Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaMalaysia

2 Chapter Investment Environment

-

-

Latest News & Updates

【Regarding foreign currency capital restrictions on export companies】

It is anticipated that Malaysia, a trading country, will suffer a great deal of damage once Pres. Trump, the US new President, announced that it will abolish the TPP policy once again. Also, according to the IMF's announcement, Malaysia knows that the outlook for foreign currency reserves at the end of the year is $ 100 billion (about 11.3 trillion yen) and short - term foreign debt has deficit of 128.2 billion dollars. In the November foreign exchange market, the Malaysian Ringgit (Ringgit) performance against dollar is the worst among the emerging market currencies in Asia and its outflow of capital among emerging markets are reported to be the weakest.

Against this backdrop, the Malaysian Central Bank announced capital restrictions on foreign currency last December 2 in order to stop the ringgit depreciation. This regulation was being imposed from December 5 (Monday). Below is the Japanese translation of the content on the website of the Central Bank of Malaysia.

The outline of the regulation is as follows for eligible export companies:

1) Exporters must retain only up to 25% of export proceeds in foreign currency as against 100% done at the present. They may, however, hold high balances with approval from BNM to meet their obligations in foreign currency.

Presently exporters can possess 100% foreign currency money acquired from the exports. However because of the new regulation, the possession will be limited to as low as 25%. The possession of more than 25% is possible upon the permission of the Central Bank.

2) Payment by resident exporters for settlement of domestic trade of goods and services is now to be made fully in ringgit.

In the future, it is necessary to do all domestic transactions (goods and services) with ringgit. Exporters cannot use foreign currency.

Through the special accounts of all banks, the ringgit which the exporter acquired from export (after money exchange) will be applied an interest rate of 3.25% per year, which is higher than the market interest rate. This measure will be applied until December 31, 2017 but will be subject to further review.

4) Exporters are also able to hedge and unhedged up to six months of their foreign currency obligations.

Exporters can hedge foreign currency assets and liabilities up to six months.

The main point is that export companies will be able to hold up to 25% of foreign currency until that time will need to hold ringgit in domestic transactions. Government's intention is to stop the current situation where the value of ringgit will stop declining and capital out flows will be visible through.

【About the business license in Kuala Lumpur city】

The main purpose of mandating to secure business license in Kuala Lumpur is to crack down many illegal stalls that are built in the city.

Companies that acquire business license must meet either of the following requirements:

a) Investment of 50% or more from individual shareholders in Malaysia

b) Malaysian citizenship employees must be 50% or more of the total number of employees to be hired.

All companies Doing Business in KL.

However, if your company was approved as "Management Office", you do not have to fulfill this regulatory requirement.

* Although detailed definition of Management Office is not fixed and is supposed to be changed by the officer, basically, a Management Office should not buy or sell any goods in the site of business that they applied for. If they do so, their business office will be subject to inspection after receiving an "Appeal Letter".

Opinions of the officials are divided as to whether to apply this regulation when renewing a business license. For some officials the application of the regulation is unnecessary while others believe that it is a responsibility to apply the regulation. However, many officials approved to apply this regulation even at the time of renewal. So they also think of better direction or way in applying the regulation.

The following are the steps to be taken for first time application. It is said to be probable that upon using the new regulation, the same process of application will be followed.

1. Application

* Here, "Reject Letter" will be issued from DBKL if the above requirements are not satisfied.

2. Issue "Appeal Letter" for "Reject Letter"

※ In "Appeal Letter", fill in capital structure, business location, business purpose etc. Also, temporary business license will be issued after receiving "Appeal Letter". Because the main objective of the regulation is to prevent outdoor and small scale fraud caused by as street vendors, as per the official in charge, for the possibility of the approval of "Appeal Letter" received from restaurants and retail stores in shopping malls and hotels owners is strong.

3. Visit by DBKL official

Here, after submitting "Appeal Letter", inspection officers without prior notice will do the inspection if more than 50% of the total employees who applied in the office are Malaysian citizen and the business is located in the appropriate location.

4. After inspection, issue this business license

This is the issuance of a business license where application of new regulation starts.

However, due to the nature of Malaysia, I think it will take a long time for everyone to proceed in the same way. In addition, although we talked with several officials this time, we feel that further investigation is necessary for issues such as differences in opinions of each officer. -

Investment regulation

Malaysia is a multinational country where Malay, Chinese and Indian people live, and economic disparity among ethnic groups was a problem.

Malaysian individuals and indigenous people, as defined in the Federal Constitution, are called Bumiputera. The overall policy for preferential treatment and protection for Bumiputera is called "Bumiputra Policy". This policy has functioned not only to eliminate on Malays' economic disparities but also serves asr foreign capital regulation. The purpose of Bumiputra Policy is to support Bumiputera companies, to improve the educational environment of Bumiputera, and to support employment.

