Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaIndia

1 Chapter Introduction

-

-

Outline of the Draft Budget for 2014

■Outline of the draft budget for 2014

On 10th July 2014 the Government of India announced the Federal Government budget for Fiscal 2014, which will be the first time that Mr. Modi became the new government. It was the content of policy to promote infrastructure investment, industry growth and economic growth and fiscal consolidation. In infrastructure investment, I am planning to construct a high-speed railroad in an industrial area called "Diamond Hexagonal Project". In the same fiscal year we invest about 1 billion rupees (about 1.7 billion yen) and we are investing 70.6 billion rupees (about 119.3 billion yen) for 100 cities for modern urban development. We also approved port construction projects for 16 ports during FY 2014. In addition, we announced that we will invest 50 billion rupees (about 84.5 billion yen) for laying a 15,000 Km gas pipeline and building a warehouse for food distribution. We will make these investments and aim to realize economic growth rate of more than 7 ~ 8% after 16 years. In addition, we set the policy deficit to be a deficit of 4.1% of the gross domestic product (GDP) against 2014, and to lower it to 3% in FY 2016. It is estimated that 5,750 billion rupees (about 9.7 trillion yen) will be spent on the above-mentioned plan including infrastructure development. This will be a 27% increase compared to the previous fiscal year. Moreover, the goods service tax (GST) bill attracting attention from the past is expected to be passed within the year for the early introduction, and it is expected to be expected for companies and investors who are considering investing in the Indian market in the future. -

Outline of the Draft Budget for 2015

■Outline of the draft budget for 2015

Regarding infrastructure, an attempt to bring India to a world factory (Make in India Programmes Programs) was recommended and additional contributions of 700 billion rupees were added to infrastructure, of which 140 billion rupees were constructed for road construction, 1 , We plan to spend 100 billion rupees for railway construction. In addition to newly constructing a road with a total extension of 100,000 km throughout India, we will also construct five huge power plants (4,000 MW each) to eliminate power shortages. We will also establish an infrastructure fund (NIIF) and invest 200 billion rupees annually.

In connection with this, in terms of living environment, we will improve the power, water supply, road paved houses of 20 million cities and 40 million rural areas, and supply 20,000 rural areas by 2020, 17 We decided to build a road connecting 80 thousand villages, provide medical services to each city and village, and guarantee Senior Secondary School which can pass within 5 km to all children.

-

Direct Tax Change

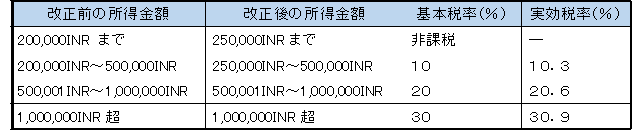

■Personal income tax(Income Tax Rate for Individuals)

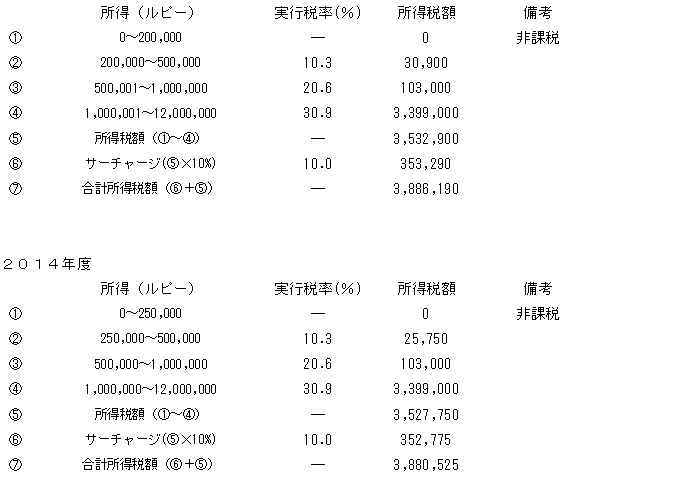

According to the budget plan for FY 2014, the minimum income taxable income of Indian residents under 60 years old was raised by Rs. 50,000 from Rs. 200,000 in 2012 to Rs 250,000. There is no change from the fiscal year 2011 as to the effective tax rate, which is calculated by adding 3% of education purpose tax to the basic tax rate.

