Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaJapan

2 Chapter Tax

-

-

1 Chapter Accounting

2 Chapter Tax

2.1 Overview of Japanese corporate tax system for investment in Japan

2.3 Outline of corporate income taxation

2.4 Outline of Withholding Income Tax

2.6 Summary of consumption tax

2.7 Outline of a personal tax system

2.9 Other significant corporate taxation related to international transactions

2.10 Main treatment of corporate tax · local tax · consumption tax due to large/small capital amount

3 Chapter Labor

-

-

-

■ Neutrality of tax system against a form of advancement (branch office or local corporation)

A corporation that conducts economic activities in Japan is taxed in Japan regarding the profits arising from its economic activity. However, when multinational companies perform commercial operations in Japan, measures are taken to prevent the tax system from becoming unfair depending on the type of entry. For corporations established in Japan, an income of the Japanese corporation is subject to taxation regardless of the income generation place (income source area) in principle except for individual income, which is not taxable or tax-exempt. In that case, if profits earned in a foreign country are included and taxation is made in the source country of income about that profit, in order to eliminate the double taxation in income source country and Japan, there is a provision for a foreign tax deduction that deducts tax imposed in foreign nations from Japanese tax. Meanwhile, measures are taken to prevent double taxation internationally in Japan, for example, Japanese branches of foreign corporations are subject to the imposition of individual income only in Japan.As for the scope of income to be taxed by the Japanese branch of a foreign corporation, a substantial change has been made from the fiscal year beginning on or after April 1st, 2016, the Japanese branch office and the head office, etc., are regarded as separate independent corporations. As a result, the taxable income of the Japanese branch is the income attributable to the Japanese branch (permanent establishment) (the income obtained when the Japanese branch is assumed to be a company separated or independent from the head office, etc.,) and other fixed-income. In the calculation of income attributable to the Japanese branch (permanent establishment), the internal transactions between the branch office and the head office, etc., are deemed to be traded on an inter-company price basis, and the profit and loss of the inter-company transaction are recognized. In accordance with the change in the scope of income, which is subject to taxation of the Japanese branch (permanent establishment), the foreign tax credit provision is newly established for foreign corporations, and the Japanese office (permanent establishment) earns it in a third country in the case of income attributable to a Japanese branch (permanent establishment) that has been taxed in a third country, a foreign tax credit deducting the tax imposed in a third country from the Japanese tax to a certain extent, international we exclude double taxation. -

■ Tax withholding or declaration payment

When a foreign company conducts business activities in Japan and gets a specific income in Japan, according to a particular method depending on the form of the enterprise and the type of income, tax amount by procedures of tax withholding or declaration at the time of payment will be calculated, and tax payment will be made.

-

-

-

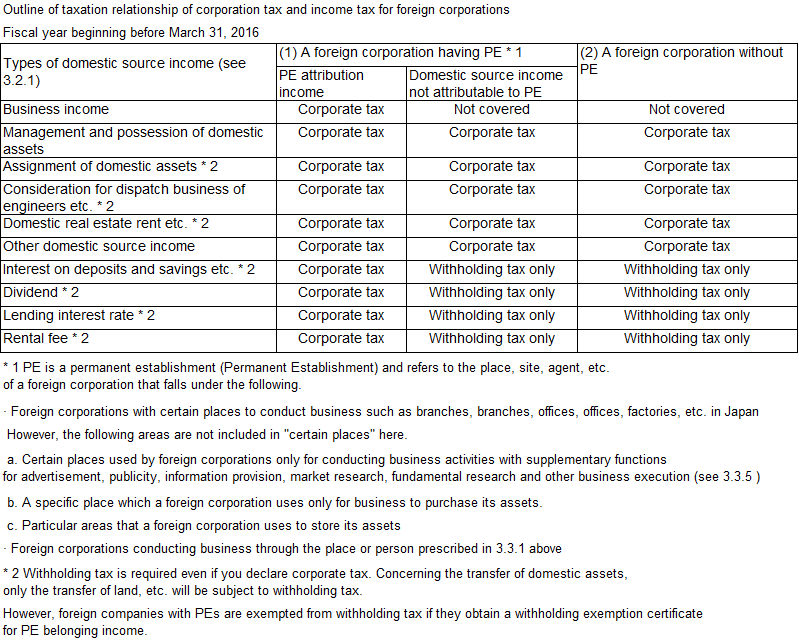

■ Domestic source income

The primary domestic source incomes are as follows. The specific taxable scope depends on the type of activity of the foreign corporation in Japan. (Described later)1. Permanent facility attribution income2. Income from operation/possession of assets in Japan3. Income from transfer of domestic assets4. Consideration for dispatch business of engineers etc.5. Lease fee etc. for local real estate etc.6. Other domestic source income

-

-

-

■ Establishment of a Japanese corporation, the establishment of a Japanese branch, etc., and notification to the tax office

In the case of newly establishing a Japanese corporation under the laws of Japan, when opening a branch etc., in other specific circumstances, after the establishment or establishment thereof, within the specified time limit the documents to be filed concerning the establishment or establishment you must submit it to your local tax office. The handling when a foreign corporation opens a branch office etc. is as follows.· Establishment of Japanese branch etc., of a foreign corporation and notification to a tax office

