Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaIndia

9 Chapter Transfer Pricing Taxation

-

-

Globalization and Transfer Pricing

1.1. Introduction of History of Transfer Pricing TaxationTransfer Pricing taxation is the system that in case "Corporation" trades with particular group companies ("foreign related person") such as sales of assets, purchase of assets, provision of services, other transactions ( following is "Foreign-related transactions"). And in case a certain price that the amount of the consideration paid from foreign related person is considered to be appropriate, namely the case of less than Arm's Length Price or the case of more than Arm's Length Price (ALP), the foreign-related transactions has been considered trading by ALP on the calculation of corporate tax.

Transfer Pricing Tax system existed since 1920 as provisions on income distribution between each state in the United States.

In the sixties, the production subsidiary company of an American enterprise considered the tax system favorable. The overseas manufacturing subsidiary company of an American enterprise made efforts to create profits and lower the tax burden. As a result, in 1968 in USA, internal revenue code regulations regarding Transfer Pricing were enacted.

Since the 1970s expansion of international transactions particularly for intangible assets trading in existing trading provisions between the nations was enacted in 1968.

Transfer pricing is adopted all over the world, and has been established in the Special Taxation Measures Law in 1986 in Japan as a special case of “Taxation on Transactions with Foreign Affiliated Persons”.

1.2. Internationalization and Transfer Pricing

In recent years, progress in multinational companies is no longer a border of people, goods, money in globalization. For huge global companies, a same product utilizing the brand, it becomes possible to provide services and also make foreign transactions. It has been followed that the risk involved in the Transfer Pricing problem has also been rapidly expanding.

Advances in recent years in multinational corporations, globalization in people, goods and borders are dissolving. A steady increase has been marked in overseas transactions through capitalizing brand power by increase in products and services of huge global corporations. Also the risks associated with Transfer Pricing have been growing rapidly.

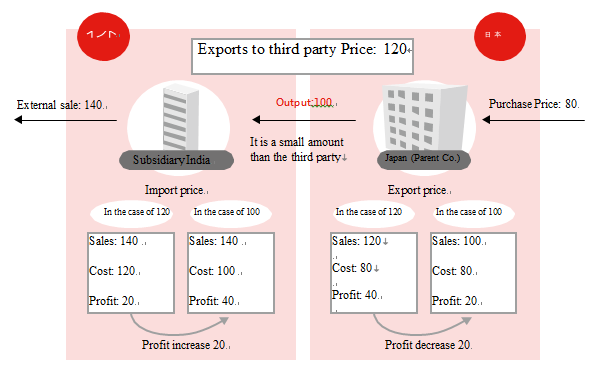

Profit transfer between Japan and India

In this way, simply changing the trading price of between affiliated companies (transfer pricing), income to be generated in the country is reduced. This eventually reduces tax in the country.

In the Transfer Pricing tax system, when more than a predetermined price adjustment has been made through international transactions, possible tax collected in their own country is not unduly transferred to other countries. It is intended to add a limit on the price adjustment based on the tax laws of each country to prevent the reduction of unfair taxable income. It can be said that these provisions are order to ensure the country's taxation rights.

On Transfer Pricing issues, basically there are two types of cash transfer goods and services. In these rather than just goods, products and raw materials; intermediate goods also include royalty and management fee or loan interest.

Transfer Pricing strategy of international companies in particular plays a major role to overcome the promotion and barriers for entry of capital accumulation group of companies.

On the other hand, it cannot be denied that negative acts with respect to transfer pricing strategy forms capital and tax revenues in the invested country. Transfer pricing strategy has been criticized as "abuse of dominant market" and "tax avoidance".

Tax authorities of countries do not overlook the outflow of profit from the country due to Transfer Pricing. The authorities determine the correction of transaction price in order to ensure the tax revenue to be obtained originally.

Transfer Pricing problem is a set of transaction price between corporate groups which requires pricing considering the aspects of financial strategy. For international transactions the divergence in the transaction price between group of companies and third party occurs which requires modification.

In addition, assuming that transaction price was set to third party, the profit is not generated on overseas side. The problem of saving’s location occurs if profit is generated on the Japanese side.

This way, Transfer Pricing problems is not just of tax. In addition, management and statistics is entwined in a complicated way and hence the proof of validity of the transaction price requires extensive knowledge.

-

Transfer Pricing in India

2.1. Introduction Background of Transfer Pricing in India

Due to the close relationship between the Indian resident and non resident who is a related party, resident’s income becomes nil and the authorities adjusts their income.

Since there are no guidelines for execution, it was insufficient for tax authorities to deal with Transfer Pricing issues. The numbers of foreign companies expanding in India are increasing with a remarkable development and foreign direct investment in the economic environment. In view of such factors, Transfer Pricing taxation was introduced in April 1, 2001.

Transfer Pricing taxation of India, has been defined in the Income Tax Act. Calculations of arm’s length price (ALP) in India are generally compliant with the OECD guidelines.

OECD Guidelines for Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations. OECD tax commission related to Transfer Pricing, relates to multinational companies for the above problem. It shows the measures of resolution for tax authorities and multinational companies in both countries.

The OECD guidelines do not constitute to a legal bind but it has been compiled on the consensus of OECD member countries and functions as international consensus.

As per OCED guidelines, 1979 are created for a purpose of fair application of prevention and Transfer Pricing of double taxation corresponds to rapid changes in the international economy through advances such as globalization and technology. Set guidelines are published since 1993.

2.2 Features of Indian Transfer Pricing

Transfer Pricing taxation rights are country specific. The differences vary by country. However for the OCED member countries, the taxation rights are compliant to OECD guidelines.

As a feature of Transfer Pricing in India, it includes the following points.

2.2.1 Verification method of Arm's Length Price (ALP)

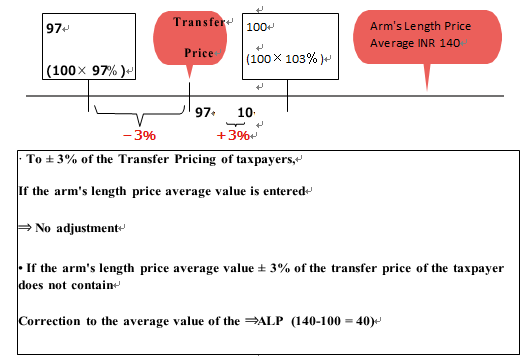

Usually while calculation of inter-company price, average of more than one calculated value is treated as Arm's Length Price. However in India, there is a set Arm's Length Price range. Whether Transfer Pricing is within range or not, Transfer Price will be judged.