The effective tax rate of personal income tax based on the budget plan for FY 2014 is as follows.

Tax exemption for elderly people who are residents of India from 60 to 80 years old was raised to 300 thousand rupees. Indian residents over 80 years old are tax exempt up to Rs. 500,000. Elderly people who do not earn income from the 2012 budget proposal do not need Advance Payment (planned payment).

Also, in the budget proposal for FY 2013, it is supposed to be surcharged for high income people on personal income tax. There is no change in the progressive tax rate, but if it exceeds 10 million rupees, we will charge additional surcharge 10%. Surcharge refers to tax on tax. In the income tax calculation of expatriates, many companies are incurring income taxes. Therefore, in the case of gross-up calculation of income tax calculation, taxable income tax amount exceeds 10 million rupees in many cases.FY 2013

The tax reduction effect of 5,665 rupees has been achieved since the taxable minimum income amount has been raised from 200,000 rupees to 250 thousand rupees.

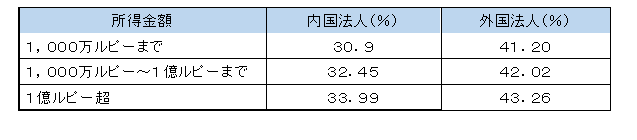

■Corporate income taxes(Income Tax for Domestic and Foreign company)

In the budget draft for fiscal 2014, there was no change in the corporate income tax rate. The education purpose tax 3% (Education Cess 2% + Secondary & Higher Education Cess 1%) remains the same as before. The effective tax rate of corporate income tax based on the budget plan for fiscal 2014 is as follows.Income tax rate 2014 (no change)

■Minimum alternative tax (MAT:Minimum Alternate Tax)

In the 2012 budget plan, the minimum alternative tax rate has been raised from 18% to 18.5%. If the corporate income tax calculated in accordance with the Indian income tax law falls below 18.5% of the profit (Book Profit) of the profit and loss statement prepared pursuant to the Companies Act, 18.5% of the profit is paid as the minimum alternative tax. In addition, the minimum alternative tax will be applied in the budget for 2012 to SEZ developers and companies in SEZ which were not covered so far. The minimum substitute tax paid can be offset against future corporate income tax, but its carry-off deduction period remains unchanged for 10 years as before. In addition, a surcharge (10%) and education purpose tax (3%) will be imposed up to 100 million rupees. For educational purpose tax (3%) only for Rs 100 million or more is imposed. There is no change in the minimum alternative tax in FY 2014. The effective tax rate of the minimum alternative tax rate based on the draft budget for FY 2014 is as follows.

*1 20.9605%(18.5%+Charge10%+Educational Cess3%)

*2 20.0077%(18.5%+Charge5%+Educational Cess3%)

*3 19.055%(18.5%+Educational Cess3%)

*4 20.0077%(18.5%+Charge5%+Educational Cess3%)

*5 19.4361%(18.5%+Charge2%+Educational Cess3%)

*6 19.055%(18.5%+Educational Cess3%)

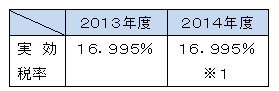

*1 16.995%=15%×1.03(Education Cess3%)×1.10(Additional Tax10%)

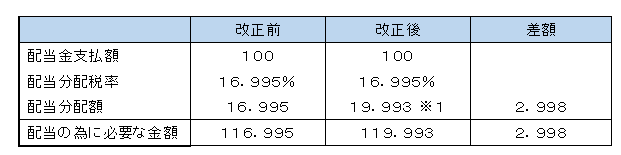

■Dividend distribution tax

In India, there is a system called DDT (Dividend Distribution Tax), and dividend payment tax paid by Indian domestic corporation will be subject to dividend distribution tax for corporate dividend payment corporation. In the draft budget for 2014, the tax rate of DDT has not changed from 15%. However, from October 1, 2014, the calculation method of dividend distribution tax will be changed to gross-up calculation. The effective tax rate of dividend distribution tax based on the budget proposal for FY 2014 is as follows.