When opening a new branch office in Japan, after opening it, you must submit the notification documents for the establishment to the local tax office within a specified time limit. Also, even if a foreign corporation does not have a branch office or the like, it will result in a guaranteed income, which is subject to corporate tax taxation in the country, it is necessary to submit the written document to the tax office in charge. -

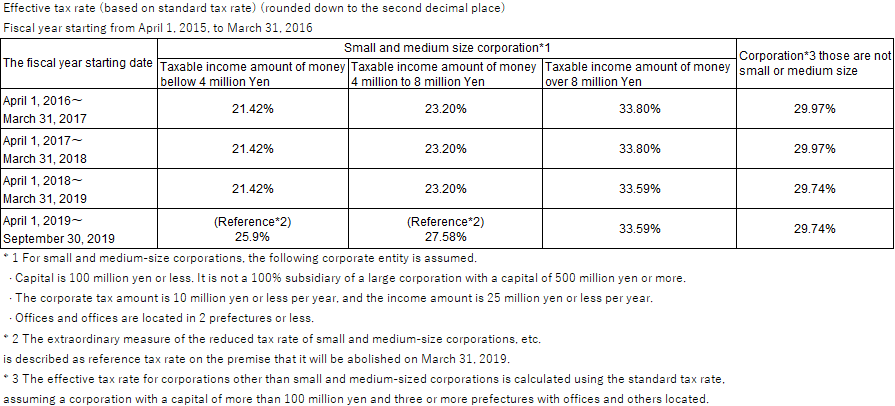

■ Corporate Income Taxation and Tax Rate

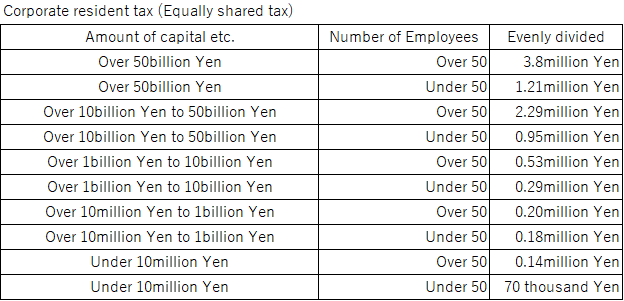

The income arising from corporate business activities, taxed in Japan, is classified into two major categories, national tax, and local tax. There are corporate tax, local corporation tax, domestic corporation special tax on local tax, and the local fee includes corporate resident tax and business tax (collectively referred to as "corporate tax, etc."). Calculation of taxable income and taxable income of corporate inhabitant tax, enterprise tax (including local corporation special tax, after this the same) will be subject to corporate tax handling with certain exceptions.Corporate inhabitant tax consists of corporate tax expense and equally divided two. The corporate tax rate is calculated based on the corporate tax amount, and the equivalent amount is determined based on the amount of capital and the number of employees. An equal division has no income, and it is characterized by payment obligation even if there is no corporate tax or resident tax.

Regarding business tax, when the amount of stated capital at the end of the business year of the corporation is over 100 million yen, the standard external taxation will be applied.Taxation on income These income taxes, etc. shall be the taxable income calculated for each business year of the company. In addition to this, there is a corporate tax for retirement pension fund reserve fund (no corporate tax is imposed for the fiscal year commencing on March 31, 2020).The tax rates for corporate tax, corporate inhabitant tax and enterprise tax for income in each business year are as follows. As for the local tax, the tax scale is slightly different depending on the size of the business and the local government in which it is located, so please check the tax rate of each local government.

-

■ External form standard taxation of business tax

For corporations whose capital or investment amount exceeds 100 million yen at the end of the fiscal year, standard external imposition is carried out based on the amount of income, added value, and capital. The standard tax rates for income divided, value-added and money related to each amount are as follows.

-

■ The scope of corporate taxable income

Regarding corporations established in Japan, regardless of the place of revenue generated by the business activities, their income will be subject to taxation in Japan. On the other hand, regarding taxation of foreign corporations, depending on the start date of the business year of the corporation, it is classified into PEs in the following table, and each of the aforementioned domestic source income is determined according to the classification Income tax is imposed in Japan on income. However, corporate inhabitant tax and business tax are not imposed on foreign corporations that do not have PE in the table.

-

■ Income from Representative Office

A foreign corporation that conducts activities in Japan through a representative office or the like, and the office, etc. acts as an advertisement, advertisement, information provision, market research, fundamental research, and acts that have supplementary functions for the execution of the project Only when doing so, it is said that income that is subject to corporate taxation will not arise from that action. However, please keep in mind that tax payment risk occurs when income appears by doing business related to the business of a foreign corporation besides ancillary functions as a representative office. -

■Calculation of corporate taxable income

The amount of income, which is the taxable standard such as corporation tax for rent in each business year, is calculated by performing necessary tax adjustments to corporate income computed by accounting standards generally accepted as fair and reasonable. Except for the exceptional treatment shown below, the number of costs, expenses, and losses incurred to earn revenue can be deducted from taxable income.In the case of a foreign corporation, there are no restrictions on costs, expenses and losses to be deducted in the calculation of taxable domestic source income in Japan. However, in the case of deducting costs, fees, and losses generated outside the country in calculating local income, it is necessary to prepare the statement and evidence.