As a concrete standard before and after the taxpayer's Transfer Pricing if price was calculated at 3% in * the average value in the taxpayer's Transfer Pricing is reasonable. Outside income is adjusted to the average value of the price.

Since April 1, 2012 5% was changed to 3%

Conceptual Diagram of Arm's Length Price

Between 3% before and after the Transfer Pricing (100) (97-103), the average value of Arm's Length Price is considered reasonable. However in the example of figure, it is 140 which are above the range mentioned. Hence, it shall be subject to income correction by tax authorities.

In this case the amount applied will be 40, difference between the actual Transfer Pricing (100) between independent companies with an average price value (140). It has been notified that the wholesale range defined as 1% is now 3%. It does not show clearly about what specifically how taxpayer corresponds to wholesale trade. From now on, this is where clarification of wholesale definition is awaited.

Location Saving

The savings in costs realized by a multinational company when it relocates facilities from a high-cost jurisdiction to a low-cost jurisdiction. The savings are typically derived from lower labor, rent, material and property tax costs. However, India tax authorities, certain portion of the profits generated by the difference of location to be recognized in India, the benefit amount is to be determined by the contribution degree of Indian domestic services.

It is thought that the calculation of location saving correct, practically is difficult. In fact there are variables such as both price levels in the overseas allied business or the competitive power with the competing company. Therefore, many cases actually calculate a price between independent companies in a standard at a profit rate for the total cost that they took.

In addition, it is extremely delicate and demands a change in calculation method. Also there is a case of royalty for the parent company being denied because there was no index that clarified about distribution of the location saving.

When viewed from the perspective of companies operating in relation to these matters, location saving improves economic efficiency leading to cost reduction. Independent domestic companies operating in the same environment also enjoy benefits of inexpensive management cost. Income transfer generated by the associated inter-company transactions is not directly related.

Cherry Picking

In Transfer Pricing study, the change of arbitrary comparable companies carried out by investigators has been referred to as "Cherry Picking".

It is not specific to a realistic and comprehensive market only. It analyzes the company’s business environment based on assumptions; hypothesis relative object enterprise is modified by the highly profitable enterprise whose Transfer Price authorities are convenient. In case low profit enterprise, deficit of an enterprise is dismissed.

The purpose of Transfer Pricing study is not to reveal whether there is intention of income transfer, but is to calculate the income transfer amount using objective methods and possibly disconnect the status of companies. In depth discussions have been done in case of individual transactions, which result in exercise of appropriate non-income countries. Recent national tax on litigation court (ITAT) in Adjudication obviously Transfer Pricing officer was recognized as "Cherry Picking". (TPO: Transfer Price Officer) correction request was rejected. Detailed and comprehensive analysis and documentation is essential.

Safe Harbors

The safe harbor is as a defending benchmark to corporate side of the profit level indicated by the tax authorities in each industry. The system makes it possible to avoid correction due to tax authorities.

In India, on 18th September, 2013 direct and safe harbor was published from Tax Central Committee (CBDT). It has been expected that the litigation related to Transfer Pricing taxation is reduced. However, in case safe harbor is to be applied, a mutual consultation of 3% of the allowable range for MAP: Mutual Agreement Procedure.

Provisions for Strict Documents Maintenance

In India’s Transfer Pricing system, provisions relating to documents maintenance are stricter than Japan. Documentation relating to Transfer Pricing has clearly been defined by law. It requires one to be careful because if not adhered to guidelines, penalty shall be imposed. (It will be described in detail later)

Target Trading Range of Transfer Pricing

The subject transaction of Transfer Pricing is usually transferred assets to pay off loans. It includes all transactions such as services provided.

In India, advances of expenses between affiliated companies and other capital transactions (investments and capital increase, etc) are also included in the target transaction.

2.3 Individual Provisions Related to Transfer Pricing

2.3.1 Range of Subjects (Subject Corporation)

As per Income Tax Act, Article 92, the business between international transactions that occurred between an overseas associated enterprise (AE: Associated Enterprise) is established with Arm’s Length Price (ALP).

Real Standard and Format Standard are the two Transfer Pricing standards applicable for foreign related persons.

Format Standard: Such as the number of shares held is a majority, the decision whether to apply to foreign related parties by specific numerical

Real Standard: Even if there is no direct dominance relationship between human resources and trading

Even if there is no direct dominance relationship, human resources and trading, and judged by whether is found to be in the Control and the dominance of the relationship as an entity such as through financial

Even if there is no direct dominance relationship,

Human Resources and trading,

The dominance as an entity such as through financial and

The determined by whether recognized and the relationship of the controlled

In Section 92 of the Income Tax Act, if any entity controls the other enter price either directly or indirectly or through equity participation alone or through several intermediaries then the provisions of the transfer pricing will apply subject to certain condition.

26% if more than holding relationship

One of the entities to provide direct or indirect services, and vice versa in case of affected entities.

90% or more for procurement of raw materials and other provisions have been met as per company’s requirements

If one entity is located in a specific defined location

If more than 51% of the book value of total assets of one of the companies, there are loans or debt guarantees from other companies

Officer with a representative authority of one of the company if, or a majority of the directors of the company, and is an officer of other companies

If the business of one company relies on intellectual property of the other companies

Certain other requirements

Transfer pricing in Japan was introduced in tax reform in 1986. Transfer Pricing is applied on transactions like sale of assets that corporations do with a foreign related party or purchase of assets. As per Special Taxation Measures Law Article 66, the principle states that one is limited to transactions with foreign related parties.

Following is the relationship between a corporation and foreign related party transactions. (Special Relationship)

- One of the companies, the relationship that holds the number or investment amount of more than 50% of the shares of other companies directly or indirectly

- Both companies, each company holds more than 50% of the number of shares or investment amount directly or indirectly by the relationship of such outstanding shares by a person

- Officer or director, trade dependent, funded by borrowing, substantially determined can do relationship is one of the corporation per all or part of the other corporation of business policies.

There are differences in recognition of its range. It must be noted that in Japan and India "foreign related persons ' would be subject to transfer pricing.

For applying transfer pricing for transactions among related companies on the Japan side, and about trading with overseas branches not eligible for transfer pricing, India is subject to transfer pricing for transactions with overseas branches.

The application of Transfer Pricing in India is a permanent establishment criterion. In other words, it is because they are made to entities that are functionally separate rather than corporate status unit. Branches of overseas subsidiaries are also the scope of application of transfer pricing. Attention is necessary because it is being considered that amendments to tax treaty between the U.S. and Europe will be stricter.

