Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaBangladesh

6 Chapter Tax

-

-

Latest News & Updates

[Habitability and tax rates of branches]By the tax law revision in July of last year (2016), the tax rate on the provision of services to nonresidents has become higher than the tax rate for providing services to residents. For that reason, we need to pay attention to the tax rate when we provide services to overseas corporations and obtain compensation.Based on Article 2 55 of the Income Tax Act, residents are defined as all companies that conduct Bangladeshi company or all of Bangladesh's administration and management, so in addition to foreign companies outside Bangladesh, foreign corporations The Bangladesh branch of Bangladesh is also considered to be a non-resident under the tax law.Article 2, paragraph 55 of the Income Tax Act (definition of "resident") "Resident" in respect of any income year, means- (c) a Bangladeshi company or any other company that control and management of its affairs is situated wholly in Bangladesh in that year.However, regarding branches of a Japanese corporation, there is provision that Article 4 of the Japan - Bax Tax Convention does not impose a higher tax rate than resident.Article 4 of the Japanese-Japanese tax treaty"A tax on a permanent establishment (*) that a company in one Party has in the other Contracting State shall be taxed in the other Contracting Party for the taxpayer of the other Contracting State Party performing similar activities "Permanent facilities" refers to places where you do business, such as a representative office or a branch office.Bangladesh If domestic and domestic tax laws and the contents of the tax treaty differ, either one of the more advantageous one will be applied. In this case, with the Bangladesh Income Tax Law, the withholding tax for providing services to non-residents of Bangladesh (branch) is set higher than that of Bangladeshi residents (local corporations), whereas the Japan-Vietnam DTA treats " The provision that the tax on the branch of the Japanese corporation (the permanent establishment in the other Contracting State) will not be more disadvantageous than the tax imposed on Bangladeshi residents (= the parties in the other Contracting Party) " Yes. For that reason, for the Bangladesh branch of the Japanese corporation, the tax treaty takes precedence and the tax rate similar to Bangladesh resident (local corporation) is considered to be imposed. -

personal income tax

When calculating personal income tax, it is first necessary to judge whether the target person is "resident" or "non-resident", that is, the subject's residentiality in Bangladesh. Due to this comfort, the range of income on which personal income tax is imposed is greatly different.The definition for each category is as follows.■ Definition of residentsThe definition of the resident in Bangladesh shall satisfy any of the following requirements.

(1) When the cumulative staying days in Bangladesh at the taxing period (July 1 to June 30 *) is 182 days or more

* Taxation period for personal income tax in Bangladesh is generally from July 1 to June 30 th the following year. However, if there are special reasons for business and permitted by the tax authorities, a special taxation period different from the above period can be adopted.

(2) If you have stayed in Bangladesh for 90 days or more within the taxable period and the total of the staying days in the past 4 years exceeds 365 days.jpg) Due to the difference between the above categories of resident and nonresident, the scope of income taxed will differ as follows.

Due to the difference between the above categories of resident and nonresident, the scope of income taxed will differ as follows..jpg) Regarding these incomes, it does not matter whether it is a place of receipt of income or a resident / nonresident. The income which does not correspond to the above domestic source income will be foreign source income.In other words, if you become a "resident" in Bangladesh, you will be taxed in Bangladesh not only for income in Bangladesh but also for income generated in other countries. In this case, tax will be doubly charged as much as foreign source income, so the Bangladesh side will adjust the amount of tax payment under the provision of "foreign tax credit".In addition, if it is regarded as a non-resident, only income generated in Bangladesh will be taxed in Bangladesh and other foreign income will be taxed in the country of residence.However, in Bangladesh 's tax law, residents who stay in Bangladesh for a cumulative stay of more than 182 days, or stayed in Bangladesh for 90 days or more within the taxable period, and the number of days stayed in the past 4 years is 365 days It is defined as exceeding.However, in Japan 's Income Tax Law, individuals with domicile in Japan or individuals who have residence for more than one year to date have been defined as residents, so in certain cases, in both Japan and Bangladesh Under the accreditation of residents, income tax will be doubly taxed in both countries. If it is necessary to travel frequently to Bangladesh subsidiaries etc for support of launching of a manufacturing subsidiary that has just been established, etc., and as a result the cumulative number of stayed days reaches 182 days There are not many cases that fall under double taxation.In such a case, based on the tax treaty between the two countries, after judging which countries have habitability, they will declare tax payments respectively.