Specific items with restrictions on cost, expense, loss deduction· Corporate taxes and penalties· Deductible excess deductible limit· Excess allowable limit of entertainment expenses· Provision of various provisions· Amortization limit exceeding the number of depreciable assets and deferred assets· Assets write down· Executive salaries, officers retirement fees -

■ Taxation of retained earnings of specified family companies

Regarding certain corporations among Japanese corporations that are family companies, there is an application of retained tax in addition to corporate income for ordinary income.Even if income arises in a company, retained taxation can cause profits to be kept in the company more than necessary without paying dividends. The tax burden of individuals and corporations depends on whether it is a specific family company or not. Therefore, in order to balance the tax burden, in the case that a particular family company holds profits within the company exceeding the allowable amount in each business year, the corporate tax based on the individual tax rate is changed to the regular corporate tax for the retained earnings It is a system which is taxed by adding.

Calculated by multiplying taxable retained amount calculated by deducting retained deduction amount from the retained amount in each business year by the individual tax rate. Depending on the amount of income, the different tax rate is 10% for the amount less than 30 million yen a year, 15% for the amount less than 100 million yen/year, more than 100 million yen/year It is 20% against it. -

■ Handling of deficit

The amount of loss arising from the calculation of income for each business year is carried forward for nine years after that (10 years for losses incurred in the fiscal year beginning on or after April 1, 2018). This carry-forward system is applicable only when submitting a blue declaration in the business year in which the deficiency occurred and submitting a final return form from that onwards. If the capital of the corporation at the end of the fiscal year exceeds 100 million yen, or if it is a wholly-owned subsidiary of a large corporation (including foreign corporation) with capital of 500 million yen or more, the deficit that can be deducted from income The amount of money can be inferred to the extent of the income amount below the limit by the start business year of the corporation.

For certain corporations, such as small and medium corporations that submit a blue declaration, the deficit shall be reversed in the fiscal year that began within one year prior to the start of the business year in which the debt was incurred, and the business year It is also permitted to receive refund of all or part of the corporate tax amount of. However, for unlisted corporations, corporations, etc. being rebuilt, the reduction ratio is set to 100% for a specified period.

However, for unlisted corporations, corporations, etc. being rebuilt, the reduction ratio is set to 100% for a specified period. -

■ Organization restructuring tax system

When a corporation relocates an asset by reorganization such as division, merger, in-kind investment, etc., in principle the transaction is carried out at the market price, so the tax on the transfer of the transfer assets is taxed.On the other hand, for the following three cases, it will be a qualified organization reorganization.

· Constitutional restructuring between corporations in direct or indirect holding relationship with holding the ratio of 100%· A certain amount of corporate restructuring between corporations with a direct or indirect holding relationship of more than 50%· Organization restructuring that meets specific requirements as organization restructuring for a joint projectWhen it falls under qualified organization restructuring, measures are taken to defer the tax on profit/loss of the transfer by carrying out the book value of the relocated asset. -

■ Tax return and payment

1. Tax return and paymentWithin two months from the day after the end of each business year, the corporation shall submit a tax return on corporation tax, local corporate tax, corporate resident tax, enterprise tax, domestic corporation special tax, and consumption tax on that income, payment You must pay the amount. However, the final return cannot be submitted because the settlement of accounts will not be finalized due to circumstances where the ordinary general meeting of shareholders will not be convened within two months due to the provision of the articles of incorporation, etc. or exceptional circumstances of the corporation, etc. and other unavoidable reasons in cases, you can ask the extension of the deadline by approval of the director of the tax office. However, this extension is only for submitting the corporation tax, local corporate tax, corporate resident tax, business tax, local tax return declaration, and payment must be made within two months. There is no system to extend the deadline for the consumption tax, so you must submit and pay the declaration within two months. The amount of income, tax amount, etc. stated in this final return form must be calculated based on the settlement determined by the resolution of the general meeting of shareholders.

In the calculation of the fixed tax amount to be paid, if there is an interim payment amount paid in advance, it is deducted.2. Intermediate declaration and paymentFor a corporation whose business year exceeds six months, an interim tax return shall be submitted within two months from the date on which the first six months have elapsed, for the period up to the date six months have passed since the commencement of the business year, Payment amount must be paid (unless the tax calculated by the prescribed formula is less than a certain amount). On the other hand, it is necessary to pay the consumption tax separately in three patterns of January intermediate declaration, mid-March declaration, and June mid declaration according to the tax payment amount of the previous year.3. Blue returnCorporate tax returns are distinguished between blue declaration form and white return form. For corporation tax return, we apply, we approve by the tax office and submit blue declaration form. Various tax benefits are granted to corporations that provide the blue declaration.To obtain the tax office's approval for it to file a blue tax return must be submitted to the tax office a proposal for approval by a specific format to a date before the date of the start of the fiscal year. For a foreign corporation was supposed to provide a branch of the newly established corporations and recently in Japan, in the case of the fiscal year of its establishment (installation) was the day seeking the application of blue declaration, it established the (facility) It is necessary to submit a form for approval by the day before 3 months after the establishment (establishment) or the day of the end of the first business year, whichever is earlier, but the blue declaration is more advantageous In most cases, therefore, we will submit the application form at the time of establishment. -

■ Remittance to home country

Remittance to the home country parent company carried out by the Japanese subsidiary in Japan is made as a transaction between businesses and is generally treated as a payment of cost, expenses, distribution of profits, or loan (or repayment of loans), etc. Specific cost and expenses are deducted for income calculation by Japanese corporation as the payer. For income (e.g., interest, dividend, royalties, etc.) of the parent company, there is the case that withholding tax withholding income tax is required at the time of payment. About withholding income tax, if you have a tax treaty with Japan, the withholding tax rate may be reduced, or tax exempted in some cases, and it is necessary to submit a prescribed letter of written notification.

