Japan

Japan UnitedStates

UnitedStates China

China Hong Kong

Hong Kong Mongolia

Mongolia Russia

Russia Thailand

Thailand Vietnam

Vietnam Laos

Laos Cambodia

Cambodia Myanmar

Myanmar Indonesia

Indonesia Philippines

Philippines Singapore

Singapore Malaysia

Malaysia India

India Bangladesh

Bangladesh Pakistan

Pakistan Sri Lanka

Sri Lanka Mexico

Mexico Brazil

Brazil Peru

Peru Colombia

Colombia Chile

Chile Argentina

Argentina DubaiAbuDhabi

DubaiAbuDhabi Turkey

Turkey South Africa

South Africa Nigeria

Nigeria Egypt

Egypt Morocco

Morocco Kenya

KenyaMexico

7 Chapter Tax

-

-

1 Chapter Basic knowledge

2 Chapter Economic Environment

3 Chapter Establishment

3.1 Character of Business base

3.2 Establishment of business base

3.3 Necessary registration to other duties.

4 Chapter M&A

4.1 M&A case of Japanese company

5 Chapter Corporation Law

6 Chapter Accounting

7 Chapter Tax

8 Chapter Labor

8.1 Overview of working environment

9 Chapter Q&A

-

-

-

Mexico`s tax system

If you live in Mexico, or when you start trading with a Mexican company or doing a business in Mexico you will unavoidably have tax problems. It is notunusualrare that an unexpected tax burden arises afterwards if you trade in this state without this recognition. In this chapter, we will explain theoverallwhole picture of taxation system in Mexico, explanation of individual tax items, and international tax problems.With the revision and change of tax system in FY 2014, the corporate single tax (IETU: Impuesto Empresariala TasaÚnica) and the cash deposit tax (IDE: Impuestoalos Depositos en Efectivo) have been abolished that The IDE took

■ Types of tax items

The main tax items in Mexico are as follows.

.png)

[Federal tax]

Most of the taxes in Mexico are national federal taxes, such as corporate / personal income tax (ISR: Impuesto Sobrela Renta), value added tax (IVA: Impuestoal Valor Agregado), and etc. The tax collector The competent authority of national federal tax will is be the federal government.

[Local tax]

Local tax is the tax imposed on individuals and corporations, and the taxable entity the competent authority is the state government X or local government. Payment tax, real estate acquisition tax, property ownership tax, accommodation tax, and etc. are applicable as tax items of Mexican local tax.

■ System of tax law

The x Mexican tax law system, as x shown in the figure below, the constitution and the tax treaty exist as a superordinate concept of above each individual tax law. Also, since the revenue law including the revision and change of the tax law is revised every year, some tax reform is done every year. If the tax system revision is considered as unconstitutional one, the taxpayer can submit a protest the letter called AMPARO.

.png)

■ Features of the Mexican tax system

The characteristics of the tax system in Mexico are summarized as follows.

-

-

-

Tax on entry

■ Step 1. When doingStarting ayour business without establishing a base

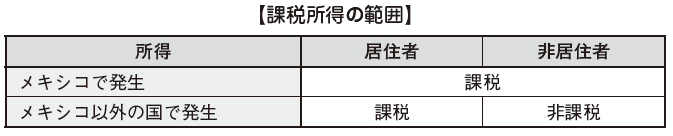

Even in with the absence of a base in Mexico, when you deal dealing with a company in Mexico, the tax problem accompanies arises that by transaction. In with the absence of a base in Mexico it is usually considered a "non-resident" and taxes will be imposed only on income generated in Mexico under the Mexican tax law. Also, even in with the absence of a base, you need to pay attention isx requiredx because there is a case where taxation is done levied in Mexico in as the form method of PE (permanent establishment) certification.

■ Step. 2 When establishing bases and doing operating your business

When After trading in of Mexico becomes get full-fledged, we you will develop a your business base basement with local bases ones. As Below below, we will examine give you guidance and example of the tax rules related connected to each form of extension, such as representative office, branch office and overseas affiliate.

a.[Whenx establishingx ax representative office andx activitiesx]

As forto the Representative Office (Oficinade de Representación), it is stipulated as "a foreign corporation that does not conduct its business in with the normal ordinary circumstances in Mexico" in the Civil Code Article 2736 of Civil Code., and sox basically nox income will you are not concerned with incomeoccur.

Therefore, there is no risk of direct income taxation on the representative office itself, but if this representative office is certified as a PE, it is deemed thatx there your office is sales office in Mexico and also foreign corporation As a result, and corporate income tax (ISR) will be imposed. on the income assumed to have occurred there.

b.[Whenx doingx ax businessx withx ax sales office suchx asx ax :branch office]

Regarding the branch (Sucursal), asx stipulated in Article 17 of the Foreign Capital Law as "a foreign corporation that you intends intend to conduct commercial business in a normal state in Mexico", income occurs incurred with in Mexico as a basically basic tax source country. There is no any other clear difference than this definition isx nox to tell from clearx differencex otherx thanx thisx withx the above-mentioned representative office, and it will be judgedregarded onx thex basis x ofx whether orx notx tox you are going to conduct a business practice under normalMexican ordinary circumstances or not. When a foreign corporation operates in as a branch office in Mexico, it falls must be under the tax law as a non-resident and also is taxed levied ( a country of withholding tax at the source countryx taxx) on income generated incurred in Mexico.

c. [Whenx doingx ax businessx withx ax local corporation setx upx]

If you set up a subsidiary office, you will be taxed in by Mexico Mexican government for income generated paid in all countries including Mexico tox bex ax as a domestic corporation in of Mexico (worldwide income tax). In addition, if income generatedx inx from ax other country countries otherx thanx Mexicox isx was alreadyx previously taxed in the other country and it would be becomes taken as a double taxation with Mexico, by applying the provision of foreign tax credit, the double taxable portion declined From from the amount of corporate income tax tox would be paid in to Mexico. As for to the relationship between Japan and Mexico, foreign tax credits are stipulated in the tax treaties between the these two countries, so the double taxation will be adjusted in accordingly according with these treaties.

■ Step 3. Verification of method of investment return methodx

If you make a move move to Mexico and gain profits through on-site your service and activities, you will have face the problem issue that of you plan to reserving keep this profit and reinvesting reinvest it to your branch or returning return it to the your headquarter and parent company. In the case of reinvesting in the local area, there are no special especially tax issues, but when if returning profits to the headquarters in Japan or parent company in x Japanx, taxx handlingx the way of taxation will be different depending on the refund method.