Regarding these incomes, it does not matter whether it is a place of receipt of income or a resident / nonresident. The income which does not correspond to the above domestic source income will be foreign source income.In other words, if you become a "resident" in Bangladesh, you will be taxed in Bangladesh not only for income in Bangladesh but also for income generated in other countries. In this case, tax will be doubly charged as much as foreign source income, so the Bangladesh side will adjust the amount of tax payment under the provision of "foreign tax credit".In addition, if it is regarded as a non-resident, only income generated in Bangladesh will be taxed in Bangladesh and other foreign income will be taxed in the country of residence.However, in Bangladesh 's tax law, residents who stay in Bangladesh for a cumulative stay of more than 182 days, or stayed in Bangladesh for 90 days or more within the taxable period, and the number of days stayed in the past 4 years is 365 days It is defined as exceeding.However, in Japan 's Income Tax Law, individuals with domicile in Japan or individuals who have residence for more than one year to date have been defined as residents, so in certain cases, in both Japan and Bangladesh Under the accreditation of residents, income tax will be doubly taxed in both countries. If it is necessary to travel frequently to Bangladesh subsidiaries etc for support of launching of a manufacturing subsidiary that has just been established, etc., and as a result the cumulative number of stayed days reaches 182 days There are not many cases that fall under double taxation.In such a case, based on the tax treaty between the two countries, after judging which countries have habitability, they will declare tax payments respectively.

■ Income AmountFirst of all, it is necessary to distinguish taxable income from non-taxable income from all income in the taxable year.Taxable income is classified as follows. (Direct Tax Law Article 15)·Employment income· Real estate income· Agricultural income· (Corporate or individual) business income·Capital gain· Other incomeWhen calculating the total income amount, you can deduct a certain amount as the amount spent to earn that income according to each classification. Specifically, the list is as follows..jpg) For each income amount, the total amount minus expenses etc. to be deducted is totaled, and the total income amount is calculated.

For each income amount, the total amount minus expenses etc. to be deducted is totaled, and the total income amount is calculated.

■ Tax calculationCalculate the income tax amount by multiplying the gross income amount calculated above by the progressive tax rate shown below. The income tax rate is 1. General male, 2. Women, older people 65 years and older 3. Disabled person 4. Non-resident, depending on the classification.

【Personal income tax rate】

The personal income tax rate has been changed as follows according to the 2015 - 16 national budget proposal..jpg) The income tax rate before revision is as follows.

The income tax rate before revision is as follows..jpg)

.jpg) For nonresidents, it is not progressive taxation, but it is uniformly 25%.In addition, with regard to dividend income, separating taxation takes 20% income tax apart from the above tax rate.■ Minimum alternative taxIn Bangladesh, even if it is a taxpayer who is tax-exempted in the personal income tax rate table above, if the tax payment amount is less than 2,000 takka, there is an obligation to pay 2,000 hak as a minimum alternative tax. In addition, 3,000 hawks in the city and 1,000 taka in the suburbs are applied. However, in order to alleviate the complexity of the procedure, it is a move to unify the tax price in the future.

For nonresidents, it is not progressive taxation, but it is uniformly 25%.In addition, with regard to dividend income, separating taxation takes 20% income tax apart from the above tax rate.■ Minimum alternative taxIn Bangladesh, even if it is a taxpayer who is tax-exempted in the personal income tax rate table above, if the tax payment amount is less than 2,000 takka, there is an obligation to pay 2,000 hak as a minimum alternative tax. In addition, 3,000 hawks in the city and 1,000 taka in the suburbs are applied. However, in order to alleviate the complexity of the procedure, it is a move to unify the tax price in the future.

■ Declaration / Payment Procedure① Tax return / paymentWith regard to income taxation in Bangladesh, income of the taxable year will be declared and taxed to the local tax office by the end of September of that year.In returning to Japan, when an assignee residing in Bangladesh returns, he / she will declare and pay tax before returning home (Direct Tax Code 184).② Intermediate declaration / paymentIf the income of the previous tax year is over 400,000 Taka, or if it is predicted that the income will exceed 400,000 hu in the tax year without declaration in the previous year, unless taxes are distributed evenly every quarter It will not (direct tax law Article 88).Regarding the deadline, the first quarter will be September 15, the second quarter will be December 15, the third quarter will be March 15 and the fourth quarter will be June 15 It is (direct tax law 89 Article).

· Fiscal Year 2015September 15: Planned tax payment (1st time in 2015)September 30: Tax return for 2014Scheduled payment on 15th December (2nd in 2015)· FY 2016Tax payment planned on March 15 (3rd in 2015)Scheduled payment on June 15th (4th in FY 2015)September 30: Tax return for 2015

③ Penal ProvisionsIf the person who should make a final tax return does not make a declaration, a penalty of 10% or 1,000 huge of the amount of taxation, whichever is larger, is additionally charged as penalty fee.In addition, if you delay your tax payment, 5% of the delay amount, 20% for the second time and 25% for the third time will be taxed for the first time. -

Corporate income taxes

■ TaxpayerTaxpayer of corporate income tax in Bangladesh shall be liable for all corporations and unions (hereinafter "domestic corporations") established under the laws of Bangladesh, and corporations and unions (hereinafter referred to as "foreign corporations" ), And it is said that they will operate business in Bangladesh. With this classification, the range of income to be taxed will vary greatly.Domestic corporations include not only all corporations and unions established under the laws of Bangladesh but also corporations and unions that are substantially controlled and operated by foreign companies in Bangladesh.