On the other hand, regarding the remittance made to the head office (home country) by a branch of a foreign corporation, we regard the intercompany profit and loss as a branch office from the head office. From the head office to the branch office, there will be no profit and loss as it applies to the capital transaction, etc. regarding the provision of branch office funds and the remittance from the branch to the head office, etc. There is no tax on income tax withholding tax for internal transactions.

-

-

-

Outline of Withholding Income Tax

The income tax system adopts a "tax return system" that the taxpayer himself calculates the income amount of the year and the tax amount for it, and voluntarily declares and pays these taxes. In addition to this tax payment system, we also adopt a withholding system whereby payer collects income tax and spends it when paying income for a specific profit. Withholding tax will be levied and paid in case of payment of particular salary which is subject to taxation regardless of individuals or corporations. The income covered by the withholding system is determined according to the type of income and the category of recipients of that income. -

■Tax withholding and payment procedure

Those who pay income to be withheld must pay the withholding tax amount to the tax office by the 10th day of the month following the month of payment. Provided, however, that if the payer has an address or business office in Japan and the payment is made to a non-resident or a foreign corporation abroad, the withholding income tax shall be paid by the end of the month following the month of payment I will pay. Concerning withholding income tax such as salary paid to residents, only for small businesses with less than ten persons to be paid, from January to July by July 10, from July 12 Special provisions are allowed to withhold the monthly amount by January 20 and half a year to collect withholding income tax. -

■ Tax withholding for residents (individuals)

The following other certain payments made in Japan to residents are subject to withholding tax.· Interest· Dividend· Salaries, wages, bonuses and other similar remuneration· Retirement allowance· Remuneration, fee, etc. for sure experts -

■ Withholding tax for domestic corporations

The next payment made domestically to the domestic corporation will be subject to withholding tax.

· Interest· Dividend -

■ Tax withholding for nonresidents and foreign corporations

In cases where compensation for dispatch work of engineers etc. lease of domestic real estate, etc. is paid to nonresident or alien corporation, payment is made in the country or even when it is paid abroad If a person has an address, business office, etc. in the country, those who make payment must withhold withholding. With regard to certain income specified in accordance with the classification of nonresident and foreign corporation, in the case where a nonresident or a foreign corporation who is a recipient of income has a permanent establishment in the country, its revenue is Withholding tax is exempted on the condition that it is attributed to the permanent establishment, and it is combined with the business income and presented to the payer with the certificate of the tax office to the effect that it is subject to tax return.

-

-

-

Tax Treaty

To avoid international double taxation, Japan has concluded a tax treaty with many countries with the aim of adjusting the range of income that can be taxed for bilateral investment and economic activities.The provision of the tax treaty will be applied over domestic law. Concerning the taxation of Japan to individuals or corporations who are resident of the treaty partner country, income source sites of various incomes set as taxable income under domestic law following the tax treaty (Definition provision concerning the place of occurrence of income on which taxation is based) may be corrected. There is also a provision for reduction and exemption of taxes in Japan which is the source of income for many incomes.

-

-

-

Overview of consumption tax

For domestic and import transactions, a consumption tax is imposed except for tax-exempt transactions and limited listed transactions. The consumption tax rate is 8% (including local consumption tax 1.7%).1. Domestic transactions: Transfer and lending of assets carried out by a business operator in business in the local market, and provision of services2. Import Transaction: A foreign cargo was taken from a bonded area, this international cargo is defined in Article 2, Paragraph 1, Item 3 of the Customs Law.Foreign cargo is not limited to those stated in domestic transactions in 1 above, and it is subject to taxation even if it is free of charge or what is not done as a business (private import).Transactions of financial transactions, capital transactions, postage stamps, stamps, stamps, stamps, etc., disabled persons articles, educational books are exempt from tax.Certain export transactions such as export transactions, international communication, international transportation, etc. for providing services to nonresidents are exempt from consumption tax subject to export certificate.(Note) From October 1, 2019, the consumption tax rate will be raised to 10% (including local consumption tax 2.2%). At the same time, the consumption tax reduction tax rate system was implemented to reduce the consumption of drinks and meals excluding alcoholic beverages and to eat out and the newspaper issued more than once a week (based on the subscription agreement) reduced tax rate 8% (local consumption tax Including 1.76%) will be applied. -

■ The duty-free business operator system

For taxpayers whose taxable sales in the reference period (Note 1) is 10 million yen or less (Note 2), the consumption tax obligation is exempted. Businesses exempted from this tax obligation are called "tax-exempt businesses." Even tax-exempt companies can be taxable businesses by submitting a notification form in advance. As tax-exempt companies are exempt from a consumption tax, it is not only that they have not received sales tax on sales, but also because they are not paying consumption tax on purchase tax on the purchase, In the calculation, we cannot apply the purchase tax deduction. At the beginning of the project, there may be cases where upfront investment, such as fixed assets and inventory assets, is higher than sales due to business activities. Therefore, in such a case, it is important not to the tax-exempt business operator, but to make a notification, become a taxable business, and apply for a refund of consumption tax.A newly established corporation with a capital of 10 million yen or more, a corporation organized with 50% or more investment by a group with taxable sales of more than 500 million yen among newly created corporations with capital less than 10 million yen (in either case Taxation obligation is not exempted for businesses and others whose taxable sales etc. (Note 3) in the previous year or the first half of the last fiscal year exceed 3 million yen.