[Branch ➡ Returnx tox main store]

If a Japanese company establishes a branch office in Mexico and returns theits profits generatedx there to the head office in Japan, there is no tax on profit remittance to Mexico, so it is possible to refund profit to the head office without special taxation It will be possible.

[Subsidiary ➡ Return to parent company]

When returning profits generated by a subsidiary in Mexico to the parent company in Japan, there are the following methods.

① How to return to parent company by dividend

② How to reflow through transactions with the parent company

In case of (1), the withholding tax rate at the time of payment of dividends from Mexico subsidiary will be 10% in principle. Under the Japan-India tax treaty, the withholding tax rate on dividends is stipulated as 5% (dividend to non-affiliated companies) of dividends to the parent company, so it is advantageous to apply the tax treaty Dividends can be made to the parent company by the withholding tax rate.

Prior to the reform of the tax system in FY 2014, the withholding tax rate on the dividend of Mexico domestic law was 0%, which was better than the 5% withholding tax rate prescribed in the tax treaty between the two countries. Therefore, Preservation · Close (If domestic law is more advantageous than tax treaty, we could refund to parent company with 0% tax rate by applying domestic law preferentially, but changed to tax rate by tax system revision , We will compare the tax rate under domestic law and tax treaty and apply a withholding tax rate of 5%.

Also, for the parent company in Japan receiving dividends, dividends will be subject to corporate tax as income. However, as for dividends received from foreign subsidiaries, there is a "foreign subsidiary income-excluding system" which makes 95% of dividends non-profitable. The subjects that can be applied are as follows.

【Requirements to be eligible for tax-free system related to dividends from foreign subsidiaries】

In case of (2), tax rate of 25% or 30% withholding tax for nonresidents is applied under domestic law when paying management fee, system usage fee, royalty etc. to parent company. However, because the application of the withholding tax rate of 10% is permitted under the Japan-India tax treaty, in fact, the tax treaty rate that is more advantageous than the domestic law above will apply.

In case of (2), tax rate of 25% or 30% withholding tax for nonresidents is applied under domestic law when paying management fee, system usage fee, royalty etc. to parent company. However, because the application of the withholding tax rate of 10% is permitted under the Japan-India tax treaty, in fact, the tax treaty rate that is more advantageous than the domestic law above will apply.

-

-

-

Personal income tax

When calculating personal income tax (ISR) for those who lives in Mexico or locally dispatched from Japan, first of all, if the person concerned is "resident" or "non-resident" in Mexico's personal income tax law.In other words, the living status of the person concerned is important. Due to this status, the range of income tax will be different.

■ Definition of residents

In Mexico it is classified as a resident if the following conditions are fulfilled.

· A Individual who has address in Mexico

· The person who stays in Mexico for over 183 days within twelve months

The range of income tax depends on the classification of "resident" and "nonresident" as follow.

In Mexico residents, not only Mexico domestic income but all income incurred in other countries are taxed in Mexico. It is necessary to declare in so-called worldwide income (income tax law Article 153).

■ Salary income for short-term residents (Article 15 of the Japan-Mexico tax treaty)

In tax treaty, it is stated that taxation will be imposed on wage only in the country where actual business is performed. In other words, if “business” incurred as the source is not performed, taxation would not be applied to salary income in that country but tax will be imposed on the place of actual business in real. Traveling from Japan to Mexico, if the following three requirements are met with your company, Mexico side will not be taxed on remuneration or salary paid.

■ Taxation on executive’s compensations(Article 16 of the Japan-Mexico tax treaty)

With regard to salary income, in principle of tax treaty, taxation will not be applied as long as you do not work in Mexico. In other words, if employees are dispatched from Japan to Mexico, no taxation will be incurred on salaries on Japan side unless they work in Japan. However, there is note that an executive compensations is taxed on Japan side, if an executive who obtains remunerations from Japanese company becomes a resident of Mexico.

Duration of Tax

According to the Mexican tax law, the period of taxation is from January to December (taxation of calendar year) without exception. It means even though the business start month is not January, the taxation period is closed in December or that year.

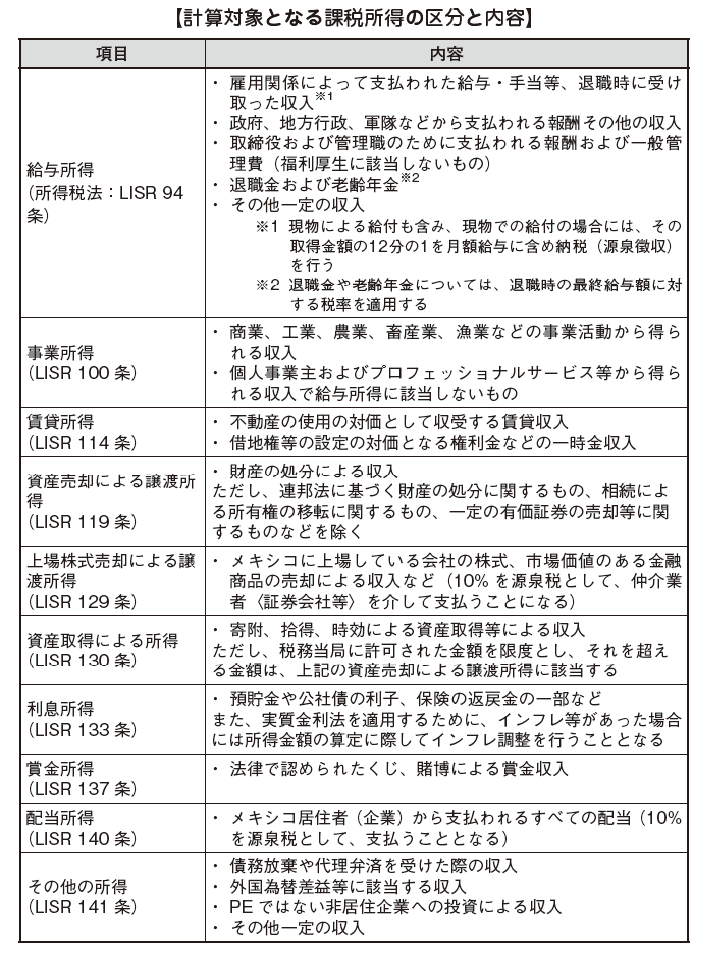

■ Calculation of the amount of income tax in Mexico

The calculation of income tax in Mexico is summed by the procedure of the following figure.