■ Calculation method of taxable incomeTaxable income in the direct tax law is calculated by deducting the amount of all deductible from the amount of all gains on the business that was executed during the accounting period. The taxable year is assumed to be 12 months (Direct Tax Code Article 14 (1)). Corporate income tax will be imposed on the calculated taxable income.■ Calculation method of taxable income.jpg) · Costs attached with appropriate and complete bills and vouchers required by law

· Costs attached with appropriate and complete bills and vouchers required by law

For tax purposes, expenses permitted to be deducted are limited to appropriate and effective costs or losses. In other words, expenses not directly involved in earning income, costs not supported by related vouchers, or expenses not meeting the conditions of related laws and ordinances can not be deductible for tax purposes.The tax office has the right to decide the appropriateness of revenue and expenses and the judgment of effectiveness. Below, we will explain the main provisions stipulated in the Corporation Tax Law in calculating income amount.

Depreciation cost

In calculating tax depreciation expenses in Japan, we calculate based on "acquisition price", "depreciation method", "useful life" prescribed on tax.However, in Bangladesh, the amount that can be deducted as depreciation expense is calculated by multiplying the acquisition price by the depreciation rate specified by the direct tax law (Direct Tax Code 27 c). In addition, the calculated amount can be included in the amount of deductible as the limit amount.

① Acquisition priceThe acquisition price of the asset is the sum of the expenditure purchase price plus incidental expenses (customs duty, interest on purchase funds, transportation fee, insurance fee, renovation cost, installation cost etc).

② Amortization rateThe depreciation rate of depreciable assets is stated in Direct Tax Law 8th Schedule A and is stipulated in the table below according to the classification of assets..jpg) Depreciation of intangible assetsFor intangible fixed assets (patent rights, trademark rights, etc.), calculate by dividing the amount spent for that acquisition by the useful life. If the use period is less than 1 year, it is calculated on a daily basis.Those with a useful life exceeding 10 years or those whose useful life is unknown are calculated assuming that the useful life is 10 years (Direct Tax Law 8th Schedule D4). In addition, due to the tax law, there is no clear amortization period defined for each individual asset, so it is necessary to set the depreciation period arbitrarily within this range.In the event that the intangible asset is disposed of or the rights expire in the period, amortization expenses can not be recorded in the taxable year.

Depreciation of intangible assetsFor intangible fixed assets (patent rights, trademark rights, etc.), calculate by dividing the amount spent for that acquisition by the useful life. If the use period is less than 1 year, it is calculated on a daily basis.Those with a useful life exceeding 10 years or those whose useful life is unknown are calculated assuming that the useful life is 10 years (Direct Tax Law 8th Schedule D4). In addition, due to the tax law, there is no clear amortization period defined for each individual asset, so it is necessary to set the depreciation period arbitrarily within this range.In the event that the intangible asset is disposed of or the rights expire in the period, amortization expenses can not be recorded in the taxable year.

DonationRegarding donations, in principle, they are not included in the amount of deductible expenses, but donations to charity and educational institutions approved by the government can be included in the amount of deductible expenses.

Credit losses and provisionsIn order to include credit losses as deductible, it is necessary to fulfill all four requirements below.① The bad loan amount has been eliminated from the claim amount② to conclude that it is reasonably unrecoverable③ tried to collect by reasonable procedures④ The credit loss amount is included in the previous year's income

In other words, merely recording it as an allowance for doubtful accounts can not be included in the amount of deductible expenses, it will be allowed to be included in the amount of deductible expenses only if the loan loss actually occurs and satisfies the four requirements.

R & D expensesR & D expenses spent for future profit earnings can be included in the amount of deductible expenses.However, even for research and development purposes, acquisition of depreciable assets and land can not be included in the amount of deductible expenses. Expenses related to the mining of natural deposits can not be included in the amount of deductible expenses.repair costsRepair expenses expended for repairing and improving depreciable assets used for profit earning purposes can be included in the amount of deductible expenses.However, up to 5% of the book value at the beginning of the tax year and 3% of the building can be included in the amount of deductible. The excess portion is recorded in the asset as capital expenditure and is included in the amount of deductible loss through depreciation.Other cost itemsItems other than those listed above, which are not included in the amount of deductible for tax purposes are as follows.

· Personal expenditure, living expenses (direct tax law Article 28)· Fine (direct tax law 31 Article)· Unfair expenses (direct tax law 32 Article)· Value added tax, corporate enterprise tax, personal income tax■ Tax rateThe tax amount is calculated by multiplying the taxable income amount by the tax rate stipulated by the type of the following corporation..jpg) * A listed company (communication company) will receive a refund of 10% of tax payment if you pay a dividend of 20% or more.According to the 2015 - 16 national budget proposal, the corporate tax has been changed as follows.