(Note 1) A corporation whose period of one year from the previous business year is the reference period for the last year business. For a corporation whose period of the last year business is less than one year, a period combined with each business year that started between the day before two years before the start of the business year and the day after one day after that date.(Note 2) For a corporation whose reference period is not one year, determine the taxable sales in the reference period converted to one year's worth.(Note 3) It can be judged by the amount of payment salary instead of taxable sales. -

■ Purchase tax credit

In calculating the consumption tax amount to be paid, calculate it by deducting the consumption tax amount on taxable purchase from the consumption tax amount on taxable sales (purchase tax credit deduction). Taxable procurement refers to buying assets or providing services from others to do business. There are items related to all costs, expenses, and losses in the purchase, but not all transactions will be a taxable purchase, but those to be taxed and those not subject to consumption tax (non-taxable transactions, tax-free transactions) Since there is a trade, these classifications become necessary at the time of trading. Regarding certain e-commerce transactions that have been provided across the border from overseas operators in deals with offshore business operators, about operations that are subject to the application of the reverse charge method or transactions that were provided by non-registered business operators Only purchase tax deduction is allowed. Since the purchase deductible tax amount differs depending on the taxable sales ratio (taxable sales / total sales), etc., not all of the consumption tax paid will not be deducted.Also, to receive the purchase tax credit, it is necessary to save books and invoices that describe certain matters.

For small and medium-sized enterprises whose taxable sales in the reference period is 50 million yen or less, by submitting a notification form in advance, it is calculated by multiplying the consumption tax amount on taxable sales by a fixed ratio prescribed for each industry type You can consider the amount as a purchase deduction tax amount and make a purchase tax deduction. This system is called "simple taxation system."(Note) From the implementation of the reduced tax rate system for four years (from October 1, 2019 to September 30, 2023), in order to receive purchase tax credits, books that describe items necessary for segmental accounting and It is required to save invoices and the like described in the classification (preservation method such as invoice stated statement). Also, from October 1, 2023, instead of preservation of classification written invoices, etc., it is necessary to save eligible invoices issued by the taxpayer who registered with the director of the tax office (Eligible Invoice Equal storage method (so-called invoice system)).

-

-

-

Outline of Individual Tax System

All individuals are categorized as resident or non-resident regardless of nationality. Income tax on individuals is taxed on personal income during the calendar year. -

■ Habitation concept and taxable income

1. ResidentsPersons who have an address (Note 1) in Japan, those who have resided in Japan for more than one year are referred to as residents (Note 2). For residents, income tax is levied on global income regardless of the source of income.

(Note 1) In 1, "address" refers to the home of the life. A place of residence refers to a place that continues to live for a considerable period but does not reach the level of the house of daily life.(Note 2) Residents are categorized as permanent residents and non-permanent residents. Those residents who are not citizens of Japan in Japan and who have an address or residence in Japan for a period of not more than five years within the past ten years shall be non-permanent residents. The taxable scope of a non-permanent resident is the same as the taxable range of residents, but foreign source income is not taxed in Japan unless payment is made in Japan or remittance from Japan to outside Japan. However, even payments paid outside of the country fall under domestic source income which is paid based on Japanese duty, and income tax is taxed together with wages paid in Japan.2. Non-residentThose who are not residents are called nonresidents. As for nonresidents, income tax is imposed only on Japanese domestic source income in Japan. About the scope of withholding tax withholding income tax for nonresidents, it is stipulated for local source income, and taxation will be completed only by withholding tax, except in some instances.

-

■ Declaration Income Tax

1. Declaration of Income Tax to ResidentsThe income amount for one year is calculated by the method prescribed for each category of income. We deduct various income deductions from the total amount of income and multiply taxable income after deduction by the progressive tax rate to calculate tax amount. If there is a withholding tax imposed on income beforehand such as interest income from the tax amount after calculation, we will calculate payment amount by deducting the withholding tax amount.

2. Declaration of income tax for nonresidentsNonresidents are classified into the following three according to their mode.⑴ Non-resident having offices in Japan⑵ Through a non-resident or a specific agent who continues construction in Japan etc. for one year or moreNon-resident who does business⑶ Other nonresidentsTaxable income is calculated for rent determined for each of the above categories.Regarding taxation methods for nonresidents, income taxes after 2017 are taxed separately for income attributable to permanent establishment and other domestic source income according to the presence or absence of permanent establishment. In principle, the declared income tax amount imposed on nonresidents is calculated in the same way as for residents, but there are differences in the handling such as applicable income deductions and limitations on foreign tax deductions.Care must be exercised about salary income related to labor consideration provided in Japan. Because salaries are paid abroad, we cannot withhold the salary income in Japan, so nonresidents who receive payment must declare and pay the tax amount of 20.42% of their total salary, etc.3. Individual's tax income tax rate (in the case of residents and total taxation of non-residents) is as shown in the table below. 4. For salary income, calculate the income tax amount based on the amount deducted from the income amount by the salary income deduction in the following table.