In the 2012 fiscal budget proposal, specific domestic transactions provided from April 1, 2012, also for transactions that fall under this category, it becomes the subject transaction of transfer pricing.

The specific domestic transactions, more than 20% of capital is related to Indian Law as human transactions (parent-child transactions).In addition to international transactions with foreign officials, the transaction is more than INR 50 million annually. Appropriate certificates and documents of India Chartered Accountants are required.

To perform any of the transaction, which is defined to transfer pricing, and if the transaction amount is equal to or greater than the annual INR 10 million, creating and saving the document (English) (minimum of eight years) is required. Furthermore in order to prevent the income transfer using the tax rate differences between domestic companies, Transfer pricing has been applied for the "deemed international trade" that is Specified Domestic Transactions ("SDT"). Similar obligation occurs when there is a year INR 50 million or more of trading for SDT.

In addition, in the audit certificate, statutory declaration states that November 30 is the deadline to sign the Form3CEB. One needs to certify that the documentation has been properly carried out.

It is to be noted that in some of the relevant trading companies, response for similar transfer pricing is required.

2.3.2 Subject Transaction of Transfer Pricing

All transactions are subject to Transfer Pricing considering loan sale inventories, intangible asset sales, services provided, funds etc. In addition, burden contract and allocation of costs and expenses between several companies within the group of companies is also included.

It must be noted that that considering certain transactions, regardless of money transfer even if services provided are temporary, there is a provision of mo service charge. If those transactions are traded, it would be subject to Transfer Pricing.

2.3.3 Calculation Method of Arm's Length Price (ALP)

Transaction price between underlying international incomes calculated in terms of Transfer Pricing is applied established by Arm's Length Price. Calculation of Arm's Length Price is defined in a number of ways and is considered appropriate as per the form and content of transaction.

For Transfer Pricing in India, it must be compliant with the OECD guidelines. Generally the following method is used for calculation.

Independent Price Ratio Quasi-Law

Independent Price Ratio Quasi Law (CPU Method: Comparable Uncontrolled Price Method) - Under almost similar conditions as those of foreign related transactions, the amount of consideration of which was held between third party transactions is a way of Arm's Length Price of foreign-related transactions.

If the transaction of such an article is to be compared, for change in trading conditions due to business strategies and market conditions, it may get difficult to ensure comparability. In addition, if compared to calculation method of Arm's Length Price, higher identity is required. Therefore this method is widely used in commodity trading during fluctuations in trading conditions of low interest rates. It is not adopted for normal trading of goods.

Resale Price Standards Act

A resale price standard method (RP method: Resale Price Method) is a method to assume an amount of money subtracted from amount of profit, that is obtained from a price between independent foreign related transactions and from the resale price to the third person.

This method has been used especially in case of import transactions as in many cases; comparison data is obtained from public data. Also the similarity of about independent price ratio (Quasi Law) is not required.

Cost Plus Method

CP Method: Cost Plus Method is the amount of acquisition costs incurred by foreign related transactions of interest. The amount of the other corporation is calculated by adding the amount of profit that would normally be obtained from the transaction to Arm’s Length Price of foreign-related transactions.

Cost Standards Act

Amount of Forehead + Normal Profit of Acquisition Cost = Arm’s Length Price

Contribution Profit Split Method

Arm’s Length Price is calculated based on the proportion of function and risk for each relevant person by distributing the profit among the related parties.

Compare Profit Split Method

Arm’s Length Price is calculated on the basis of the profit split ratio in non-related party transactions that have been made in the context of similar foreign-related transactions by allocation of combined profit among related parties.

Residual Profit Split Method

Each party has significant amount of intangible assets. The amount equivalent to the benefits is obtained usually in transactions where it is not taken into account. The important intangible assets of the combined profit are allocated to the rest of the amount. Arm’s Length Price is calculated by allocating combined profit depending on the value of important intangible assets.

Business Unit Operating Income Law

TNMM: Transaction Net Margin Method - Arm's Length Price is calculated by computing the Net Margin realized by the enterprise from an international transaction entered into with an associated enterprise. The net profit margin established is thus taken into account.

Other Methods

In case of sales of inventory assets (goods, etc.)

Other methods equivalent to Independent Price Ratio Quasi method or Cost Basis method as per resale price Standards Act shall be used. When applying these methods and selecting a deal with reference to the type of inventory, trading volume and trading time; other conditions must be considered.

In the case of Money Loan

Independent Price Ratio Quasi-Law, cost basis method and other equivalent methods are mainly used. In this case selection of transactions is to be compared and the currency of the transaction is the same. Loan period of money, setting the interest rate, payment method and pricing is considered as the factors affecting the creditworthiness.

In the case of providing trading services

As in the case of the loan of money, independent Price Ratio Quasi-method and the cost basis method and other equivalent methods are mainly used. Upon selection of the comparison target transactions, the terms and conditions of the service period and services provided must be the same.

It must be noted that if such service provision transactions are done in conjunction with use of transfer assets, it must be calculated properly considering the required services being provided.

Use or Transfer of Intangible Assets (such as royalty deal)

The intangible assets and other legal rights such as patents and trademarks refer to such trade secrets and other know-how. There are some differences in the range from country to country.

The intangible assets in India like patent, design, trademark, copyright, know-how, licensing rights refers to such franchise or other similar nature of business on the basis of commercial rights. Independent price Standards Law in calculation method, Cost basis method and other equivalent method is used to evaluate these when selecting the comparison target. For assets related to compare transaction timing, duration of use or transfer or other similar terms and conditions will be asked.

It is difficult to understand worth for anything other than legal rights of intangible assets. For further pricing, it becomes difficult for use or transfer due to presence of many cases that which have been corrected by tax authorities. It is necessary to show clear pricing grounds when such existence affects business.

In the case of using any calculation methods, selection of transactions that are compared becomes important as the method of selection. There are two ways of the method to be based on transaction price and a profit rate from transaction carried out between corporation and non related parties.

If present transactions, it is common to refer those targeted in internal trade. There are many cases where there is no transaction and it would be referred to external transactions between non related parties.

2.3.5 Transfer Pricing and Custom

[Differences and similarities of the tariff]

Transfer Pricing tax system may be prescribed by Income Tax Law as rules to determine the Arm’s Length Price (ALP) in foreign related transactions. Both tariff applied to the time of import will be closely related.