* A listed company (communication company) will receive a refund of 10% of tax payment if you pay a dividend of 20% or more.According to the 2015 - 16 national budget proposal, the corporate tax has been changed as follows..jpg) * For companies that are listed companies and have a dividend exceeding 30%, 24.75%, and those with a dividend below 10% will be subject to a tax rate of 35%.■ Minimum alternative taxThe corporation must pay 5,000 hu to the minimum alternative tax regardless of income or loss.■ Minimum transaction taxIf there are incomes of more than 5 million taka per year, the minimum transaction tax (Minimum Turnover Tax) is applied to the target company, 0.3% of the total income is applied. In addition, the tax rate for three years from the start of the project is applied at 0.1%.

* For companies that are listed companies and have a dividend exceeding 30%, 24.75%, and those with a dividend below 10% will be subject to a tax rate of 35%.■ Minimum alternative taxThe corporation must pay 5,000 hu to the minimum alternative tax regardless of income or loss.■ Minimum transaction taxIf there are incomes of more than 5 million taka per year, the minimum transaction tax (Minimum Turnover Tax) is applied to the target company, 0.3% of the total income is applied. In addition, the tax rate for three years from the start of the project is applied at 0.1%.

■ Declaration · Tax payment method① Tax returnAll corporations shall declare the corporation tax amount for the relevant taxing period to the competent tax office and pay tax on the deadline within 6 months from the last day of the taxing year or July 15 of the following year whichever is earlier not. In addition, it is necessary to attach an audited account settlement report to the final return form for all corporations.

② Intermediate declarationIf the income amount in the pre-tax year is over 300,000 taka and the income amount in the tax year is expected to exceed 400,000 taka, or if there is no declaration in the previous year and the income amount in the taxable year exceeds 400,00 taka If it is predicted, you have to file a tax return on quarterly basis.The tax amount in the interim declaration is calculated by dividing the tax amount of the previous year into four and deducting the tax amount paid in the corresponding fiscal year.Regarding the deadline for reporting, the taxable year of the corporation will be from July 1 to June 30 of the following year, so the first quarter is September 15, the second quarter is December 15, the third quarter is March 15 The fourth quarter will be until June 15..jpg) · Fiscal Year 2015June 15: Planned tax payment (1st time in 2015)July 15: Tax return for 2014September 15: Planned tax payment (2nd in 2015)Scheduled payment on 15th December (3rd in 2015)· FY 2016Scheduled payment on 15th March (4th time in 2015)Scheduled tax payment on June 15 (1st time in FY 2016)July 15: Tax return for 2015As a precaution, at the 2015 tax law amendment, a change was made to the provision of "Income Year (Fiscal Year)" in Article 2 35. As a result of this change, all companies other than the financial industry will be unified from July 1st to June 30th from 2016 onwards, and it was necessary to file a tax return as of the end of June .The accounting year so far could be freely set for each company by specifying it in the Articles of Incorporation, or by making a resolution at the foundation general meeting. In the articles of incorporation, if the fiscal year is specified in a period other than July 1 to June 30, it is necessary to change the articles of incorporation in accordance with this amendment. In the articles of incorporation, there is no specific provision, and if it is decided at the founding general meeting, it is necessary to adopt a resolution to change the fiscal year from July 1st to June 30th at the next annual general meeting.

· Fiscal Year 2015June 15: Planned tax payment (1st time in 2015)July 15: Tax return for 2014September 15: Planned tax payment (2nd in 2015)Scheduled payment on 15th December (3rd in 2015)· FY 2016Scheduled payment on 15th March (4th time in 2015)Scheduled tax payment on June 15 (1st time in FY 2016)July 15: Tax return for 2015As a precaution, at the 2015 tax law amendment, a change was made to the provision of "Income Year (Fiscal Year)" in Article 2 35. As a result of this change, all companies other than the financial industry will be unified from July 1st to June 30th from 2016 onwards, and it was necessary to file a tax return as of the end of June .The accounting year so far could be freely set for each company by specifying it in the Articles of Incorporation, or by making a resolution at the foundation general meeting. In the articles of incorporation, if the fiscal year is specified in a period other than July 1 to June 30, it is necessary to change the articles of incorporation in accordance with this amendment. In the articles of incorporation, there is no specific provision, and if it is decided at the founding general meeting, it is necessary to adopt a resolution to change the fiscal year from July 1st to June 30th at the next annual general meeting. -