4. For salary income, calculate the income tax amount based on the amount deducted from the income amount by the salary income deduction in the following table.

-

■ Withholding income tax

Withholding income tax for residents and nonresidents is as described above. -

■ Declaration / Payment

Residents shall submit a final return form for each year of the calendar year for income of that year from February 16th to March 15th of the following year, unless the taxation procedure is completed by withholding You must pay the tax amount. Provided, however, that if the total income amount does not exceed the total amount of income deductions, or when payment is paid for payment subject to withholding (year-end adjustment) from one payment destination, for those salary incomes is less than 20 million Yen for that year and other income is 200,000 yen or less, in principle there is no need to declare.

Regarding payment declaration by nonresidents, in principle, it is done according to the provision of income calculation of residents. Nonresidents who have not been declared or paid by the time of leaving the country and who have not submitted notification concerning the designation of the taxpayer administrator to the director of the tax office among the nonresidents who are obliged to pay tax are required to return the final return. We have to submit charge and pay the fee. -

■ Reconstruction Special Income Tax

Individuals and corporations are subject to a reconstruction special income tax of 2.1% against the amount of income tax from January 1, 2013, to December 31, 2037. For withholding taxes, we also collect 2.1% of reconstruction special income tax on the amount of withholding income tax.

If the withholding income tax rate specified in the domestic law is reduced or exempted under the provisions of the tax treaty, no special reconstruction income tax is imposed. -

■ Individual Inhabitant Tax · Individual Business Tax

There are two types of personal resident tax: a prefectural tax on own income and municipal tax on a municipality, and it is imposed on those who have an address, etc. in Japan as of January 1 every year. Personal inhabitant tax consists of income allocation and equally divided amount (fixed amount) etc. Income division is taxed on the income of the previous year and the calculation of the taxable income is calculated according to the provision of income tax calculation except that there are special provisions. Individual inhabitant tax must be declared by March 15, but when submitting a tax return on income tax declaration of personal inhabitant tax is unnecessary. The standard tax rate of personal resident tax (income dividend) is as follows.

· The standard tax rate for equality is 1,000 yen for prefectural taxes and 3,000 yen for city municipalities, but for the ten years from FY 2014 to 2023, they are 1,500 yen and 3,500 yen respectively.

· Because local governments may have a different tax rate than the standard tax rate, attention is required.

Individuals conducting specific projects specified by local tax laws are required to pay business tax. In principle, the taxable income of business tax is calculated according to the provision of income tax calculation. March 15 and payment shall make the declaration will be made in August and November by the tax notice issued by the prefecture.

Tax rates for individual business taxes are determined for each type of business and range from 3% to 5%. -