However, recently Bumiputra Policy regulating on the establishment of foreign capital enterprises have been greatly relaxed. This results in permitting a 100% foreign capital investment in most industries especially manufacturing to enter the country. However, the former regulation remains in the service industry, especially in the wholesale and retail sector, such as convenience stores. -

Prohibited industries

In the "Guidelines on Foreign Capital Entry into Malaysia Distribution Transactions and Services" announced in 2010, the lists of business related in distribution industry, retailing, wholesale industry stipulated as follows are not allowed to enter the market with foreign capital investment:

· Supermarket, mini market (Sales floor area is less than 3,000 m 2)

· Grocery store, general store

· Convenience store (open 24 hours)

· Newspaper dealerships, grocery stores

· Pharmacy (a pharmacy that sells traditional herbs and herbal medicines)

· Gas Station (Including Convenience Stores)

· Permanent market (wet market)

· Permanent walkway store

· Business related to the strategic interests of the state

· Cloth shop, restaurant (non-high-end shop), bistro, jewelry store etc.

-

Investment ratio · Capital regulation

Besides to prohibition in some industries, restrictions on investment ratio and minimum paid-in capital regulation are established for each industry.

① Business established for the benefits of national interests

For businesses related to national interests (areas related to national interests such as water, energy and electricity supply, broadcasting, defense, security, etc.), foreign capital entry is limited to 30%.

② Manufacturing industry

In the manufacturing industry, 100% foreign capital entry is permitted in most companies, no capital requirements are imposed. However, if you are going to enter the manufacturing industry you will need a license issued by the Ministry of International Trade and Industry (MITI) and apply to the Malaysia Investment Development Authority (MIDA). Acquisition of this license is obligatory for manufacturing companies with shareholder's equity of 2.5 million ringgit and employees of more than 75 employees.

③ Service industry

For the service industry, except industries dealing with rendering service and selling goods at the same time like(petroleum products, pharmaceuticals, harmful substances, etc.) separate laws in the logistics industry, wholesale / retail industry and others being prescribed. The minimum paid-in capital amount for a pure service company is set as one million ringgit.

The jurisdiction body over the service industry is domestic trade, cooperative association and consumer Ministry (MDTCC).

Each industry will be described in details below.

(③.1) Logistics industry

In the logistics industry regulations are particularly strict, and capital regulations are set according to the type of industry. Refer to the table below..png)

(③.2) Wholesale and retail trade

Regarding the wholesale / retail industry, the capital requirement varies depending on the form of dealer. See as follows.

A hypermarket refers to a dealer with a sales floor area of 5,000 m 2 or more while a supermarket refers to a dealer with floor area that is over 3,000 m 2 but less than 4,999 m 2.

.png)

-

Other regulations

① ExchangeForeign exchange regulations are set forth in the Financial Service Act 2013 (Financial Service Act 2013) and the Islamic Financial Service Act 2013 (Islamic Financial Service Act 2013) as follows..png)

② Land ownership regulationIn the case of acquiring real estate property under the conditions falling under the following categories, it is necessary to apply to the Prime Minister's Economic Planning Agency based on the "Guidelines on Acquisition of Properties" (Guideline on the Acquisition of Properties).

.png)

① Restriction on employment of foreign representative

Foreign-affiliated companies are allowed to hire foreigners in areas where Malaysians with required expertise are not available. However, in order to protect the employment of Malaysian citizens, Malaysian are trained in various jobs and technical skills are being improved. Restrictions are being imposed on the number of foreign resident expatriates who can be dispatched by foreign-funded enterprises and the allowable period of their stay.

Categories of foreign resident staff who can be dispatched are according to job type, key post, time post, etc. The number of people accepted in each post depends on the business contents. In areas and businesses where training is the focus ofthe government, authorization of dispatch becomes easier (see table below)..png)

.png)

In addition, expatriates staying for more than two years must acquire a managerial position called Employment Pass and a work visa for professionals.

To obtain employment pass, there are conditions to be satisfied such as minimum salary of 5,000 ringgit per month, employment contract period minimum 2 years, minimum capital (see table below) etc..png)

④ About employment of localsIn addition, the Malaysian Employment Act (Employment Act 1955) prohibits the dismissal and reduction of local personnel to prioritize the employment of foreigners if the local personnel possessed the necessary abilities required by the company. (Article 60N of the same Act).

-

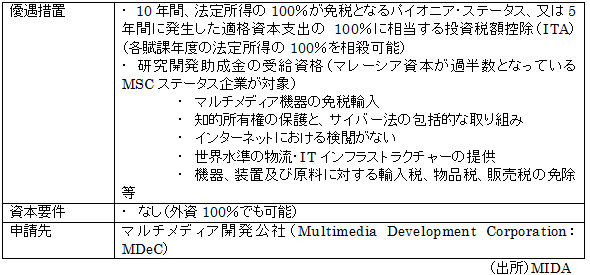

.png)