Dividend distribution tax rate for 2014 (gross up calculation)

Calculation method of dividend distribution tax rate

*1 100 ÷ (100% - 5%) = 117.64 (dividend taxation after gross up) 117.64 × 16.995% = 19.993

The tax payment amount will increase because the dividend taxation amount becomes the amount after gross up.

■Withholding tax(TDS)

Handling of withholding tax (Tax Deducted at Source (hereinafter referred to as "TDS") was revised in the budget draft for FY 2014. 1) The deadline for deeming it to be a "nonperforming taxpayer" The deadline for the taxpayer to be regarded as a "nonperforming taxpayer" due to incorrect TDS deduction or tax payment has changed. Prior to the revision, taxpayers who declared TDS were two years from the end of the fiscal year that TDS declared. Taxpayers who did not declare TDS had a deadline of six years from the end of the fiscal year when payments and credits were made. However, after the revision, both parties were due 7 years from the end of the fiscal year when payment / credit was done. It was decided to be consistent with 7 years of the usual tax investigation deadline. 2) Denialization Denied for Unpaid Withholding Tax from October 1, 2014, if you do not do so with respect to personal income tax, or if you do not pay taxes on TDS for payment of expenses, the amount of non-deductible will be reduced to 30%. Before the revision, the entire amount was considered non-deductible.3) Expanding the scope of non-compliance deductibility provision The scope of the tax deductibility disapproval provision was expanded and all income targeted for withholding tax, including salary and executive remuneration, was covered. In addition, when paying tax withholding tax and paying taxes on the payment for nonresidents before the declaration deadline, it is now possible to include deduction for the payment.

■Tax Procedure Rules

According to the draft budget for fiscal 2014, regulations on compulsory investigation right, information request right, intentional submission of document documents etc., provisional seizure, and obligation to keep information documents have been established under the taxation procedure.

1) Compulsory research right

From October 1, 2014, the authority for tax authorities' investigation on withholding tax and withholding taxes has been expanded to comply with compliance. From now on, the possibility that the tax investigation notification to each company will reach from the authorities will increase.

2) Information claim right

After October 1, 2014, the tax authorities will be given a wide range of information claims. It became possible to conduct information and document investigation to verify the credibility of information from stakeholders who are useful and judged relevant to the survey. If the tax investigation enters, if the tax authorities are not satisfied with the documents submitted by the company, you can collect information separately from other stakeholders.3) Deliberately submit document documents etc

If deliberately failing to submit the document, it will be subject to penalties, it will be fortified 1 year or a fine.

4) Provisional seizure

If you fail to file a tax return / tax obligation, it will be possible for temporary seizure by the tax authorities after 6 months from the submission deadline. It is scheduled to be extended from deliberations by authorities related departments until 2 liter from October 1, 2014, or 60 days after the end of the survey / special investigation, whichever is later.

5) Provision of obligation to keep information documents

Regarding separately prescribed financial institutions, if information and documents concerning the transactions subject to survey are specified by the tax authorities, they are obliged to submit. If the stored information and documents are inaccurate, a fine of Rs. 50,000 will be imposed on the agency concerned.

■CSR activity expenses

According to the New Company Law in 2013, expenditure expenses related to CSR (Corporate Social Responsibility) activities are not considered to be expended as the purpose of the main business, and these expenses were not deductible under the provisions of the Income Tax Code. However, of expenses related to CSR activities, deductible expenses can be included as long as the separately prescribed conditions are satisfied in future expenses that are recognized as including deductible expenses under the Income Tax Code (such as personnel expenses).

■Tax return for specific individuals exempted from taxation

If the gross income amount exceeds the tax exemption limit amount for the following specific individuals exempted from taxation, it is necessary to file an income tax return.

>Mutual fund

>Securities trust

>Venture capital company

>Venture Capital Fund

In addition, investment trusts and securities trusts need to declare and pay income tax before distributing earnings. Venture capital firms and venture capital funds need to file tax declarations using Form 64.