.png)

First, it is necessary to separate a total income of the year as taxable income and non taxable income. Below, we describe taxable income and non taxable income, income deduction, and tax rate etc.

[Range of taxable income]

The following table shows the taxable income in subject to the calculation of income tax.

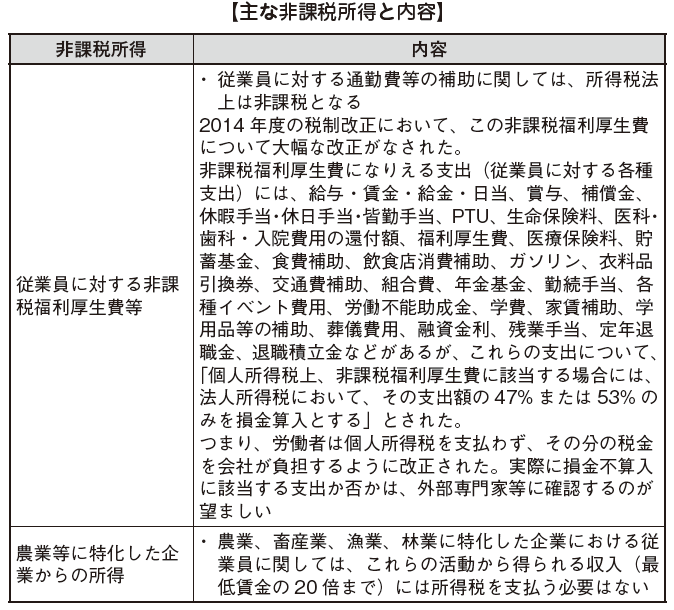

[Non Taxable Income]

As for the subjects of taxation of income tax, not all income of a individual is taken as income, but there are also incomes stipulated as tax exemption on the income tax law : LISR, Ley del Impuesto Sobre la Renta. The main "tax free income" is as follow.

[The amount of Income Deduction]

The amount of income imposed with income tax is calculated by deducting the amount spent on the income from the total amount of income. However, due to the revision of the tax system in 2014, a deduction limit was up to 95,000 pesos. The expenses deducted possibly from the amount of income are as follows.

However, this income deduction is not allowed for taxpayers who earn salary income only. Also, it is necessary to keep in mind that even though you prepare for the balance sheet saying deposit and withdrawal statement of the bank as evidence of the payment fact, with only this action you will not be accepted for deduction.

.png)

In fact, items of income deduction will change, depending on the type of income.

In general, the items of expense are listed on the above table and will be deducted from the income amount, according to the type of income.

Further, in Article 147 of LISR the specific requirements in order to take income deduction are stipulated as follows.

Requirements for income deduction (Article 147 of LISR)

· The indispensable expense to earn income

· The limit of the amount of income deduction in the amount of investment as 5% of the purchasing price for the building, 10% of the purchasing price for the facility, 30% of the purchase price for the equipment such as computers, and maximum 10% of the purchasing price for the other properties.

· In case of a lease contract, it must be subject to Article 38 of LISR.

· Payment over 2,000 pesos must be done with electronic transfer such as checks and credit cards.

· Obtaining a taxpayer registration number(RFC).

· Income deductions terminated by basing on receipts, invoices, or other proofed documents such as evidence of payment to Mexican Social Security Institute: Institute Mexicano de Suguro Social called as IMSS with fulfilling the requirement of taxation.

· The tax deduction conducted in the taxation year that you started check payment if you paid by check.

· Fulfilling tariffs, payment of IVA, and the other legal requirements if you pay toward the import stuffs.

· Fulfilling the other requirements of deductions.

As to various payments listed in Article 148 of LISR, it is not possible to deduct these cost s from the amount of income. The expenditure items of non income deduction are as follows.

Expenditure of non income deductible(Article 148 of LISR )

· Payment of income tax by taxpayers

· Payment of subsidy to third parties

· Employer's payment of social insurance fee

· Payment for private purpose

· Payment of donation etc.

· Payment of penalty or insurance of damages

· Various payments unconcerned with income

· Payment of IVA and service tax

· Temporary and accidental loss

· Payment for entertainment expenses

· Regular payment for other matters

For the objective of provision, Article 147 and 148 are considered as prerequisites for income deductions. Among expenditures that satisfy this prerequisite, they are confirmed as expenses deducted from income by the provision of tax deduction.

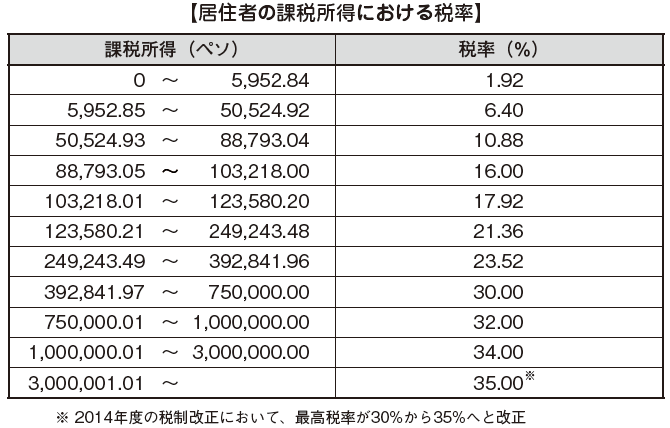

■ Tax rate

Eleven progressive taxation rate is applied to the residents who are subject to levy personal income tax under Income Tax Law, depending on the amount of taxable income decreased all of various income deductions from the total income. The tax rate of non-residents is 25% tax rate mostly, depending on the content of their income in according to Article from 153 to 175 in LISR.

■ Notice and Payment Procedure

Payment deadline of Personal income tax is separately determined for annual and monthly notice. If total annual income is 400,000 pesos and also interest income exceeds 100,000 pesos annual notice is mandatory. Also, if the rent revenue is approximately more than 19,687 pesos per month, you have to fulfill an obligation of estimated payment every three months. The deadline of payment of annual notice is until 15th April and the taxpayer is required to submit the tax notice and pay taxes by the date, but if you do it by the electronic notice, the deadline is postponed until 30th April.

The deadline of payment for monthly notice is the 17th day of the following month after income was paid, taxpayers must present a tax notice and pay taxes on schedule. If 17th is a holiday, it is necessary to notice and pay by the next day. Also, in the case income is only salary income, personal income tax is withheld on the time of payment, so there is no need to notice and pay tax. Please review "withholding system” of the next paragraph.