Similarities with tariff

In the relevant inter-company transactions commodity price evaluation on the tariff is done as a reference as to whether or not it corresponds to any of the three price below.

• Transaction Value

• Deductive Value

• Computed Value

"Transaction price to third parties" is in the arm's length pricing method in transfer pricing and is similar to independent price ratio quasi method (CUP method). "Estimated price at the time of re-sale" is in the arm's length pricing method in transfer pricing, which is similar to the resale price Standards Act (RP method). In addition calculation price, which is determined by the cost, is similar to the cost basis method.

For Transfer Pricing, the purpose of understanding the price of fair reasonable goods to customs both are the same, there is no significant difference with respect to reference of the evaluation.

Tariff Price Evaluation Criteria and Similar Arm's-Length Pricing Method

Tariff price evaluation criteria

Pricing Between Independent Firms

The transaction price to third parties

Transaction Value

Comparable Uncontrolled Price Method

The estimated price at the time of resale

Deductive Value

Resale Price Method Standards

Resale Price Method

Calculation price determined by the cost

Computed Value

Cost Basis Method

Cost Plus Method

Differences in Valuation of Goods

If you look at the transfer pricing taxation from the point of view of tax authorities, the import prices in the overseas allied business reduces the cost of importer. In order to get more profit, there won't be a problem in taxation business.

On the other hand, if looked at from tax authorities’ point of view, tariff amount is calculated based on the price of imported goods. Price of commodity being higher is not a problem.

In addition, transfer pricing rules evaluate reasonable prices all year round whereas tariff of certain imported goods are focused at the time of import. There is a large difference between Transfer Pricing Profit Split method that has been observed in the tax system (PS) method and trading unit operating income method (TNMM).

In this way, calculation method of fair price in foreign-related transactions would be similar. The purpose of price adjustment is very different.

Transfer Pricing Taxation

Tariff

Price between independent companies (Above grid)

×

○

Price between independent companies (In the grid)

○

○

Price between independent companies (Below grid)

○

×

Problems and Counter Measures

As mentioned above, between transfer pricing and customs, there are differences and similarities in the calculation of Arm's Length Price. In case the price observed on the Transfer Pricing tax system and cause problems for customs and tax authorities in different cases, it was not available during customs duties.

To avoid such problems, some companies separately select transfer pricing taxation measures. There is also information that corporation tax authorities and customs submit documents to each other. Risk is involved in this case.

For the calculation of the arm's length price, World Customs Organization (WCO: World Customs Organization) and the Organization for Economic Cooperation and Development (OECD) perform a consultation. At the same time for solving issues, it is discussed at the top level. Against countries, a system strengthening of tax authorities and customs exists.

2.3.6 Mutual Agreement

If the income correction has been performed by the transfer pricing taxation, in order for the income of modified parts that are taxable in each of the parties, it becomes that international double taxation for increased income amount.

In order to eliminate such double taxation, in accordance with mutual consultation matters that are stipulated in tax treaty, competent authority makes amendments between each country concerned (country tax treaty has been signed) and the government of Transfer Pricing is called a "mutual agreement".

On the other hand, in trading between countries where tax treaty has not been concluded, the resolution can be achieved only within the scope of the provisions of national tax law (such as appeals and tax litigation).

For a reconciliation of double taxation, it is basically done by methods defined in treaty. It is because there is a possibility that it is difficult to adjust due to difference of opinion between the two countries of the Convention. As rescue treatment of such cases, mutual consultation has been positioned.

As per India Japan tax treaty, Article 25 of the convention, the transfer pricing has been applied for the foreign related party transaction between Japan and India. The allegations for mutual consultation are made against authorities of each country of residence.

Mutual consultation is performed after complaint from the party if all the allegations of mutual consultation were not made from any of the parties in Japan and India. If mutual consultation does not take place, a three year deadline has been defined by Japan - India tax treaty.

APA

As per Fiscal Budget 2012 in India which was introduced in July 2012, the APA system gets check in advance from tax authorities on the calculation method of the transaction price of the foreign related person.

This is a system to receive confirmation about a price between the independent companies which the company side calculated on the occasion of setting the price of business to become the object of the Transfer Price and the validity of the calculation method beforehand from the tax authority. Two points below are raised:

- Unlike price verification of authorities led by prior confirmation, examination for transparency at price verification is performed

- By performing the pre check, the risk of future tax reorganization by transfer pricing study is eliminated. It is possible to prevent the taxes in advance.

In addition, due to certain conditions Rollback (retroactive application of the past four years) was newly provided. Such provision will be applied from October 1, 2014. The APA benefits have been expanded.

In addition, in determining the arm's length price, if you want to compare with other companies in the same industry of transaction information, the comparative period has been one year. Comparative period over multiple fiscal such as a three-year average value is also acceptable. Reforms of the system have been proposed.

On the other hand the disadvantage to pre-confirmation is that the procedure is expensive. Since the period of determination is relatively long, while performing the notification it is necessary to take decisions carefully.

In addition if you take a check through agreement of mutual consultation, it does not have to undergo Transfer Price taxation from partner countries.

In recent years, the increase in international trade and with the increase in number and offer to reflect the complex, prior confirmation number can be found.

Chromatography (about $ 20 million) following transactions is one million INR (about $ 20,000), 1 billion INR (about $ 20 million) Ultra 2 billion INR (about $ 40 million) following transactions 1.5 million INR (about $ 30,000), Trading for an amount to be more than it is 2 million INR (about $ 40,000).

Trading Scale

Application Fee

1 billion INR (about $ 20 million) or less

One million INR (about $ 20,000)

1 billion INR (about $ 20 million),

2 billion INR (about $ 40 million) or less1.5 million INR (about $ 30,000)

2 billion INR (about $ 40 million)

2 million INR (about $ 40,000)

Taxpayer can withdraw pre-confirmation application at any time before the terms and conditions of the prior confirmation reach the agreement. However, application fee will not be refunded. In addition, if there are deficiencies in the application, notice in writing to that effect within one month from the application will be made. Tax payers need to fix deficiencies within 15 days after receiving the notice. If you do not fix it within 15 days (extendable up to 30 days), application is rejected and application fee will be refunded to the taxpayer.

There are questions and answers from the advance personnel after the application is approved, advance teams and create draft report will be submitted in case the DGIT or permission of competent authorities (in charge of mutual consultation). And this based on agreed draft DGIT or authorized officials (in charge of mutual consultation), with approval of the Central Government, will be agreed upon between the applicant and the Central Committee of the direct taxes (CBDT).