Value-added tax

VAT (Value Added Tax) is a tax that is subject to the added value in Bangladesh and has the following characteristics.· It is an indirect tax imposed on the consumption of goods and services· Tax burden is the ultimate consumer· Intermediaries do not pay taxes, but they are obligated to pay taxesAs in the consumption tax in Japan, Bangladesh also sells goods and services, depending on the type of industry, but in principle 15% VAT is taxed.■ TaxpayerAlthough the burden on VAT is the final consumer, it is the business entities (VAT registered business operators) who provide sales of goods or services and the importers of goods, who are obligated to pay VAT, and individuals and corporations Any person whose annual sales exceed 2,000,000 ha is tax duty of 15% at normal rate.On the other hand, if the annual sales of the previous year is less than 2,000,000 taka, you have 4% tax liability.As a general rule, those who start the project will apply for a VAT registration application to the local tax office before the start of the project. If you do not register for this taxpayer, you need to be careful as you can not claim VAT tax credit or refund request.■ VAT exemption transactionsAll items and services are taxable goods and taxation services unless otherwise stipulated by law, but in Article 21 of the VAT method 2011, items and services classified as "tax-exempt" It is clearly stated.Examples of tax-exempt items· Supply or import of edible goods· Supply or import of pharmaceuticals· Supply of raw agricultural products and marine products· Sale of vacant lot· Land supply used for agriculture, horticulture, fishery industryExample of tax exemption service· Health, medical services· Educational services· Environmental pollution prevention activities· Publishing service· Library, museum, museum service· Zoo, botanical garden service■ Exemption from VATApart from tax-exempt transactions above, VAT exemption is permitted for the following goods and services (Article 20 of the VAT method 2011).Examples of duty-free goods· Goods to be exported· Leased goods used outside Bangladesh· Temporarily imported goods for repair, repair etc.· Goods used for international shippingExample of tax exemption service· Real estate services outside Bangladesh· Services offered outside Bangladesh· Intellectual property rights used outside Bangladesh· Inter-carrier communication service· Services related to international transport■ Calculation of payment tax amountIn the case where a Bangladesh company receives consideration for sale, service, etc. from a customer, when collecting the value added tax (output VAT) together with the consideration and paying the consideration for purchase · service etc., the value added tax Input VAT) will be paid.· Output VATThe output VAT is a tax that is taxed on the selling price of sales, service, etc. and is the sum of the amounts stated on the invoice. If the notation of VAT is an internal tax method, the amount obtained by deducting taxable sales from the total receipt will be the output VAT.· Input VATThe sum of the amounts stated in the tax invoice when paying the compensation for the transactions and services subject to taxation is the input VAT.Calculation methods are calculated by the following formula in the same way as Japan's consumption tax and other country's VAT.· Deduction method (invoice method)The deduction method is a method of paying the difference obtained by deducting the input VAT paid from the output VAT received every month.

Payment Tax Amount = Output VAT - Input VAT■ Tax rateThe applicable tax rate of VAT varies depending on the company's sales volume.If the annual sales for the previous fiscal year is over 2,000,000 taka, 15% is applied, and if it is less than 2,000,000 taka, 4% is the applicable tax rate..jpg) ■ Declaration / Payment ProcedureIf there is a VAT to be paid, VAT's tax payment obligor submits a tax return to the competent tax office stating necessary items in the form designated by the Revenue Agency including electronic filing by the 15th of every month, and pays taxes is needed.■ Tax invoiceIn calculating VAT value, tax invoice is very important. Basically, since the calculation of tax amount is done based on this tax invoice, tax regulations are established for its management etc.

■ Declaration / Payment ProcedureIf there is a VAT to be paid, VAT's tax payment obligor submits a tax return to the competent tax office stating necessary items in the form designated by the Revenue Agency including electronic filing by the 15th of every month, and pays taxes is needed.■ Tax invoiceIn calculating VAT value, tax invoice is very important. Basically, since the calculation of tax amount is done based on this tax invoice, tax regulations are established for its management etc. -

Tariff

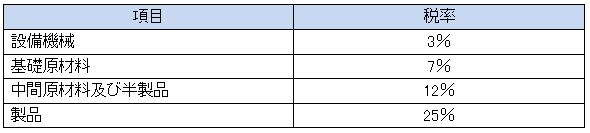

■ Types of tariffsIn Bangladesh, there are six types of import tariffs set by the Customs Law.■ Tax rateThe tariff rate is determined for each item according to HS code * classification.* HS code is a 6-digit code that was created for the purpose of unifying the names and classifications of international trade products globally as "Harmonized Commodity Description and Coding System" (a unified system for name and classification of products) The code number of that.■ General tariffsThe tax rate of general customs duty is classified into four largely for each item. 3% for equipment machinery, 7% for basic raw materials, 12% for intermediate raw materials and semifinished products, and 25% for products.In addition, high tariff rates different from usual are applied to some local industrial protection items..jpg) ■ Tax rateThe tariff rate is determined for each item according to HS code * classification.

■ Tax rateThe tariff rate is determined for each item according to HS code * classification.