In addition, due to the revision of the tax system in 2014, it required you a withholding sheet of the total amount of annual salary and an issue of electronic payroll statements.

■ Penalty provisions of personal income tax

In the case of personal income tax, if you do not pay taxes three times, you need to pay all of amount without exception. If you can not pay them all at once, since the seizure proceeding will start. That’s why it is advisable to pay it monthly on schedule. -

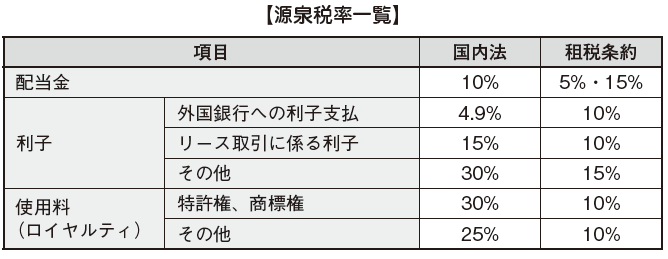

Withholding tax system

Withholding system is a system to pay the tax amount withheld by taxpayer to the government on the time of payment for certain transaction. Tax treaty has been entered between Japan and Mexico and it is possible to apply the declined rate of tax treaty rate on dividends, interests and royalties. As mentioned above, withholding tax of 10% on the dividend will be newly imposed on the tax system revision in 2014. As for the withholding tax of the dividend, it had been confirmed as 0%, so it increased in practical.For calculation of withholding tax on dividends, we use the calculation of CUFIN ; unappropriated profit on revenue, so we need to clarify the amount of CUFIN up to 2013, the one of CUFIN from 2014 and its classifications. And, regarding to dividends for foreign persons and companies concerned by tax treaty, it refers the rate must not exceed over the range of 5%, therefore it is possible to pay a dividend to them with a withholding tax rate of 5% It will be possible. However, in Japan, if the amount received for these transactions excluding dividends is treated as a tax exemption, the amount of payment in Mexico can not be included in the amount of loss in Mexico. In order to include the payment amount in Mexico into the amount of loss, you are required to prepare for the documents that these transactions are taxed in Japan, and furthermore if on the document a legal representative in Japan must sign. At last, you are required to preserve the document in Mexico.

■ Withholding tax on residents and non-residents

The employer of salary will levy withholding tax from all employees as long as they are Mexican residents. Also, if not, we will notice the amount of compensation in the same state. (LISR Article 96)

■ Payment of withholding tax and schedule of its notice

You have to file a withholding tax of the previous month on Ministry of Labor and SAT on 17th of every month. In regard with notice, it is possible to notice them by internet. However, you have to note that payment is done to SAT separately. And, according to Article 97 of LISR we calculate a withholding tax imposed on the salary by summing the amount of income tax based on all amount of yearly income at the end of the year like the adjustment way of Japan. Then, if there is excess or shortage, it should be noticed to SAT concerned by the end of February of the following year as well as a request of refund return. However, if there is an income other than salary or a foreign withholding income, or in the case an employee resigned in the middle of the year, work under some employers, or an annual salary income exceeds 400,000 pesos In case you need to file a tax return referred to Article 98. Also, employers are required to give annual withholding sheet to all employee by 15th February referred to Article 99.

■ Penalty Provisions of Withholding Tax

Based on the procedure stipulated by law, if you do not notice and pay a withholding tax. tax authority will penalize you as you performed a false notice. In this case, the amount of fine will be determined the range from 70% to 100% of unpaid tax with consideration of interest, inflation rate and others, between 70% and 100% of the taxes not paid. -

Corporate Income Tax

■ Taxpayer and taxable incomeIn Mexico, corporate income tax is stipulated in income tax law, taxpayers subjected to corporate income tax are classified into domestic corporations and foreign corporations, and as a result the range of taxable income according to each classification is different.

A domestic corporation is a legal entity established or registered pursuant to the laws of Mexico. A foreign corporation is a corporation which operates domestically in Mexico, but has not been established or registered in Mexico. For domestic corporations, corporate income tax is imposed on global income. Therefore, if tax income occurs outside Mexico in double taxation in Mexico, tax credit can be adjusted by foreign tax credit deduction.

[Domestic corporation]

All incomes including domestic and foreign withholding income during the taxing year are imposed as worldwide income tax.

[Foreign corporation]

Only withholding income incurred in Mexico during taxable year is levied as withholding tax at the source. However, even a foreign company also must pay the tax to Mexico as Mexican resident company if the following requirements are fulfilled.

· Companies which more than 50% of income arise in Mexico

· Companies whose main place of activity is Mexico

Even in other cases, it is considered to be a resident enterprise in Mexico if it is deemed that it is substantially administrative corporation in Mexico. Regarding this resident enterprise, a number of supplementary provisions are prescribed in the regulation of the Ministry of Finance, but if the person performing the management of the company is registered as taxpayer in Mexico or has an office in Mexico these corporations are regarded as a resident enterprise.

Duration of Tax

Based on Mexico's income tax law, the taxation period is applied from January to December (calendar year taxation) without exception. Even in the case business starts other than January, the taxation period of the corresponding year will be separated in December and tax calculation will be done.

■ Deductible calculation (benefits and losses)

[Benefit]

Benefit refers to income on the point of tax. Specifically it includes all incomes except confirmed as non-taxable items separately determined in Mexico.

Profit Items of Non Taxable

· Capital transactions

· Gains from revaluation of assets and liabilities by inflation accounting

· Dividend from Mexican companies

Loss

In calculation of income for Mexico's corporate income tax, the requirements for inclusion in the amount of loss for tax purposes out of expenditure are as follows.

Requirements for deductibility

· Indispensable Loss for conducting business activities

· The invoice must meet tax requirements

· The invoice printed by the tax authority concerned or approved by the tax authority concerned

· Loss listed in the book as expense in accounting

· Payment over 2,000 pesos by check or electric money

· Benefit of welfare expenses fulfilled with requirements of equal opportunity.

· Actual cash payment outgone for service charge of companies to provide a professional serve and an individual and wage of the personal.

· Tariffs paid for imported goods from overseas

· The condition the place of restaurant to eat and drink locates over 50 km from the registered place of taxpayer in order to sum as full expense. Otherwise up to 8.5% of expense will be summed.