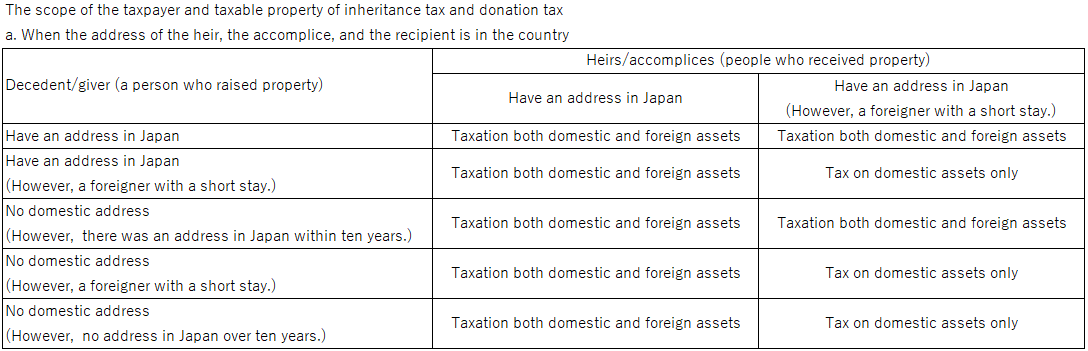

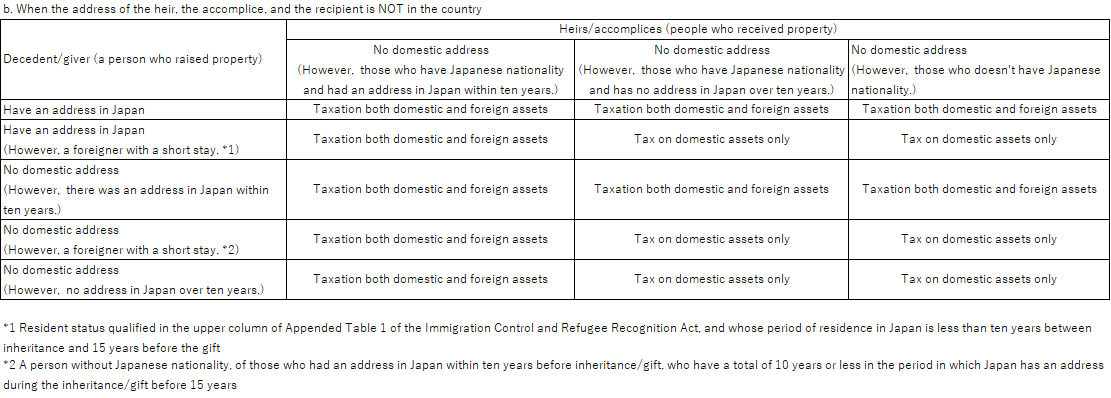

■Inheritance Tax and Gift Tax

1. The scope of the taxpayer and taxable property

Below, we denote the decedent/giver as "person who raised property," heirs/accomplices and recipients as "those who gained property."2. When the representative in Japan has inherited or accepted property by inheritance/giftIn the case that a person having an address in Japan at the time of inheritance/gift gives assets, regardless of the nationality of the heirs/recipients, the person who got the property becomes the tax liability person of the inheritance tax/gift tax. Inheritance tax and gift tax will be covered not only for the feature in Japan but also for property outside the country. Therefore, even if foreigners acquire assets located outside of Japan due to inheritance etc. from families residing in their home country while staying in Japan, they will be subject to inheritance tax/gift tax in Japan, so be careful is. However, in the case of a short-term stay, the fee will be applied only to Japanese domestic property.3. When the resident in Japan becomes a decedent or a recipient in JapanEven if a foreign resident who is an heir to a foreign resident living in Japan has acquired property by inheritance etc., the address of the person who raised the capital when he/she got the property is in Japan, tax will be imposed on all property acquired regardless of the nationality of the person who got the property. In other words, we will be subject to inheritance tax and donation tax not only for the feature in Japan but also for property outside the country. Even if a foreign resident is living in Japan and died due to an unexpected accident or the like, even if the family inheriting property etc. lives in the home country, it is subject to Japanese inheritance tax, so be careful. However, if a foreign expatriate is a short-term stay, it will be taxed only on domestic property.4. When the expatriate in Japan has left the country after completing the duty periodIf neither the decedent, donor, heir or recipient has an address in Japan, it will be subject to inheritance tax/gift tax only for property in Japan. However, if the person who got the property has Japanese nationality, either the decedent/ giver/heir/ heir/giver should have the address in Japan within 10 years before inheritance/gift When there is a thing, caution is necessary because it will be subject to inheritance tax and donation tax not only for the property in Japan but also for property outside the country.5. Inheritance tax · Gift tax rateBoth inheritance tax and gift tax are taxed at a tax rate of 10% to 55%, but the inheritance tax and donation tax differ in taxable price to which each tax rate applies.6. Foreign tax creditIf inheritance or gift gives a person who gets property outside Japan, a tax equivalent to inheritance tax/gift tax is imposed on the international capital in the country where the foreign ownership is located (For gifts, Including cases imposed), double taxation will be adjusted according to the provision of foreign tax credit which deducts tax imposed on foreign countries from a certain extent from Japanese inheritance tax/gift tax.

Below, we denote the decedent/giver as "person who raised property," heirs/accomplices and recipients as "those who gained property."2. When the representative in Japan has inherited or accepted property by inheritance/giftIn the case that a person having an address in Japan at the time of inheritance/gift gives assets, regardless of the nationality of the heirs/recipients, the person who got the property becomes the tax liability person of the inheritance tax/gift tax. Inheritance tax and gift tax will be covered not only for the feature in Japan but also for property outside the country. Therefore, even if foreigners acquire assets located outside of Japan due to inheritance etc. from families residing in their home country while staying in Japan, they will be subject to inheritance tax/gift tax in Japan, so be careful is. However, in the case of a short-term stay, the fee will be applied only to Japanese domestic property.3. When the resident in Japan becomes a decedent or a recipient in JapanEven if a foreign resident who is an heir to a foreign resident living in Japan has acquired property by inheritance etc., the address of the person who raised the capital when he/she got the property is in Japan, tax will be imposed on all property acquired regardless of the nationality of the person who got the property. In other words, we will be subject to inheritance tax and donation tax not only for the feature in Japan but also for property outside the country. Even if a foreign resident is living in Japan and died due to an unexpected accident or the like, even if the family inheriting property etc. lives in the home country, it is subject to Japanese inheritance tax, so be careful. However, if a foreign expatriate is a short-term stay, it will be taxed only on domestic property.4. When the expatriate in Japan has left the country after completing the duty periodIf neither the decedent, donor, heir or recipient has an address in Japan, it will be subject to inheritance tax/gift tax only for property in Japan. However, if the person who got the property has Japanese nationality, either the decedent/ giver/heir/ heir/giver should have the address in Japan within 10 years before inheritance/gift When there is a thing, caution is necessary because it will be subject to inheritance tax and donation tax not only for the property in Japan but also for property outside the country.5. Inheritance tax · Gift tax rateBoth inheritance tax and gift tax are taxed at a tax rate of 10% to 55%, but the inheritance tax and donation tax differ in taxable price to which each tax rate applies.6. Foreign tax creditIf inheritance or gift gives a person who gets property outside Japan, a tax equivalent to inheritance tax/gift tax is imposed on the international capital in the country where the foreign ownership is located (For gifts, Including cases imposed), double taxation will be adjusted according to the provision of foreign tax credit which deducts tax imposed on foreign countries from a certain extent from Japanese inheritance tax/gift tax.