* HS Code is a 6-digit code that was created for the purpose of unifying the names and classifications of international trade products globally as "Harmonized Commodity Description and Coding System" (a unified system for the name and classification of products) The code number of that.■ General tariffsThe tax rate of general customs duty is classified into four largely for each item. 3% for equipment machinery, 7% for basic raw materials, 12% for intermediate raw materials and semifinished products, and 25% for products.In addition, a tax rate of 1,000% to 7,000% is applied to some local industry protected items. ■Adjustment taxAdjustment tax is fixed at 5% uniformly, and specific items are not taxed.

■Adjustment taxAdjustment tax is fixed at 5% uniformly, and specific items are not taxed.

■Supplementary taxThe supplementary tax is set in the range of 20% to 350%, and the items subject to local industrial protection are high tax rates. Also, for certain items, tax is not imposed.

■ VATAs mentioned in the previous section, the applicable tax rate varies depending on the company's sales scale.If the annual turnover is 2,000,000 Taka or more, 15% is applied, and if it is less than 2,000,000 Taka, the applicable tax rate will be 4%. In addition, VAT is fixed at a uniform rate of 15%, and specific items are not taxed.

■ Prepaid Income TaxPrepaid income tax is fixed at 5% uniformly, and specific items are not taxed.

■ Prepaid trade VATPrepaid trade Value added tax is fixed at 3% uniformly, and specific items are not taxed.

■ Exempt itemsAccording to the Bangladesh Customs Law, goods imported and exported across the Bangladesh border are subject to import and export duties. However, the following goods etc. are not subject to tariffs.

· Capital equipment· Raw materials of medicines· Poultry medicines, food and equipment· Equipment for protecting the site (barbed wire, sandbag, corrugated iron plate, etc.)· Leather goods· Private generation facilities· Textile raw materials and equipment· Solar power generation equipmentRelief supplies· Goods for the blind and disabled· Imported goods by the embassy and the United Nations -

Other taxes

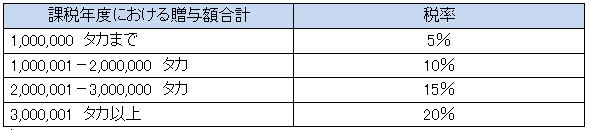

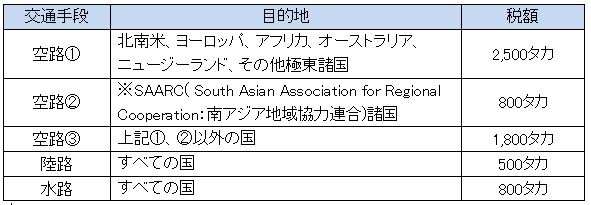

■ Gift taxGift tax refers to the tax that is incurred when you receive property from individuals, and tax payment obligations are incurred for those who received the gift.● Taxable itemsAs a general rule, gift tax is taxed on all the gifted assets, but from the viewpoint of the nature of the property and the purpose of giving gifts, gift tax is not imposed on the following property It is.Example of tax free property· Property gifted outside Bangladesh· Property gifted to government, local government· Property gifted to educational institutions, hospitals, disaster funds, charitable organizations and religious organizations operated or approved by the government· Assets gifted by wills· Gift of cause of death· Property gifted to parents, couples, brothers and sistersIn addition, if the total amount of gifted assets in the tax year is less than 50,000 taka, gift tax will not be taxed.● Calculation of tax amountCalculation of tax amount is calculated by multiplying taxable income amount by progressive tax rate stipulated by gift amount (direct tax law third schedule A). The duration of taxation of gift tax is from July 1 to June 30 of the following year, and the deadline of declaration and payment is until September 30. If declaration · tax payment deadline is delayed, 50% of gift tax amount must be additionally paid (direct tax law Article 119).■ Travel taxTravel tax is the tax imposed on traveling from Bangladesh to another country (Direct Tax Code Article 125 1), taxpayers must pay taxes to the Ministry of Finance to the extent that they do not exceed 10,000 taka not. Also, some of the following passengers will not be subject to a travel tax.· Children under 5 years old· Cancer patients· Visually Impaired· Disabled· Cabin crew on duty· Bangladesh diplomatic mission members and their families· UN staff and their families· Saudi Arabia visitors for pilgrimage to Mecca· Passengers who do not have a Bangladeshi visa, stayed in Bangladesh for the purpose of relaying to other countries, and whose staying time is 72 hours or less· Bangladesh domestic airline staff· Passengers using free tickets and air tickets issued at a special discount rate● Tax and PaymentThe amount of travel tax will vary depending on destination and transportation.