■ Criteria for tax calculation and disclosureAlthough the central government has informed the standards on tax calculation and disclosure applicable to various taxpayers, in the budget draft for 2014, income tax calculation is performed according to the accounting standard notified under Section 154 (2) If not, there is a possibility that it will be taken for 2 years imprisonment or fine by judgment based on Section 144. Also, it is well-stated that the accounting standards notified under Section 154 (2) are not meaningful for keeping books. To this background, it seems that many Korean companies' expatriates have illegally processed the personal income tax calculation, so the personal income tax calculation for foreigners is more strict.

■ Introduction of special taxation system for real estate / infrastructure investment trusts

Investment related deductions based on Section 35 AD have been expanded for the laying and operation of slurry pipelines for the transportation of iron ore, which started operations on April 1, 2014, and the semiconductor wafer manufacturing industry in the 2014 budget proposal It was. Equipment subject to deduction was obliged to be used for 8 years for specific business. Also, if the condition is not satisfied after issuing the deducted claim, the amount deducted from the deduction amount already deducted from the amount of depreciation expenses at that time is regarded as business income and subject to taxation.

In the case of enjoying benefits based on Section 35 AD, there is no Tax Holiday right under Section 10 AA. Investment related deductions under Section 35 AD will be added in calculating tax adjustments for the calculation of AMT (alternative minimum tax). However, Depreciation expense based on Section 32 is subtracted for calculation of tax adjustments.

■ Tax incentives, tax exemptions and deductionsIn the FY 2014 budget plan, if the investment amount condition for new equipment is lowered from Rs 1 billion to Rs 250 million and the total investment of the equipment exceeds 250 Rs, the acquired amount 15 % Can be deducted for additional income. Target capital investment will be acquired from April 1, 2014 to March 31, 2017 and introduced. Also, if the facility is sold or transferred within 5 years, the additional deduction is taxed as a sale or business revenue in the transferred year. However, except in the case of joint ventures and dimmers. In addition, the applicable period of 5% reduction of the withholding income tax that can be applied for borrowing interest paid to nonresidents by foreign currency was extended to June 30, 2017. (The general tax rate according to the Indian domestic law is 20%, the reduced tax rate by the Japan-India tax treaty is 10%.) This reduced tax rate of 5% also applies to the interest on long-term receivables to all non-residents, including infrastructure receivables. The tax incentive measures will be effective from October 1, 2014. In Section 2 (14), the deadline of the 15% reduction tax rate for Indian companies receiving dividends from certain foreign companies ceased. Securities held by FII / FPI are regarded as fixed assets and have properties of income and capital gains obtained from the transfer of such securities. The change will be applied from FY 2014.

■ Indirect assignment and general tax evasion prevention provision (GAAR) and othersIt was the first budget since Mr. MODY, the new administration was established, but there are still cases where unclearness remains. Regarding indirect transfer, the fiscal year 2012 fiscal budget revised for the purpose of expanding the scope of source rules in order to grasp offshore transactions, and the implementation of retroactive application was also introduced. Expansion of the scope of source rules and implementation of retroactive application had a negative effect on investment sentiment, but there are no legal changes, but in order to respond to the investor's request the procedure from the Minister of Finance is to proceed Prior to implementation, mention was made to see deliberations at high commission level committees. However, unclearness remains for the consequences of the ongoing case. -

Indirect Tax Changes

■Tariff (Custom Duty)

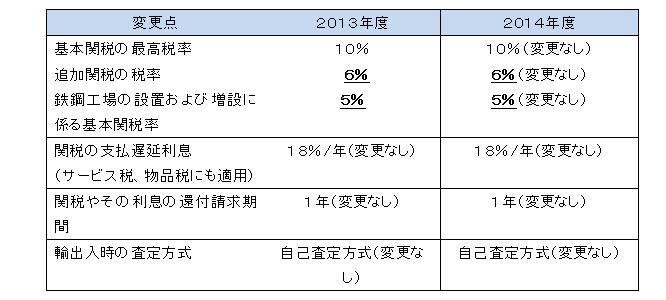

There is no change in the basic tariff rate (BCD: Basic custom duty), and the maximum tariff rate for basic tariffs remains at 10%, as is the year 2012, and the tax rate on the countervailing duty and the special addition duty is also unchanged. The execution tax rate will be 28.85% as before.