-

-

-

Other major taxes

Besides, various fees are involved when doing business in Japan, but here is one example.· Property tax: A tax that is taxed on the holding of assets, tax depreciation of land, buildings and business depreciation assets is taxed at the rate of 1.4% to the owner as of January 1 of each year. (Declaration required for depreciable holdings for business)· City planning tax: Land and buildings in the urban planning area are taxed at a tax rate of 0.3%.· Business tax: For businesses in large cities such as Tokyo and Osaka, the business tax will be levied if the floor area exceeds 1,000 square meters or the number of employees exceeds 100 people. The tax rate is 600 yen per square meter of floor area, 0.25% of salary total.· Registration license tax: Tax imposed on receiving real estate, company registration, specific business license, etc.· Stamp duty tax: Tax subject to prescribed documents

-

-

-

■ Foreign tax credit and foreign subsidiary dividend income non-inclusion system

To eliminate international double taxation on income, foreign taxes on individual income of domestic corporations are allowed to be deducted from the Japanese fee within the deductible limit. This foreign tax credit system includes (1) those that target foreign taxes paid directly by themselves to domestic corporations acquired outside Japan (direct tax credit), (2) based on the provision of the tax treaty , A system (tax deferred tax) targeting taxes specially deducted and exempted from the treaty partner country, (3) responding to income of certain foreign subsidiaries etc. added to income of domestic corporations by applying so-called tax haven countermeasure tax system There are things that target foreign tax amounts to be made, etc.

Regarding dividends from certain foreign subsidiaries of domestic corporations that satisfy the holding requirement etc., a foreign subsidiary dividend income tax-exclusion system that excludes international double taxation through the handling of eliminating a fixed amount from taxable items. -

■ Transfer price tax system

In order to prevent the corporation from setting a transaction price with an affiliated company outside the country such as a parent company to a different amount from the regular price (interdependent enterprise price) and transferring the profit to the outside of the country, In the event that taxable income decreases due to different things, it is assumed that the transaction is deemed to have been carried out at an inter-company price and the tax amount is calculated. As a reporting system to allow tax authorities in each country to grasp the overall picture of the activities of the global enterprise, a corporation belonging to a specific multi-national corporate group shall be subject to accounting of the final parent company, etc. commencing on or after April 1, 2016 it was decided that a prescribed report must be submitted from the fiscal year. -

■ Tax Haven Countermeasure Tax System

To prevent a domestic corporation from avoiding tax by retaining income through a specific foreign subsidiary located in a so-called tax haven, the amount corresponding to that share of the retained income of the foreign subsidiary is set as taxable income of the domestic corporation, and we are subject to taxation. -

■ A tiny capital tax system

If the borrowing money that a corporation procures from a specific foreign controlled shareholder exceeds the capital stock by three times (or a reasonable alternative), the debt interest corresponding to the excess amount is said that it cannot be deducted for taxable income calculation. -

■ Overpaid interest tax system

In cases where a corporation pays interest, etc. to an affiliate such as a parent company outside the country, an amount exceeding 50% of the amount of attention spent on the income amount with a particular adjustment is not deductible for calculation of taxable income. However, it is not applicable when the amount of attention paid to affiliates is 10 million yen or less, and if it is less than 50% of the total amount of interest paid by the corporation.

Also, if there is an application of both this system and the under-capitalized tax system, the one with the more significant amount which cannot be deducted is applied.

-

-

-

Main treatment of corporation tax, local tax, consumption tax due to large/small capital amount

Depending on the capital amount of the capital amount (beginning or end of the term), the applicable system may change. -

■ Corporate tax

If the capital amount at the end of the time is less than 100 million yen, there are benefits as follows.(1) The reduced tax rate (15%) can be applied up to the income amount of 8 million yen in calculating corporate tax

(2) All entrance fees less than 8 million yen can be deducted(If the capital is over 100 million yen, in principle all of the entertainment expenses will not be deductible)(3) A small number of depreciable assets less than 300,000 yen can be deducted in full amount(However, it is limited to 3 million yen per year)(4) Exclusion of subject to tax reserves for specified family members(5) Full deduction for tax losses can be applied (9 years)(6) The carryback refund of the damage can be applied(7) Various special depreciation and special deduction can be applied -

■ Inhabitant tax and business tax relationship

Regarding inhabitant taxes, the smaller the capital amount, the lower the corporate resident's tax equally divided

Regarding business tax, if the capital amount at the end of the fiscal year exceeds 100 million yen, standard external taxation will be applied. -

■ Sales tax

In the case of setting up a new corporation, if the capital is set to less than 10 million yen, basically the consumption tax will be tax exempted for the two business years after establishment. As mentioned in the introduction at the beginning, if the sum exceeds 10 million yen, the corporate resident 's tax will be increased evenly..png)

-

■ Consumption Tax

The main items of tax treatment that differ depending on the amount of capital are as follows. Be sure to check with experts individually as to whether consumption tax exemption requirements are met..png)

-