The duration of taxation of gift tax is from July 1 to June 30 of the following year, and the deadline of declaration and payment is until September 30. If declaration · tax payment deadline is delayed, 50% of gift tax amount must be additionally paid (direct tax law Article 119).■ Travel taxTravel tax is the tax imposed on traveling from Bangladesh to another country (Direct Tax Code Article 125 1), taxpayers must pay taxes to the Ministry of Finance to the extent that they do not exceed 10,000 taka not. Also, some of the following passengers will not be subject to a travel tax.· Children under 5 years old· Cancer patients· Visually Impaired· Disabled· Cabin crew on duty· Bangladesh diplomatic mission members and their families· UN staff and their families· Saudi Arabia visitors for pilgrimage to Mecca· Passengers who do not have a Bangladeshi visa, stayed in Bangladesh for the purpose of relaying to other countries, and whose staying time is 72 hours or less· Bangladesh domestic airline staff· Passengers using free tickets and air tickets issued at a special discount rate● Tax and PaymentThe amount of travel tax will vary depending on destination and transportation. ※Regional mechanism by 8 countries of India, Pakistan, Bangladesh, Sri Lanka, Nepal, Bhutan, Maldives, Afghanistan

※Regional mechanism by 8 countries of India, Pakistan, Bangladesh, Sri Lanka, Nepal, Bhutan, Maldives, Afghanistan

In addition, payment of travel taxes must be paid by the deadline designated by the Ministry of Finance. If you do not pay taxes by the deadline, you will be charged a delinquent tax of 2% per month against the delinquent tax amount.

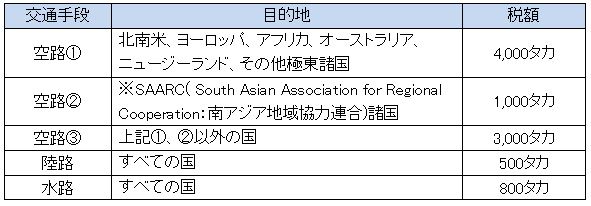

And as of July 1, 2014 tax amount has been changed as below. ■ Wealth taxWealth tax refers to the tax that is taxed on the net asset minus the total liabilities from the total assets and is taxed on all individuals with net assets. For this reason, tax returns for individual taxpayers include items to enter assets and liabilities, and the net asset value is calculated as the difference.Tax is calculated by multiplying the net asset value calculated using June 30 as the valuation date by the progressive tax rate prescribed by the following net asset value.

■ Wealth taxWealth tax refers to the tax that is taxed on the net asset minus the total liabilities from the total assets and is taxed on all individuals with net assets. For this reason, tax returns for individual taxpayers include items to enter assets and liabilities, and the net asset value is calculated as the difference.Tax is calculated by multiplying the net asset value calculated using June 30 as the valuation date by the progressive tax rate prescribed by the following net asset value. There is also provision that tax liability is exempted by prepayment of wealthy tax and if necessary, after payment is ready for payment, it will be collected.

There is also provision that tax liability is exempted by prepayment of wealthy tax and if necessary, after payment is ready for payment, it will be collected. -

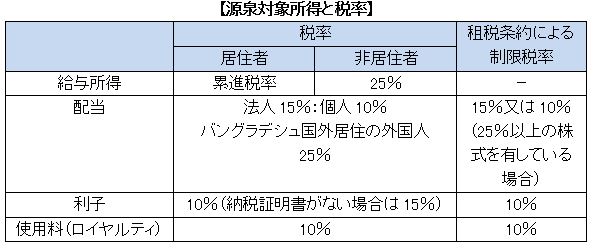

Withholding tax system

The withholding collection system is a system in which taxes to be paid by the recipient are collected at the time of payment and paid to the country instead when paying the consideration.The obligation to pay the withholding tax will be incurred by all companies including branches, liaison offices, banks and other financial institutions.In Bangladesh, income and tax rates subject to withholding tax are as follows. Since tax treaties are concluded between Japan and Bangladesh, tax rates prescribed in the Tax Treaty can be applied to items specified in the Convention by performing prescribed procedures. For taxes withheld, it is necessary to declare and pay taxes by 21 days after the payment date.If you do not collect withholding tax and do not do tax payment, attention is required because a 2% monthly tax will be raised against the withholding tax amount.

For taxes withheld, it is necessary to declare and pay taxes by 21 days after the payment date.If you do not collect withholding tax and do not do tax payment, attention is required because a 2% monthly tax will be raised against the withholding tax amount. -