1. Baggage allowance increased from 35,000 rupees to 45,000 rupees.

2. For the purpose of promoting domestic manufacturing industry, streamline the mechanism that import duties are higher than sales goods tax, and the following industries will benefit.

→ steel, textile, renewable energy, food processing, packaging, oil, IT and electric machinery

3. the tariff rate on basic tariffs for propane gas, ethane, ethylene / propylene, etc. was lowered from 5% to 2.5%. The countervailing duty was 2%.

4. For certain parts used for photovoltaic generation, basic tariffs are exempted.

5. Basic tariffs are set at 5% and countervailing tariffs are set at 0% for manufacturing opportunities required for launching photovoltaic power projects.

6. Basic tariffs are exempted for 19 inches or less LCD / LED panels and certain panel parts.

7, Parts for PC manufacturing, parts and raw materials for wind power generation projects are exempt from special addition tariff if certain conditions are satisfied.

8. When export-oriented enterprises (EOU) import imported goods and materials and ship to domestic customs area (DTA), safe guard tariffs are also imposed in addition to normal tariffs.

9. AAR (Authority for Advance Ruling) which can confirm the handling of tax on future transactions in advance, residents and private companies in India became available from July 11, 2014.

10. Export tariffs on bauxite increased from 10% to 20%.

11. imported goods such as machinery for infrastructure projects were allowed to be disposed of at book value after depreciation but only importers were permitted, but other consortium members can now dispose of it.

Tariff rate on 2014 degree budget

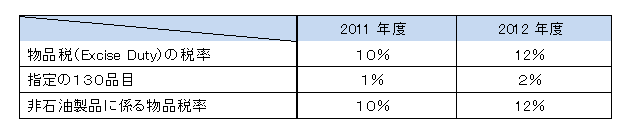

In the budget draft for FY 2014, the tax rate on excise tax has not changed since the previous fiscal year. The execution tax rate is 12.36%.

1. For the purpose of promoting the domestic manufacturing industry, the excise duty has been reduced from 11th of July 2014 for iron ore, food processing, packaging, shoes, electric machinery, wind power etc.

2. As part of dealing with concerns after the judgment of a company, the excise tax evaluation rules were revised. As a main content, if there is no inflow of additional consideration directly or indirectly to the manufacturing industry, there is a provision that the selling price of goods (even cost cracking) is the transaction price and becomes the tax base. This has been enforced on July 11, 2014.

3. With respect to the delay of payment of excise tax, we paid excise tax every time we ship individual goods until we paid the unpaid item tax with delayed interest until now. In the future, penalties of 1% are imposed monthly if exceeding 1 month. It is necessary to pay along with late interest. It applies from October 1, 2014.4. Although it was tax exempt for the original contractor to manufacture the product in the international competitive bidding (ICB), there was a tax battle in the case of subcontractors manufacturing and supplying to the former contractor., Which was also clarified as a tax exemption.

5. Payment of a fixed amount of deposit or penalty or both of the predetermined tax amount separately makes it unnecessary to apply for a grace period separately. Until now, when appealing, deposit payment was not required. 7.5% appeal to the first stage (Comm (A) or Tribunal), 10% appeal to the next stage (Tribnal), up to a deposit of Rs 100 million, applied since the fiscal bill was formed.

Main change of excise tax in 2014 degree budget

In the FY 2014 budget plan, the tax rate has not been changed and the effective tax rate remains at 12.36%. The following items will be deleted from the negative list. The enforcement date is the president's approval date.

> Sales of advertising space other than print media are subject to taxation

> Wireless taxis are taxable at a reduction rate of 60%

The following items will be deleted from exempt subject. The effective date is the same day.

> Clinical trial> Passenger transport machine of air conditioning month vehicle

> When an educational institution receives a real estate royalties such as an educational institution, a classroom, etc., it is tax exempt only for the specific service of the educational institution.

