other than lending business of aircraft etc.

· Entity standard ... have fixed facilities such as office, store, factory

· Control and control standards ... that they themselves are controlling and managing in the country of residence

· Unrelated party standard or country of origin standard

- Unrelated party criteria ... that the main business is being conducted with non-related persons (wholesale business, banking business etc. * 2)

- Country standard of country of residence ... what the main business is done in the country where the head office is located

(Manufacturing industry, retail industry etc.)

* 1 As a result of the 2010 tax reform, the controlling company holding a certain percentage of the shares etc. of the controlled company was excluded

* 2 As a result of the revision of the tax system in 2010, the managed company related to the controlling company whose main business is wholesale business and banking business was excluded

In certain cases where a specified foreign subsidiary company has an entity as an independent entity and it is deemed that there is sufficient economic rationality for conducting business activities in the country where it is located, tax avoidance is not a purpose, it is not covered by the same taxation system.

In other words, in order to avoid applying the same taxation system, it is necessary to prepare activity entities of specified foreign subsidiaries etc. before being pointed out by tax authorities.

■ Other international taxes

Overall, Mongolia has few provisions in the field of international taxation, so in the case of investment from Japan, we will mainly verify the tax provision on the Japanese side.

It is fully anticipated that international taxation in Mongolia will be strengthened as the investment from foreign countries in Mongolia will become popular in the future, so it is necessary to always keep up-to-date information on this point.

-