The tax payer must submit an annual report (Annual Compliance Report (ACR)) to DGIT from less than 30 days or an application of the prior confirmation after the presentation of the income tax return within 90 days. After the application has been accepted, prior confirmation team creates a draft report, which is submitted to the DGIT or authority of certain authorities (mutual consultation in charge). DGIT or authority of certain authorities (mutual consultation in charge) creates a draft agreement on the basis of this with the approval of the central government.

2.4 Moved in India Price Investigation

2.4.1 Overview of Transfer Pricing Study

Transfer Pricing tax system was introduced in 2001 in India and about 15 years have passed since then. Tax audit number in India, has been increasing year by year, rehabilitation income amount there are also on the rise. In particular, when the light of the India foray is actively present situation of foreign, it is assumed to continue to increase in both the number-correction income in the future.

2.4.2 Overview of Indian Transfer Pricing Study

Transfer Pricing study in India has the following features.

Transfer Pricing Expert Organization

In India, Transfer Pricing Expert organization has been established for investigation, investigators and evidence disclosure. Account Books and other related documents will not have access to information submitted in compulsion.

For standard amount of tax investigation selection, has been carried out reviewed every year. For 2014 - 2015 to force the target companies of tax audit selection to be carried out, the criterion of income increase rehabilitation was defined as INR 100 million. It has been changed significantly from the guidelines that had been the subject of transfer pricing investigation in the case of more than INR 150 million so far. In other words, if the transaction value of the year with foreign related parties exceeds INR 100 million, the direct tax personnel of normal tax authorities: from (AO Assessing Officer), information is delivered to the transfer pricing officer, and on its transfer pricing officer will conduct an investigation of the company. Transfer pricing officer provides companies, disclosure of evidence and related documents, has the authority of such interrogation. Also, if one is subject to forced tax investigation by the transfer pricing transactions criteria, one need to be careful because it means that research is also carried out for the corporate tax.

Penalties (Penalty)

The provisions pertaining to fines (penalties), are enacted strictly in Transfer Price.

- Document storage breach of duty ⇒ 2% of the transaction price

- 2% of the information provided breach of duty ⇒ transaction price to the tax authorities

- Undeveloped ⇒ INR10 million of 3CEB

- 100% of the tax relating to ⇒ correction if there is income rehabilitation% to 300%

- If there was a false statement to Transfer Pricing documentation ⇒ 2% of the transaction price

In most cases, penalty in accordance with the tax laws, the form of what percent has been taken against the tax is in question. In document storage, 2% of the transaction price is imposed as penalty if there is a false description of contents. Such document will be required in trading with large-scale company.

2.4.3 Tax Litigation related to Transfer Pricing

If Transfer Pricing amended and corrective measures imposed from the tax authorities do appeal court on the tax payer’s side.

There is the severity of cherry picking and penalty in India. Many cases develop into lawsuits.

-

Transfer Pricing and Documentation

3.1 Provision System involved in the documentIn Transfer Pricing of India, transactions with a foreign-related person, information and documents must be directly stored as provided for Tax Central Committee (CBDT).

However, until you are asked by the tax inspector, there is no submission obligation. Storage obligation period will be eight years.

Information should be kept and documented. Validation data of the overview of the related party group, transaction details, transfer price calculation, and other auxiliary materials, are included while calculating the transfer price.

If the annual amount of transactions between related parties is more than INR 10 million. In addition we are obliged to create a document related to Transfer Pricing.

On the other hand, if annual transaction value is less than INR 10 million, the creation of document is not required. However, if the price is asked for proof which is appropriate due to the tax investigation, it is necessary to prove that transactions between related parties have been made in arm's length price (ALP). Also, if annual transaction amount is not more than INR 10 million or less; documents of related transaction must be established.

Companies that are subject to Transfer Pricing and get India Institute of Chartered Accountants issued Transfer Pricing Certificate (trade with a 3ECB/ALP certificate) must attach and submit it to the tax returns for income tax.

India tax authorities require documents for the company within 30 days from issuing a notice of tax audit because it has the authority to request submission of information. If there is a transaction with a foreign related person, one needs to keep the required materials.

Even trading price of taxpayer was an independent business-to-business price.

It is not possible to escape penalty by breach of storage and submission of written materials or 'Transfer Pricing certificate (3CEB)'.

However taxpayers put in a considerable effort. And if it is proved considerable attention was paid to determine purchase price, penalty associated with the correction is not imposed.

Similarly, also for other penalty in the table above, if the taxpayer has demonstrated that there was good reason according to the breach, penalty is not imposed.

It has been suggested that, in various debates of the India Government, take the documentation requirements for trading the same two penalties does not apply at the same time.

However after such a comment being made, it is also true there is no legal binding for the tax authorities, which has the authority to impose a penalty.

3.2 Transfer Pricing Audit

3.2.1 Summary

When income tax return law Transfer Pricing documentation provisions for the transaction in case of transactions with foreign related parties has occurred, certain law provisions are enacted. Specifically in each taxable year when performing a transaction with foreign-related person, it is transferred to create proof of price (Form 3CEB) by India Institute of Chartered Accountants. Also it must be submitted with the tax return.

If you did not submit a Form3CEB, INR 100 000 as a penalty is imposed.

3.2.2 3 Example of 3CEB

Form 3CEB is divided into two parts, Part A and Part B. Each of it is described as follows.

1) Part A

The Part A, Company name and location will describe such basic information of other companies. In addition, Chartered Accountants of signing are listed in this.

2) Part B

In Part B, the transactions performed between related parties outside the question format; the description shall be continued in the form of a Yes or No. Specifically, the presence or absence of trading in each of the following categories requires company name, street address and transaction amount to describe the calculation method of ALP.

Usually increase in content is often described. For more information about each transaction creating a separate sheet (Annexure) as supplementary material shall describe the forms in detail.

Q. In Japan, a small parent company and India subsidiary are traded, what would be required corresponding to the Transfer Pricing taxation?

A. Accountant's certificate (3CEB) will be required between affiliated trading companies.

In addition, the corporation is doing international transactions between INR 10 million or more. Every year one is obliged to store the documents related to the transaction. It must be submitted together with the tax return Transfer Pricing Certificate (3CEB) in order to prove that the transaction is valid.