The following items will be expanded from the exempt subject. The enforcement date is July 11, 2014. In case

> Indian travel company services to foreign travelers who participate in tours outside of India

Below are other major revisions. The enforcement date is the president's approval date.

> Time restriction provision until ruling

> Penalty exemption is limited only to cases within normal restriction period

> It is unnecessary to apply a grace period for the balance. However, in order to appeal, it is necessary to pay a deposit of 7.5% - 10%.

> When importing goods and doing improvements and engineering, the "destination" condition of goods and services has been changed to actual results. If the place of offer is India it will be subject to taxation.

> When doing brokerage work of goods, the place where the intermediary service is performed becomes the "offering place" of goods and services, and in the case of India it is subject to taxation.

> When delaying 6 months, there is a significant increase in delayed interest rate (24% to 30%)

> Taxable amount of goods transported by ship was reduced from 50% to 40%. In other words, the effective tax rate is 4.944% (12.36% x 40%)

> When using mixed tax rates for mixed contracts of goods and services, we have unified the reduction rate of 30% with respect to the assessment of the price of the service portion of the contract work, the service portion is 70% (formerly "other contract work "Was 60%," repair, maintenance, goods service "was 70%.

> The domestic reverse charge provision is enforced on the same day in the case of the following services.

> Services for directors' corporate entities

> Collection support service to banks, financial institutions, NBFC

■ CENVAT Credit

In the FY 2014 budget proposal, an expiration date has been set for the input of credits (purchase tax credit) of inputs and input services, so-called CENVAT credits. Within 6 months, credit rights will expire if credit is not stated. Also, in the case of reverse charge, credit can be credited at the time of payment of service tax, regardless of whether or not the claim price has been paid. (Credit was possible only when payment for service has been paid so far). In the future large-scale taxpayers will not be able to replace credits within the company.

-

Goods and Service Tax

■Goods and Service Tax

In the budget bill for FY 2014, it was announced that it will approve the introduction schedule of goods and service tax (GST: Goods & Service Tax) within the year on the conclusion on the introduction method. Goods and service tax (GST: Goods & Service Tax) is aimed at simplifying complex indirect taxes in India and unifies indirect tax such as excise tax, service tax, state VAT and central sales tax I am aiming for that. Although the actual introduction timing and tax rate etc. are not announced at the local point, it is expected that some expression will be made for introduction within the year. However, as concerns, there are things such as handover of tax collection right in each state, guarantee, legal improvement, etc. If these concerns are not cleared the introduction may be postponed. Future trends are drawing attention.

-

Major Changes in Transfer Pricing Taxation

■ Retroactive application of advance confirmation system (APA)

The FY2012 budget proposal introduced an advance confirmation system (APA: Advance Pricing Arrangement) to obtain agreement in advance from the Indian Tax Authority on how to calculate the transaction price among affiliates. This preliminary confirmation system was valid for five years or the period described in the advance confirmation system, and the application start was July 1, 2012. For the purpose of improving the prolongation of litigation concerning the transfer pricing taxation this time, the 2014 budget proposal can apply retroactively for the past four years before the business year that started APA. The requirements and procedures for retrospective application and the details of specific application will be announced at a later date, but it will be possible to retroactively apply from October 1, 2014. In addition, the first case since the start of the preliminary confirmation system in India since FY2012 is approval for dealing with Mitsui's Indian subsidiary in India and Mitsui India in December 2014. In order to avoid taxation of transfer pricing between the two companies, India and Japan's tax authorities have applied the preliminary confirmation system (APA) that this transaction is valid.

■Introduction of concept range concept of Independent Intercompany Price (ALP)

Under the Indian Income Tax Law, when calculating actual international transactions and Arm's Length Price (ALP), the average of multiple calculated values will be treated as ALP. (Arithmetic average) Also, if the difference between the actual international transaction and the independent company price is within ± 5% in the 2012 budget plan, the transaction price was considered valid, the range of the difference has been changed to "± 3%". In the 2014 budget proposal, we announced the introduction of the range concept aiming at calculating an appropriate price from international concepts. In addition, we mention the adoption of arithmetic average when the number of companies to be compared is insufficient. From now on, we need to be careful what kind of specific provision will be announced.