About the tax requirements of the invoice

· Name, company name, address, and taxpayer registration number must be stated

· Sequential numbers are attached

· Issued place and date must be attached

· Taxpayer registration number of invoice issuer is attached

· The amount and the contents of the expenditure must be stated

· Described of a single currency, depending on the amount

· In the case goods are imported, the custom number and date are attached

· Printers' certification data and date of printing approved by tax authority

· Electronic invoice

However, the following items can not be included in the amount of loss.

Items of non Deductibility

· The sum of provisions and its amount.

· Certain amount of taxes such as corporate income and asset tax

· Depreciation expenses of company cars exceeding 175 thousand pesos (electric vehicles and hybrid cars may be up to 250 thousand pesos)

· Car rental fee exceeding 200 pesos per day

· Goodwill charge and amortization expense

· Amount exceeding 47% or 53% of tax exempted welfare expenses ; either is applied depending on targeted benefit welfare expense.

· Cost calculation by the last-in first-out; LIFO method

Individual Points to Note on Calculation of Deductible Cash

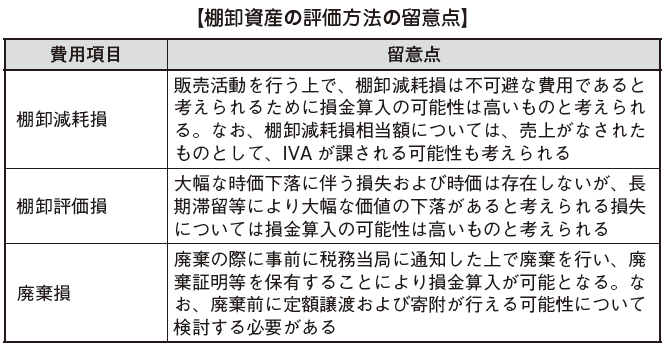

[Inventory Asset]

Evaluation method

The first-in first-out; FIFO method, the average cost method, the selling price reduction method, and the individual method can be optional as the inventory valuation method. As a result of the reform of the tax system in 2014, cost calculation by the last-in first-out method is no longer allowed. Individual method is enforced to use to products and selling products identified by serial number and exceeding 50,000 pesos.

Regarding losses of valuation loss, the requirements for tax deduction of the following items are strict and procedures are strictly regulated. However, there are unclear items in Mexico today.

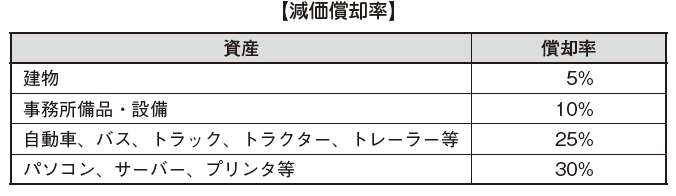

[Depreciation expense]

Depreciation expense for depreciable assets is calculated by using the following formula.

Depreciation expenses = acquisition costs x depreciation rates x inflation adjustment factors

Inflation adjustment factor divides a nationwide consumer price index at the end of the current fiscal year by the national consumer price index of fixed monthly acquisition month.

The depreciation rate related to depreciation is as follow.

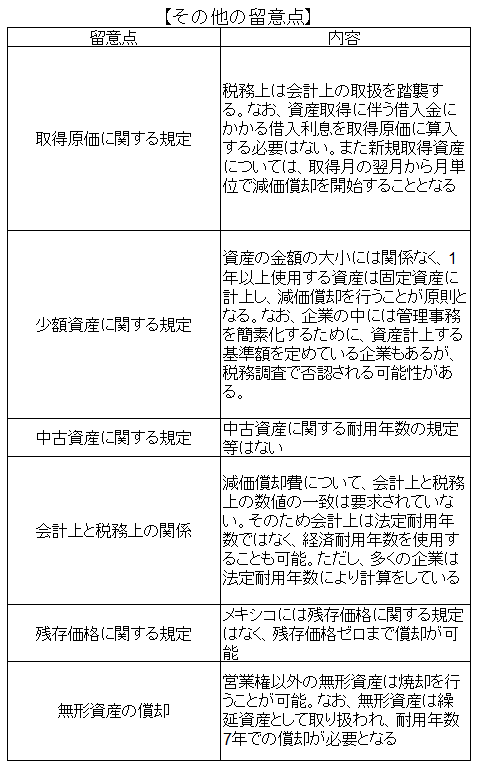

Among the matters related to the calculation of depreciation expenses, the following table shows other points to be noted.

[Provisions]

Provisions included in the amount of loss for tax purposes are restricted to the following items and the reserves for retirement benefits, warranty for product and provision paid for vacation can not be included in the amount of deductible expenses.

[Payment of dividends]

Companies that pay dividends have different treatments about corporate income tax depending on whether the dividend resource is profit before or after tax. In the case of paying dividends with pre-tax profit as dividend resource, the amount of tax calculated by multiplying the corporate tax rate with the amount grossed up the corporate tax rate must be paid on the dividend amount by the 17th of the following month after the dividend was distributed. Also, as to additional taxes due to dividends, it can be offset against income tax incurred over three years since the year dividend was done. In the case of using after-tax profit as a capital, it is a profit after the corporate income tax has already been deducted, so additional tax payment is not especially necessary.

[Reserved losses]

For the reserved losses incurred in Mexico, a duration of 10 years for deduction is allowed after this losses arose.

■ Inflation Finance on Tax Revenue

In calculating Mexico's corporate income of taxable income it is necessary to consider the impact of inflation. The method of calculating taxable income is as follow and the amount calculated by this formula will be treated as a tax benefit item or deduction item.

[Method of calculation]

Calculation of monthly average monetary assets and monthly average monetary liabilities

= (Total of final balances on accounting at the end of each month) ÷ (the number of months in the business year)

Estimated interest is not included into the calculation of monthly average monetary liability.

When taxable income increases as a result of considering the influence of inflation and also the monthly average monetary liability amount is larger than the monthly average monetary asset amount, the taxable income increases with an excess amount multiplied by the inflation rate.

When taxable income decreases as a result of considering the influence of inflation and also the monthly average monetary asset amount is larger than the monthly average monetary liability amount, the taxable income reduces with an excess amount multiplied by the inflation rate.

This calculation is not related to inflation finance on the accounting, and also even though you should carefully note that you have to use the inflation finance on tax revenue, despite you do not have on accounting.

■ Tax rate

The amount of the Mexican corporate income tax is calculated to multiply the taxable income amount by the tax rate of 30%.