FORM NO. 3CEB

[See rule 10E]

Report from an accountant to be furnished under section 92E relating to international transaction(s)

1. *I/We have examined the accounts and records of (name

and address of the assessee with PAN) relating to the international transactions entered into by the assessee during the

previous year ending on 31st March,

2. In *my/our opinion proper information and documents as are prescribed have been kept by the assessee in respect of the international transaction(s) entered into so far as appears from *my/our examination of the records of the assessee.

3. The particulars required to be furnished under section 92E are given in the Annexure to this Form. In *my/our opinion and to the best of my/our information and according to the explanations given to *me/us, the particulars given in the Annexure are true and correct.

**Signed

Name:

Address:

Membership No.:

Place:

Date:

Notes:

1. *Delete whichever is not applicable.

2. **This report has to be signed by —

(i) a chartered accountant within the meaning of the Chartered Accountants Act, 1949 (38 of 1949); or

(ii) any person who, in relation to any State, is, by virtue of the provisions in sub-section (2) of section 226 of the Companies Act, 1956 (1 of 1956), entitled to be appointed to act as an auditor of companies registered in that State.

ANNEXURE TO FORM NO. 3CEB

Particulars relating to international transactions required to be furnished under section 92E of the Income-tax Act, 1961

PART A

1. Name of the assessee

2. Address

3. Permanent account number

4. Status

5. Previous year ended

6. Assessment year

PART B

7. List of associated enterprises with whom the assessee has entered into international transactions, with the following details:

(a) Name of the associated enterprise.

(b) Nature of the relationship with the associated enterprise as referred to in section 92A(2).

FORM NO. 3CEB

[See rule 10E]

Report from an accountant to be furnished under section 92E relating to international transaction(s)

1.

*I/We have examined the accounts and records of (name and address of the assessee with PAN) relating to the international transactions entered into by the assessee during the previous year ending on 31st March,

2. In*my/ouropinionproperinformationanddocumentsasareprescribedhavebeenkeptbytheassesseeinrespectof the international transaction(s) entered into so far as appears from *my/our examination of the records of the assessee.

3. Theparticularsrequiredtobefurnishedundersection92EaregivenintheAnnexuretothisForm.In*my/ouropinion and to the best of my/our information and according to the explanations given to *me/us, the particulars given in the Annexure are true and correct.

**Signed

Name:

Address:

Membership No.:

Place:

Date:

Notes:

1. *Delete whichever is not applicable.

2. **This report has to be signed by—

(i) a chartered accountant within the meaning of the Chartered Accountants Act, 1949 (38 of 1949); or

(ii) any person who, in relation to any State, is, by virtue of the provisions in sub-section (2) of section 226 of the Companies Act, 1956 (1 of 1956), entitled to be appointed to act as an auditor of companies registered in that State.

ANNEXURE TO FORM NO.3 CEB

Particulars relating to international transactions required to be furnished under section 92E of the Income-tax Act, 1961

PART A

1. Name of the assessee

2. Address

3. Permanent account number

4. Status

5. Previous year ended

6. Assessment year

PART B

7. List of associated enterprises with whom the assessee has entered into international transactions, with the following details :

(a) Name of the associated enterprise.

(b) Nature of the relationship with the associated enterprise as referred to in section 92A(2).

(c) Brief description of the business carried on by the associated enterprise.

8. Particulars in respect of transactions in tangible property.

A. Has the assessee entered into any international Yes/No

transaction(s) in respect of purchase/sale of raw

material, consumables or any other supplies for assembling/processing/manufacturing of goods/articles from/to associated enterprises?

If ‘yes’, provide the following details in respect of each associated enterprise and each transaction or class of transaction :

(a) Name and address of the associated enterprise with whom the international transaction has been entered into.

(b) Description of transaction and quantity purchased/sold.

(c) Total amount paid/received or payable/receivable in the transaction—

(i) as per books of account.

(ii) as computed by the assessee having regard to the arm’s length price.

(d) Method used for determining the arm’s length price [See section 92C(1)]

B. Has the assessee entered into any international transaction(s) Yes/No

in respect of purchase/sale of traded/finished goods?

If ‘yes’ provide the following details in respect of each associated enterprise and each transaction or class of transaction :

(a) Name and address of the associated enterprise with whom the international transaction has been entered into.

(b) Description of transaction and quantity purchased/sold.

(c) Total amount paid/received or payable/receivable in the transaction—

(i) as per books of account.

C.

(ii) as computed by the assessee having regard to the arm’s length price.

(d) Method used for determining the arm’s length price [See section 92C(1)] Yes/No

Has the assessee entered into any international transaction(s) in respect of purchase/sale of any other tangible movable/immovable property or lease of such property?

If ‘yes’ provide the following details in respect of each associated enterprise and each transaction or class of transaction:

(a) Name and address of the associated enterprise with whom the international transaction has been entered into.

(b) Description of the property and nature of transaction.

(c) Number of units of each category of movable/immovable property involved in the transaction.

(d) Amount paid/received or payable/receivable in each transaction of purchase/sale, or lease rent paid/received or payable/receivable in respect of each lease provided/entered into —

(i) as per books of account.

(ii) as computed by the assessee having regard to the arm’s length price.

(e) Method used for determining the arm’s length price [See section 92C(1)]

9. Particulars in respect of transactions in intangible property:

Has the assessee entered into any international Yes/No transaction(s) in respect of purchase/sale/use of intangible property such as know-how, patents, copyrights, licenses, etc.?

If ‘yes’ provide the following details in respect of each associated enterprise and each category of intangible property :

(a) Name and address of the associated enterprise with whom the international transaction has been entered into.

(b) Description of intangible property and nature of transaction.

(c) Amount paid/received or payable/receivable for purchase/sale/use of each category of intangible property—

(i) as per books of account.

(ii) as computed by the assessee having regard to the arm’s length price.

(d) Method used for determining the arm’s length

price [See section 92C(1)]

10. Particulars in respect of providing of services:

Has the assessee entered into any international transaction(s) in respect of Yes/No

services such as financial, administrative, technical, commercial services, etc.?

If ‘yes’ provide the following details in respect of each associated enterprise and each category of service:

(a) Name and address of the associated enterprise with whom the international transaction has been entered into.

(b) Description of services provided/availed to/from the associated enterprise.

(c) Amount paid/received or payable/receivable for the services provided/taken—

(i) as per books of account.

(ii) as computed by the assessee having regard to the arm’s length price.

(d) Method used for determining the arm’s length price [See section 92C(1)]

11. Particulars in respect of lending or borrowing money:

Has the assessee entered into any international transaction(s) in Yes/No

respect of granting/receiving loans/advances to or from associated enterprise?

