Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaMongolia

6 Chapter Accounting

-

-

Outline of Mongolian accounting system

In Mongolia, various laws have been enacted since the market economy in 1990, and from 1993 revisions have been made so that the accounting system approaches international standards. Also, in May 1997 we adopted the auditing law (Law of Mongolian Auditing) and in December 2001 the Law of Mongolian Accounting was adopted and it followed this law until 2016, but in June 2015, a new accounting law was enacted. In the year of 2016, we decided to abide by. Therefore, this Accounting Part contains the provisions of the Accounting Act of 2016.

According to Article 4.1 of the Accounting Act, the company must comply with the following accounting standards;

1. International Financial Reporting Standards (IFRS)

2. International Financial Reporting Standards for SMEs (IFRS for SMEs)

3. International Financial Reporting Standards for State Enterprises

Until 2016, all companies operating in Mongolia made financial reports in accordance with International Financial Reporting Standards (IFRS), but were divided into three according to the new accounting law. In addition, all companies record income and expense based on accrual basis (Accounting Act 6.1).

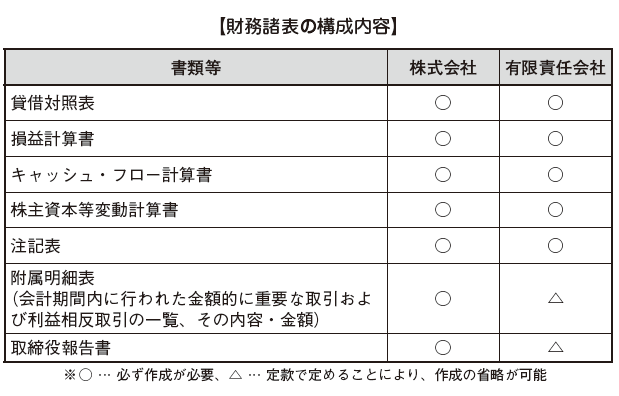

The company must prepare accounting books and financial statements in accordance with the Company Law and Accounting Law and disclose it to shareholders (Article 95, paragraph 1 of the Companies Act). In the case of a listed company, it is necessary to submit financial statements together with the financial regulation committee (Financial Regulatory Commission) and documents required by the stock exchanges and to publish them..png)

Post period

Under the accounting law of Mongolia, the accounting period of the company is from January 1st to December 31st (Article 10 paragraph 1 of the accounting law), it is not permitted to set the other period as the accounting period. Therefore, in order to prepare the consolidated financial statements by the parent company in the March financial year, it is necessary to deal with temporary closing of subsidiary of Mongolia at the end of March within the company.

■ obligation to keep account books

The company has an obligation to keep necessary documents such as accounting books (Article 97 paragraph 1 of the Companies Act). The accounting book must be kept for 10 years from the date of creation, and after 10 years has elapsed, it will be kept at the National Archives (General Archival Authority) (Article 11.1), which is the national and enterprise. It is a government agency that stores and manages documents created by the private sector. The necessary documents such as accounting books that need to be kept in the company and maintained so that they can be read by shareholders at any time.

The accounting book must be recorded in local currency Tugguru (Article 7). Or, if you obtain permission from related institution (Mongolian bank and financial regulation committee), it is possible to record with overseas exchange.

Accounting penalty

According to the accounting law, if a company fails to fulfill its obligation, it is subject to a penalty and classified as follows according to the content of the violation (Article 27 of the Accounting Act).

1. If you violate the following provisions, you will need to pay an amount equivalent to five times the minimum wage; (192,000 Tugulg / September 2013).

4.1 Accounting books comply with accounting standards

Article 7 Accounting books are created in Mongolian and recorded in Tuggle

Article 8.4. The executive officers and accountants sign the financial statements and press the seal

9.1. Report financial statements in electronic form to relevant organizations within the time limit of the law

Section 9.2. Obligations of Financial Management Organizations Reported in Electronic Form

9.5. In the case of electronic reporting, an executive officer or an accountant electronically signs it

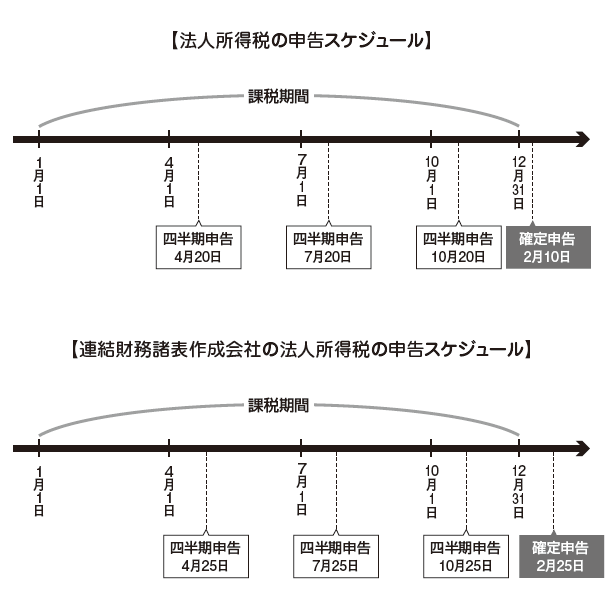

Article 10.3. Companies that comply with International Financial Reporting Standards report interim financial statements (January - June) by 20th July and electronic filing of tax returns to financial management organizations by February 10 next year

Article 10.4. Companies that prepare consolidated financial statements report the final declaration electronic form to the financial management institution attached to the parent company by March 1 of next year

10.5. Companies other than the above 2 will report the final return in electronic form by February 10 next year

10.6. Conditions financial institutions related to rural areas, the governor of the capital, shall submit a final return to the financial management organization by 20th March next year

11.1. The company keeps the financial statements for more than 10 years

14. Rules for accounting records, etc.

2. If you do not memorize accounting, if you are not preparing a financial report, give the employee a penalty of Togguru which is equivalent to 5 times the minimum wage and 5 to 10 times the low wage of the company to the company (27.1. 2 articles).

■ Mongolian accounting standards

Mongolia does not have its own accounting standards and adopts International Financial Reporting Standards (IFRS) as it is.

According to Article 4.1 of the Accounting Act, the company must comply with the following accounting standards;

1. International Financial Reporting Standards (IFRS)

2. International Financial Reporting Standards for SMEs (IFRS forSMEs)

3. International Financial Reporting Standards for State Enterprises

In recent years, the number of companies investing in Mongolia from abroad has increased, and the transparency of accounting standards is also required. Especially the qualitative improvement of accounting report is also strongly requested for comparing accounts with other countries. It is expected that it will be possible to attract investment from overseas markets by improving the transparency of these accounting standards and the qualitative improvement of the report contents.

-