■ Tax return

[Annual file of corporate income tax]

The tax year of Mexico is the calendar year (January 1 - December 31), and for annual notice there are three kinds of submits; one is normal (Normal), another correction (Complement aria) and the other is correction of tax audit(Complementaria por Dictamen. Annual notice must be submitted by March 31 of the following year after the end of the taxable year. For annual notice, it is necessary to match the a total amount of 12 months with monthly notices. if not matching, monthly notice is required to correct.

[Monthly planned payment of corporate income tax]

The deadline for payment of monthly notice is the 17th day of the following month after income arises, and the taxpayer is required to submit the tax return and pay the tax so far. If 17th is a holiday, it is necessary to pay the corresponded tax amount by the day after the holiday. The paid tax amount is calculated based on the profit of the previous year. Also, the amount of planned payment tax after the early half of the year can be reduced only with approval of tax authority, due to the situation of cash flow.

Tax audit

An independent accountant can elaborate an annual tax audit report (Dictamen Fisical) and submit it by the end of June if the amount of actual achievement of the previous year meet one of the following requirements. You can not submit it if one of the following requirements does not meet your company’s situation.

① Total asset exceeds 79 million pesos

② Gross income exceeds 100 million pesos

③ The number of employees in each month exceeds 300

④ The company concerned located in Mexico meets either the above requirements from (1) to (3).

Toward taxpayers applying this tax audit system in Mexico, tax investigation is rarely done. This is because tax authority should asked questions to the accountant who conducted the tax audit, but in certain cases such as the accountant who conducted the tax audit can not answer the authority's question, the authority can ask the taxpayers about the payment after questioned toward the accountant. -

VAT

■ Outline of IVA

VAT in Mexico (IVA) is an indirect tax prescribed in the Value Added Tax Law (LIVA: Ley del Impuesto al Valor Agregado) and has the following characteristics.

· It is an indirect tax imposed on the consumption of goods and services

· Tax burden is imposed on the ultimate consumer

· Intermediary agents do not bear tax, but they are obligated to a tax liability.

· There is an obligation to notice and pay each month ; to submit notice and pay tax by the 17th day of the following month after IVA arose)

As Japan's consumption tax, 16% VAT will be regularly taxed in Mexico on selling goods and providing services.

■ Taxpayer

IVA's bearer is the ultimate consumer, but the obligation of tax liability is the business entities that sell the taxable goods of IVA and provide services, as well as importers of goods ; IVA related to the collection of taxable cargo:, Tax obligation arises regardless of individuals or corporations. All employers who perform the businesses that conduct so-called sales activities in Mexico, such as selling, manufacturing, importing, exporting or providing services for the purpose of business, must be registered with the taxpayer registration number.

Taxable transaction

The taxable transactions of IVA are as follows.

· Transfer of assets

· Providing of services

· Crediting of assets

· Importing of a taxable cargo

In Mexico, the above-mentioned transactions which a employer performs business to aim for the charge of service are subject to IVA taxation.

"Assignment of assets" includes not only sales of goods and products, but transfer of business equipment, transfer of intangible assets such as patent and license and others. Furthermore, spot investment and substitute payment are considered as assignment of assets.

"Provision of service" refers to providing services such as eating and drinking, transportation, repairing, construction, storage, intermediation, advertisement, accommodation, information, etc., including advisory services based on expert’s knowledge such as lawyers and accountants.

"Crediting of assets" means any act letting others use assets, including loans of right of intangible property as well as lending of goods.

"Importing of taxable cargo” means taking over foreign cargoes from bonded areas.

■ Tax exemptions

For the following transactions, as tax-exempt items IVA is not taxed.

· Transfer of land and residential buildings

· Transfer of books and newspapers

· Transfer of Share

· Transfer of used household goods

· Transfer of lottery

· Other transactions of certain food, medical, educational and others.

■ Tax exemption

Transaction of export is true of the transaction of tax exemption. This is because the idea of IVA is based on the principle of consumption taxation at the place, and many indirect taxes including Mexico IVA, Japanese consumption tax, and foreign value added tax are levied at the final consumption place of the targeted goods etc.

IMFTX : Industria Manufacturera, Maquiladoray de Servicios de Exportacion: Export-oriented manufacturing, Macquiladora service industry: Import transactions of IMMEX goods made by companies are also exempted from tax; IVA exempted on withdrawal, however, due to taxation reform in 2014, this is prohibited. In addition, certain transactions such as transfer of assets among nonresidents are tax exempt transactions.

■ The amount of Tax Base

The amount of consideration such as assignment of taxable property and provision of taxable service will be IVA 's amount of tax base. The amount of tax base is agreed by the parties and is the transaction price stated on the invoice.

Also, because Mexico adopts the invoice method in calculating the amount of tax base, invoice is very important as a basis for IVA calculation (deduction and refund). In addition, since IVA is taxed on a cash flow basis, even if there is a cash movement due to advance payment, provisional payment, etc., IVA may be taxed Therefore, please be careful. The invoice in Mexico is called Factura which means invoice. In this chapter we will explain tp use the word of "invoice".

[Invoice and Recording system]

There are two methods of calculating IVA: one is an invoice method and the other is a recording one. Invoice method is adopted in Latin America region including Mexico and EU countries, and others. It is possible to make a calculation of accurate purchase tax deduction amount excluding arbitrariness by calculation of tax amount by using invoice for each transaction. On the other hand, the recording system is adopted in Japan. The recording system is the system to deduct the total of purchasing during the same period multiplied by the amount of tax rate from the total of sales multiplied by the amount of tax rate..

■ Calculation of payment tax amount

The payment tax amount of IVA is calculated by multiplying the tax base amount of the sale of goods and the providing of services by the tax rate of 16%. IVA is the indirect tax that you basically pay the rest deducting input IVA from output IVA.

[Output IVA]

The seller charges IVA to the buyer when selling the taxable goods or taxation service. From the side of the seller, this IVA will be the output IVA (provisional receipt IVA, sales IVA).

[Input IVA]

Buyer must pay IVA to seller when purchasing taxable goods or taxation service. From the side of the buyer, this IVA will be Input IVA (Prepayment IVA, Purchase IVA). If the purchased taxable goods and taxation services are within the range associated with buyer's business, this input IVA can be offset with the buyer's output IVA. Likewise, the seller can offset the output IVA with the input IVA that he/she paid when purchasing taxable goods and services.

[Offset of Input IVA]

The IVA has to be noticed and paid to the tax authorities every month. The input IVA of a specific taxable period :month must be basically offset and deducted from the output IVA of the same taxing period. The fact of proper invoice of IVA is particularly important in offsetting the input IVA, and the invoice of IVA should contain the following information at least.