If ‘yes’ provide the following details in respect of each associated enterprise and each loan/advance:

(a) Name and address of the associated enterprise with whom the international transaction has been entered into.

(b) Nature of financing agreement.

(c) Currency in which loan/advance granted/received.

(d) Interest rate charged/paid in respect of each loan/advance.

(e) Amount paid/received or payable/receivable in the transaction —

(i) as per books of account.

(ii) as computed by the assessee having regard to the arm’s length price.

(f) Method used for determining the arm’s length price [See section 92C(1)]

12. Particulars in respect of mutual agreement or arrangement:

Has the assessee entered into any international transaction with an Yes/No

associated enterprise or enterprises by way of a mutual agreement or arrangement for the allocation or apportionment of, or any contribution to, any cost or expense incurred or to be incurred in connection with a benefit, service or facility provided or to be provided to any one or more of such enterprises?

If ‘yes’ provide the following details in respect of each agreement/arrangement:

(a) Name and address of the associated enterprise with whom the international transaction has been entered into.

(b) Description of such mutual agreement or arrangement.

(c) Amount paid/received or payable/receivable in each such transaction—

(i) as per books of account.

(ii) as computed by the assessee having regard to the arm’s length price.

(d) Method used for determining the arm’s length price [See section 92C(1)].

13. Particulars in respect of any other transaction:

Has the assessee entered into any other international Yes/No

transaction not specifically referred to above, with associated enterprise ?

If ‘yes’ provide the following details in respect of each associated enterprise and each transaction :

(a) Name and address of the associated enterprise with whom the international transaction has been entered into.

(b) Description of the transaction.

(c) Amount paid/received or payable/receivable in the transaction—

(i) as per books of account.

(ii) as computed by the assessee having regard to the arm’s length price.

(d) Method used for determining the arm’s length price [See section 92C(1)].

**Signed

Name:

Address:

Place:

Date:

Notes: **This annexure has to be signed by __

(i) A chartered accountant within the meaning of the Chartered Accountants Act, 1949 (38 of 1949); or

(ii) Any person who, in relation to any State, is, by virtue of the provisions in sub-section (2) of section 226 of the

Companies Act, 1956 (1 of 1956), entitled to be appointed to act as an auditor of companies registered in that State.

3.3 The Creation of Transfer Pricing Documentation

3.3.1 Document Summary

For companies doing business with foreign related parties in India, creation of 3CEB will be required. If the transaction total annual with foreign related parties exceeds 10 million rupees, separately one must save the document stating the matters required by the tax authorities. If there is a false in the case and described what has been neglected this creation, 2% of the transaction price of the foreign-related transactions will be imposed as a penalty.

Tax authorities request the description as follows.

• Business Overview and capital structure of each related party, as well as the market, such as each related party makes a business

• Each related party in related party transactions to function and burden fulfill risk, as well as the goods or the contents of the provision of services and its trading stage, etc.

• Elected independent business-to-business pricing method is the best way reason and the calculation process, etc.

• Between the detailed data and independent company for the comparison target company pricing process, etc.

• Budget on the arm's length pricing, financial projections, assumptions and detailed documentation concerning the negotiation, etc.

3.3.2 Flow of document creation

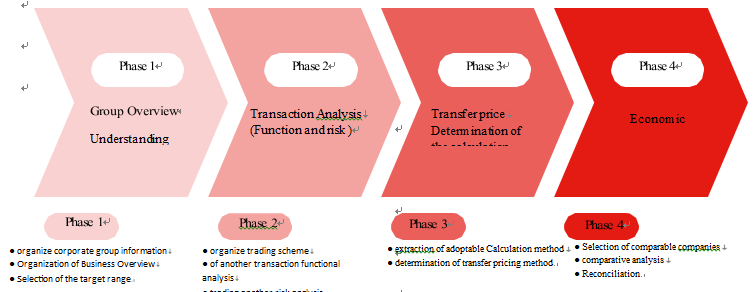

Process of document creation, will be followed roughly as shown in the description.

Following, details for each of the phases will be looked at:

Phase 1 - Fact analysis (Group Overview)

First, the entire outline group associated with the company is an overview of entities in India that shall be described including an overview of the company which belongs to the industry.

Specifically, History, companies such as shareholder composition overview, outline and each of activities of National companies, what kind of trading within the group has occurred, and a description of the various handling products, business background and business flow, customer segments and sectors of the group, value drivers and intangible assets, which is a business field industry trends, outlook, up to the position of the company in the industry, and then describes the information necessary to determine the transaction price.

Phase 2 - Transaction Analysis (Functions and Risk Analysis)

Transfer Pricing transactions actually take place pertaining to details of specific deals

Examples of Functional Analysis (Manufacturing)

Functions in a series of transactions carried out between affiliates are classified as follows (Continuous analysis in detail the features that are included in each):

- Before Production Stage

The research and development in the pre-production stage, such as intangible assets owned.

- Production stage

Procurement of raw materials, such as the ability of quality control, etc. at the time of production

- Logistics stage

The transport responsibility at the time of shipment of products such as inventory management responsibilities.

- Sales stage

Customer support, authority of pricing, marketing functions, and responsibility for claims.

- After-sales stage

For example, responsibility range for claims.

Examples of Risk Analysis

- Inventory Risk

Excess inventory, obsolescence, etc. Guarantee risk of such returned goods quality.

- Distribution risk

At the time of delivery damage, loss, risk of delay, etc.

- Credit risk

Receivables

- Setting of exchange risk

Trading Currency

For example if applied to the product of the manufacture and sale transactions, production from the stage of development, logistics, sale and it is possible to describe the functions and risks to sales after step, analysis of transaction in detail is continuous.

To describe and quantify in detail the burden rate, etc. between the importance of the degree and related parties of each of the business activities, analysis needs to be done.

Phase 3 – Determination of Transfer Pricing method.

From trading analysis one can select the most suitable and possible Arm's Length Pricing Method. The Transfer Pricing guidelines for multinational enterprises and tax authorities that have been issued by the OECD is conventional in the calculation of the Arm's Length Price. The traditional calculation method (independent price ratio quasi-method, resale price standard method) profit law (trading unit operating income method, profit split method), should be applied with reference to the revisions made on July 2010.

It should be noted that a similar tax reform in 2011 in Japan had been made.

OECD guidelines are not required to select a suitable method in order to evaluate the fair reasonable nature of TP in the enterprise. Analysis of comparison transactions for selection of the appropriate method, and reliability of the data is the important factor.