Bangladesh DTA Treaty

I mentioned the summary of the tax treaty in the preceding paragraph, but here we will look at the details of some excerpted texts on the tax treaty signed between Japan and Bangladesh.■ Definition of PE (Article 5 of the Bangladesh Duty Treaty)In Article 5 of the Bangladesh DTA, the definition of permanent establishment (PE: Permanent Establishment) is stipulated and it is defined as the office, branch, office, warehouse for storage management, period over 6 months The place where it exists (construction PE) etc is stipulated as PE.However, in the case of using the facility only for the storage or exhibition of goods or goods belonging to a Japanese company in Bangladesh, cases where the facility is held only for exhibition, or it is held only for processing by another company , If you are doing business in Bangladesh through an agent such as an intermediary who has an independent position from a Japanese company, a wholesaler or other agent, the fact that it is not a PE is merely stated in the tax convention as just the fact that it is a controlling relationship.When doing business in Bangladesh, it is necessary to pay attention to the content of activities so that it does not fall under this tax treaty PE.■ Special affiliated companies (Article 9 of the Bangladesh Duty Treaty)The details relating to transfer pricing taxation are prescribed by Ministry of Finance Ordinance, but it is also prescribed in the Japan Bangladesh Dexax Treaty.As a content, if a company or the same person of one Contracting Party is directly or indirectly participating in the business management, control or capital of another Contracting Party, the terms of the transaction are When it is different from the terms and conditions, if one does not have such a condition, one of the Contracting Parties will tax the profit which the enterprise etc of one Contracting State would originally obtain, and in summary "Relation If you do business between companies, you must follow the terms of the third party transactions "is stated.Regarding the mutual consultation after transfer pricing taxation in paragraph 2, if there is agreement between competent authorities of the two countries, it states that appropriate adjustment will be made for the tax amount which was taxed.■ Taxation on usage fees (royalties etc.) (Article 12 of the Bangladesh DTA)In Japan and Bangladesh there are cases where royalties are collected as consideration for providing know-how etc.For this use fee, in the tax treaty it is said that "you can tax in the country where the fee was generated". In other words, if royalties are paid from Japan to Bangladesh through the provision of technology from Japan, tax will be levied by withholding at the time of payment.In the tax treaty, the withholding tax rate is considered not to exceed 10% of the usage fee, so withholding tax will be done at the time of payment within that range.In addition, the seventh section has a statement concerning the transfer pricing taxation, and for the transactions between affiliated companies, tax rates under the tax treaty are not applied for parts beyond third-party prices and are subject to regular tax rates It will be.■ Personnel service income for short-term residents (Article 15 of the Bangladesh Duty Treaty)In the tax treaty, it is stated that salary income is taxed only in the country where actual work is being carried out. In other words, if work that is the source of salary is not done, taxation will not be applied to salary income in that country, and tax will be imposed on the actual work place.When traveling from Japan to Bangladesh, if you fulfill the following three requirements, you will not be taxed on the Bangladesh side for the remuneration or salary paid (short-term stay exemption).· Based on the number of days stayedThe number of days stayed in the taxable year shall not exceed 183 days· Salary Payment Area StandardsRemuneration or salary paid at Japan side· Salary burden criteriaRemuneration or salary is negative in PE etc. in BangladeshWhat is not carried outTherefore, even if the number of stay days is short, salaries will be paid in Bangladesh, or if Bangladesh will bear that salary, this provision will not apply.As an exception, the income earned by international travel, private acting by actors, musicians, entertainers and athletes in Bangladesh is taxed on the side of Bangladesh.■ Tax on executive remuneration (Article 16 of the Bangladesh Duty Treaty)With regard to salary etc., in principle, tax is not taxed if work is not done in that country in principle. In other words, if employees are dispatched from Japan to Bangladesh, taxation will not occur in Japan unless work is done in Japan.However, if the officer of the Japanese corporation resides as a resident in Bangladesh, if the Japanese company earns compensation as an officer, if the Japanese side is a non-resident and the domestic work Even if there is nothing, attention is required because taxation is done on the Japanese side.On the contrary, for those who are officers at Bangladeshi corporation, even if you are a resident of Japan, if salary is incurred in Bangladesh, you will be taxed in Bangladesh.In other words, if you receive remuneration as an officer, there is no application of the short-term stay duty exemption under Article 15 of the preceding Article, and tax will be levied in the local country regardless of living qualities.■ Elimination of double taxation (Article 23 of the Bangladesh Duty Treaty)Regarding the method of double taxation exclusion between bilateral countries in both Bangladesh and Japan, the clause states that. Each allows the deduction from the amount of tax to be paid in each country to the extent of the tax amount calculated based on the tax laws of each country.In addition, if a Japanese company reduces or exempts taxes from dividends, royalties, and interest from Bangladesh, the amount of tax that was deducted is regarded as the tax amount paid by Bangladesh and a foreign tax credit is deducted You can do it.■ Bilateral talks on double taxation (Article 25 of the Bangladesh Duty Treaty)In accordance with the tax laws of either Japan or Bangladesh, if you receive a tax that does not comply with the provisions of this tax treaty, you can file a complaint against an authorized authority in your country of residence.In this case, the competent authorities of both countries will keep in touch with each other and hold mutual consultation with each other to eliminate taxation that does not conform to the provision of this tax treaty.In cases where this provision is not stipulated in the tax treaty or in countries where a tax treaty has not been concluded with Bangladesh, tax will be imposed based on the tax law stipulated in their respective countries.

-

.jpg)