Description requirement of invoice of IVA

· Name, company name, address, taxpayer registration number must be stated

· Sequential numbers are attached

· Issued place and date must be attached

· Taxpayer’s registration number of invoice issuer is attached

· The amount and the contents of the expenditure must be stated

· The amount of IVA must be stated

· Described by a single currency depending on the amount

· In the case where goods are imported, the customs clearance number and date are attached

· Printers' certification data and date of printing approved by tax authority

· Issued by electronic invoice

■Notice · Tax Payment

If the cumulative amount of output IVA for a month exceeds the cumulative amount of input IVA for the same period, the taxpayer can file the different amount of tax return. Basically tax return of Iva is not filed yearly but monthly. Therefore, IVA's payment must be done monthly. The taxpayer is required to file a tax return by the 17th of the following month. In addition, as well as ISR (corporate income tax), if the following 17th is a holiday, you will be required to pay it by the day after the holiday.

Refund

If the cumulative amount of input IVA for one month exceeds the cumulative amount of output IVA for the same period, it’s possible the taxpayer refunds the difference : the refund of the IVA is not filed yearly but basically a monthly. Since the refund of IVA is performed up to the application, in case there is a refund of IVA, it is necessary to request tax refund without a delay to the tax authorities. In many other countries, the refund of VAT is not done in many countries, but in Mexico IVA refund is done properly. The actual period until the refund is about 2 to 4 months.

It is also possible to offset the tax amount with the amount paid after the next month without refunding.

■ Penalty

If taxpayers who have a tax liability neglect their registration, they are obliged to pay penalties in the range from $209 to $629 US dollars, and unless they comply with the request of registration more than one year, they can be imposed of an imprisonment sentence from three months to three years.

■Changes by Tax Reform in 2014

As a result of the reform of the tax system in 2014, the tax rate in the border regions was raised from 11% to 16.,IVA rate was certainly 16% in the whole Mexico. Also,, we are subject to taxation on the services of surface public transportation outside of the urban area. Moreover, the exemption provisions of IVA has been canceled as the following items.

· IVA in temporary imports pertaining to the companies concerned with IMMEX

·IVA in temporary imports relating to the companies concerned with maquiladola : boned processing system

·IVA of Temporary imports related to the automobile companies concerned

·IVA of Temporary imports related to bonded warehouse

·IVA of Temporary imports related to strategic bonded facilities

·IVA related to sales from a foreign company with inventory in Mexico to a company concerning with INMEX

As you can see from the above description, the exempted benefits of IVA on IMMEX and Maquiladora were greatly cut. Because requirements and continuation requirements are complicated, it is necessary to decide whether to use IMMEX after firmly estimating the management cost. However, once your company is a member of IMMEX within one year from the day when you published to official telegram in order to be approved of IVA exemption by the Mexican tax authority, you can continuously obtain the most of benefits of the company concerned with IMMEX

-

Tariff

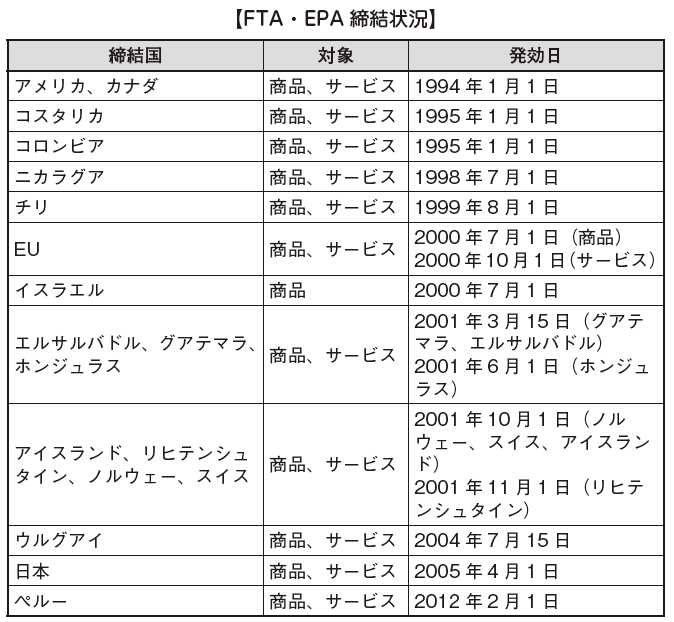

Tariffs are confirmed by the agreement of Ministry of Finance (SHCP: Secretaría de Hacienda y Carrédito Público) and Economic (SE: Secretaría de Economía), and both ministries have authority to set up. Although valorem (taxing according to imported amount) is ordinarily calculated, depending on specific items, targeted tax (taxing according to imported weight) is done based on CIF price (price composed of three factors, insurance, fee, and freight). Tax rate is calculated based on the one stipulated of HS code (Harmonized System Code). Tariff system in Mexico is so complicated that you need to apply for importer registration on the import business. Import notice must be either reported by customs clearance officer. This officer must be Mexican who has her nationality and the number is limited. That’s why it is a matter of concern for importing companies. Tax rate is calculated based on the HS code in ordinary import, so it is different for each imported items. Not only tariffs, it is also necessary to IVA imposed on withdrawal of taxable cargo, custom service’s fee of 0.8% and honorarium for custom clearance.Companies targeted by IMMEX and PROSEC (Program of Sectoral Promotion Program) can use the privileged tariff system, but only the companies approved by tax authority can take the benefits of IMMEX because of the reform of the tax system in 2014, the requirement is stricter for approval of joint and renew of benefit as time goes.

■ Other privileges of tariffs

Mexico has concluded various prior trade agreements in Latin American Integrated Coalition, ALADI: Asociación Latinoamericana de Integración). The agreement of ALADI is called the ALADI Economic Complementation Agreement, ACE: Economic Complementation Agreement, and the status of entry is as follow.

· ACE No. 6 (Argentina, January 1987)

· ACE No. 8 (March 1987, Peru)

· ACE No. 53 (May 2003, Brazil)

· ACE No. 55 (January 2003, Brazil, Argentina, Uruguay, Paraguay)

ACE No. 55 is a framework of privileged tariffs in the automobile industry,. Particularly, the trade with Brazil and Argentina often arises. The status of the entry of the FTA (Free Trade Agreement) and EPA (Economic Partnership Agreement) is as follow.