■ Changes in deemed international transaction definition

In deemed international transactions, regardless of nonresidents, if either or both of the enterprises or related companies are nonresidents, deemed international trade is also applicable for dealings between Indian residents, regardless of nonresidents. It is applied from April 1, 2015.

■ Use of data for multiple yearsUnder the regulation of the India transfer pricing taxation, the information used for comparing and analyzing overseas related transactions and transactions between independent companies was applied to the tax year in which foreign transactions were conducted. However, if the information is within two years before the taxable year, if the information affects overseas related transactions that are subject to this information, use data of multiple years so that it can be used as valid information we are making suggestions.

■ Grant penalty imposing authority to transfer pricing tax officer (TPO)Currently, under the provision of the India Transfer Pricing Taxation, there is an obligation to create transfer pricing documentation, and in the event of failure to make, the assessing officer or the lower appeal authority can impose a maximum penalty of 2% on foreign transaction volume, though a proposal was given to give authority to the transfer pricing officer (TPO) as well. Currently, Transfer Pricing Officer has the authority to disclose evidence, related documents, interrogation etc. to companies. Issuance of this revision is proposed from October 1, 2014. According to the 2015 budget plan, the target standard for transfer pricing in domestic transactions has been raised from Rs. 50 million to 200 million rupees.

-

Latest News & Updates

【GST latest information】

At the GST Council Meeting held on May 15, 2017, the introduction of GST was agreed on July 1st in all provinces except West Bengal. Although this final guideline has been announced, the format of the declaration form can be confirmed on the online site of the Central Board of Excise and Customs. Also, at the Council Meeting held on May 18th in Shrinagar City, the GST target items were classified into 98 categories, and a tax rate on 1211 items was announced in all. For the most part, a tax rate of 18% will be applied, but different tax rates will apply depending on each item and kind, so I think that you can confirm this.

[Overview]Indirect taxes that are subject to unification include, but are not limited to, countervailing duties, special additional duties, excise duties, service tax, central sales tax, state value added tax, transboundary tax, entertainment tax, luxury tax, Indirect taxes will be unified into GST. As for the cost side of the company side, it is thought that tax burden will be alleviated as a whole. The biggest impact is the two tariffs (offset tariffs, special addition tariffs) excluding basic tariffs and the central sales tax that occurs when purchasing goods across the state. Up to now, in the case of companies other than manufacturers (excluding first stage dealers), purchase tax deductions are not allowed for offset duties and special addition duties, and trading companies have been forced to pay a large tariff burden. In addition, when purchasing goods across states, tax is imposed on the central sales tax that does not allow purchase tax deductions, which was a cost to the company.

[Benefits to companies]Even after the introduction of GST, even if the offset tax deduction was not previously granted, the tax can be deducted from the provisional GST by unifying it into GST. This will lower the purchasing cost for the company and ultimately establish a mechanism whereby end users will be responsible for taxes.

[Issues of Japanese companies entering India and points to keep in mind]On the other hand, on the practical side, it is necessary to make a declaration three times a month for each state where each site is located, 37 times per year. For companies with multiple bases, the monthly declaration work will be the task for the future. Until now, the movement of stocks across the province will be taxed as IGST after July, if it is not subject to indirect tax. Since IGST is a tax that can be deducted for purchase taxation, although it will not be an additional cost to the company, spending will be temporarily involved, so we need to think carefully about cash management. Also, it is necessary to pay attention to changes in invoices. Since the method of issuing differs depending on the sale of goods or the provision of services, please check below.

"When selling goods"· Issued at the timing of supply of goods

· Issued in 3-page spelling (for us, for forwarding companies, for forward forwarding)

· HSN (Harmonized System Nomenclature) code required

· It is necessary to describe the address of the supplier

· Invoice number is alphanumeric and less than 16 digits

"In the case of provision of service"

· Invoice is issued within 30 days from the completion of service

· It is necessary to write SAC (Service Accounting Code)

-