Phase 4 - Economic Analysis

From the most suitable method of choice in the calculation of the Arm's Length Price, selection of companies to be compared, the process up to the selection of the arm's length price.

Specifically, regional and year and financial data analysis results and selection subject, I will be in the election process, etc. of the target company (trading).

Main economic analysis matters

• Information of comparable companies

• Determination of the comparative year

• Selection of profit rate index

• Adjustment of differences (accounting adjustments, capital adjustment, accounts receivable adjustment, accounts payable adjustment, inventory adjustment)

• Range of arm's length price

3.3.3 Document the Contents of Details

Upon enforcement of transfer pricing, tax authorities not only corporate information with its own is, using a database of detailed data of the various countries of the companies have been recorded, with the profit level of similar companies that have been extracted from the database by comparison and comparison of the analysis results in the past similar projects, to determine the validity of the profit level.

For example, Japanese companies doing business in India export their products from Japan. In such a case where sales are through Indian subsidiary, etc., India tax authorities focus on the profit level of the Japanese subsidiary. If the profit level of the corporation is determined to be too high statistically in trade between the Indian corporation and the Japanese corporation, it is recognized that there is a high possibility of income transfer.

Authorities of Viewpoints for the foreign corporation, profit level of India corporation from a statistical point of view, will be the point of whether not too low.

3.3.4 Creating a Transfer Pricing Report Utilizing Database

For survey methods of tax authorities, each country has its own research means and there is also a part of the official’s judgment.

1. From the database, select the country of interest

2. To select the type of industry that should be the object of comparison

3. Other additional selection and its detailed information. (Ownership situation, the comparison period figures etc.)

4. Function, eliminating the companies that do not have similar by risk, etc.

From the huge database and its selection should be compared. Verification of Transfer Pricing on the basis of the profit levels of the company shall continue to be done.

In general, transfer in price economy analysis using the mean or median of earnings data of multiple selections have been the target company and verification is done.

In addition even if there is no deal to be very similar to the comparison, adjustments are also required.

-

Verification by Transfer Pricing Case

4.1 Proceedings Related to Transfer PricingAbout appeal relating to transfer pricing, alternative dispute resolution procedure (ADR) has been introduced from October 1, 2009.Taxpayers and ADR, it is a system that performs processing of disputes between three parties of the tax inspector and dispute resolution mechanism (DPR). Previously the dispute settlement in accordance with the transfer pricing taxpayers, tax inspector and tax commissioner (CITA: Commissioner of Income Tax Appeals) had been done between three parties.

For example, it required up to two years for adjudication of Tax Commissioner, prolonged appeal had been a problem. However, dispute resolution mechanism by the introduction of ADR is obliged to ruling within 10 months which became a possible conflict resolution in a short period of time.

4.2 The Transfer Pricing Litigation Cases in India

4.2.1 Marketing Intangible Assets

Case Study

January 23, 2013, ruling by the Special Court (SB) of Treatment of Delhi Tax Court of selling intangible assets for the L, Inc., a corporation of India (Marketingintangibles) (ITAT) has been published.

Company L of the relationship Company G is a corporation of Korea manufacturing electrical products and electrical appliances. Company L is a wholly owned subsidiary of Company G located in India. In Transfer Pricing study of Company L, Transfer Pricing Officer (TPO) is compared with the comparison target company. Excessive advertising was claimed to have been borne by sales promotion expenses (AMP).According to the TPO, the difference of Company L is intended to be incurred in order to spread Company G's brand and correction as is to be paid out to Company G. Further markup to AMP was also reasonable. It should be noted that the dispute resolution committee (DRP) have also supported this. Company L appealed to ITAT for this decision. ITAT is for Transfer Price adjustments related to AMP expenses. Company L was expended in connection with the creation and improvement of sales intangible assets for Company G in judgment and even has a mark-up which is recognized.

Issue

Issues in this case include the following:

Fact that L Corporation Company G Brand (G, Inc. legal owner) is promoting

Company L has the burden of AMP cost more than between independent companies price for Company G, the absence of a contract cannot be argued. And longer than the ratio between the independent companies (AMP cost of sales percentage) by Company L and Company G's brand advertising information, compensation should be determined.

Transfer Pricing as an International Trading

AMP expenses have been paid to a third party, service according to brand building only, those from Company L was made to Company G, as international trade, and is required to be adopted subject to the India of transfer pricing .

Point:

Advertising expenses related to the sale of products should be considered separately from the AMP cost according to the present brand-building. SB conclusion is also based on these facts. Transfer Pricing corrections authorities carried out on the AMP cost is reasonable for AMP cost. It must be determined that the mark-up is also reasonable.

On the other hand, with respect to the validity of the underlying cost and the rate of markup has been remanded to the authorities for reconsideration.

4.2.2 Transfer Pricing Taxation to India Subsidiary

Case Study

Tax court in September 2008, when a back tax based on the Transfer Pricing taxation against India subsidiary of Japanese companies Company S was made but denied the 5% Safe Harbor, application by the subsidiary, all taxpayers including the subsidiaries in the judgment of this 5% safe harbor were able to apply. It is a provision that deems the price (interest rate) and safe harbor provisions in the Transfer Price taxation in India. 5% rule for the calculation of the price is determined and the comparison as a result of the Transfer Price calculation methods is applied.

Issue

For the calculation of the Arm's Length Price in India of Transfer Pricing, whether or not to apply the safe harbor provisions became a major issue in this case.

4.2.3 Case to pay loan costs

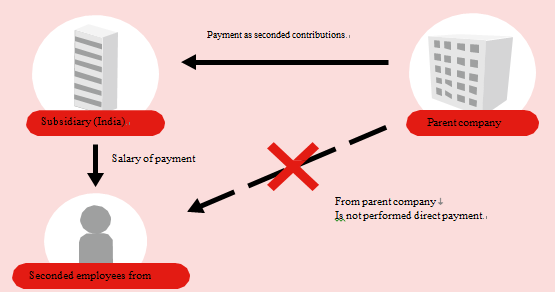

Case Scenario

Salaries of expatriates in a Japan parent company dispatched in the form of a loan to India subsidiary may pay through India subsidiary directly. The latter will be subject to Transfer Pricing transactions.

Issue

In the present case, Indian Company and the percentage of salary burden of Japanese corporation will be a problem. Salary amount based on the local level in the Indian side is to be borne. If the difference is paid in the Japanese side, usually cost processing is recognized for tax purposes in Japan side as "Salary Disparity Compensation Benefits".

-