-

PTU (Labor Profit Distribution)

One of the important matters is PTU system when you enter into Mexico. PTU refers to distribution of profits to workers, which means the system that distributes 10% of the company's pre-taxed net income to the workers. PTU was contained in the labor law from the characteristic perspective of protection of workers in Mexico. Afterward, although labor law had been revised frequently, there were not so many changes about PTU. However, due to the drastic revision of labor law in December 2012, the paragraph of PTU was revised for the first time. Specifically, the range of workers receiving PTU was limited to those who directly employed until the revision of labor law, but to those who are deemed to be directly employed after revision The range has expanded.In other words, even though you take the form of dispatching or outsourcing workers, there is the possibility of paying PTU if they are deemed to be employed directly by outsourcing company. Eventually in Mexico, many companies use schemes to avoid PTU. It is a scheme to set up an outsourcing agency separately from the operating company when entering into Mexico to establish the business, and send the outsourced employees to the operating company.

Although we described as "when entering into Mexico to establish the business," you will face the conflict against labor union after establishment of incorporation and gaining of profit..As a result, it is tough to register the employees into outsourcing company.. However, the revision of labor law in 2012 hits this scheme of unspoken agreement above-mentioned and even now there is a chaotic situation in the market regardless of the history of company. It seems that many domestic and foreign companies that had taken countermeasure and protection against PTU has submitted an opposition proposal for amendment and revision of law called AMPARO to the government, but it take a couple of years to establish the determined system. Up to local lawyers’ opinions, we need to be concerned carefully to this system in the future.

■ Calculation of Total Payment

Based on the following formula, PTU's total payment (deductible amount) is calculated.

[Calculation of total payment amount]

Taxable taxable income (* 1) ± inflation adjustment amount ± dividend income · foreign exchange adjustment amount (※ 2)

= Profit of PTU

PTU profit × 10% = payment amount (deductible amount included (※ 3))

* 1 Taxable income before deduction of reserved losses

* 2 Only the ones was come out, the amount before inflation adjustment

* 3 PTU's deductibility has been possible after 2005

The basic figures of calculation of PTU is the amount of taxable income on tax revenue and it is linked with corporate income tax calculation. In other words, the tax rate 40% added the total corporate tax rate of 30% and PTU 10%, is the efficient one of Mexico's corporate income tax. In other developed countries, there are few countries which have an efficient tax rate of 40%. Actually, Mexico is one of highest tax rate in the world.

Distribution method

A half of total PTU's payment is proportionally divided by the number of working days of employees and the other half is proportionally divided based on salaries of employees. Also, the considerations of PTU distribution are as follows.

· Divided basing on employee's salary, salary shall be regular one

· Directors shall not be included into PTU

· Target only employees whose number of work days exceeds 60 days

· Absent days due to reasons such as injuries of work shall be included in working days

■ Calculation of distribution amount

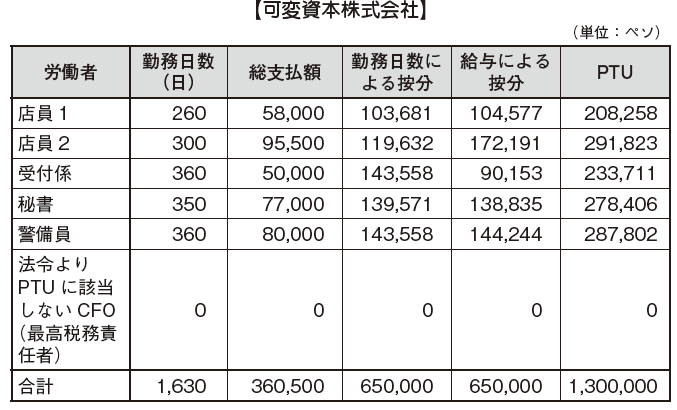

According to the above calculations, if the total payment of PTU is more than 1.3 million pesos, you distribute the total payment amount to each employee as follow.

[Example: Case of shop assistant 1]

Total payment 1,300,000 × 1/2 = 650,000 pesos

Proportion by number of working days

650,000 × 260/1, 630 days = 103,681 pesos

Proportion by salary

650,000 x 58,000 / 360, 500 pesos = 104,577 pesos

Distribution amount to clerk 1

103, 681 pesos + 104, 577 pesos = 208, 258 pesos

■ Subject of payment exemption

Payment of PTU is a heavy burden for companies, so PTU payment is exempted for certain companies. The companies subjected to exemption are as follows.

· Companies within one year after establishment

· New companies that manufacture new products approved by law (exemption for two years)

· New enterprises engaged in natural resource development business (Exploration period only)

· Not-for-profit organization certificated by law

· Companies with capital equal to or less than the fixed amount approved by both Ministries of Economic and Labor

Payment deadline

Employers are required to distribute to employees within 5 months from the end of the term ; within 2 months from the deadline of payment notice. Also, In the case the employees can not obtain PTU, the amount will be added to the one of PTU of the following year.

Scheme

As to countermeasures against PTU before the revision of Labor Law in December 2012, as described above, you can establish a company and an outsourcing company to operate when establish an incorporation, and transfer those employed at outsourcing company to operating company. You could use a scheme of avoiding PTU payment.

However, due to the revision of Labor Law, the nowadays scheme is questioned and the situation in the future remains uncertain. As of 2015, there are still many uncertainties about PTU countermeasures, but at the beginning of the establishment, you will use an outsourcing company with different capital and at the beginning of the establishment register all of expatriates’ name as executive staffs while paying attention to the situation to consider another scheme until this provisions are fixed. -

Appeal procedure against Tax Survey and Tax Reform

Appeal Procedure for Tax Survey

If you are dissatisfied with the results of the tax investigation, you can submit a petition or a lawsuit to the tax authorities within 45 days after tax return. Besides, lawyers and accountants basically prepare for the petition and will advise you. It is necessary to clarify the objective reason and the evidence. At that time we will attach the opinion report of the tax authorities concerned to it.

If the above procedure is conducted to the tax authorities within 45 days after filing, an objection report will be issued within 3 months by them. If you are dissatisfied with their result, you will be able to claim a lawsuit of tax revenue. Once the judgment is disadvantageous for taxpayers after trial is terminated, you can appeal to the federal court within 45 days and the result of this federal court will be the final conclusion.

Appeal Procedure for Tax Reform etc.

Companies can file a lawsuit in the court if the tax system revision is unconstitutional against the Constitution reflecting on the revision of tax law. Even in this procedure, lawyers or accountants will support them as advisors.

Besides, it is indispensable to finish n the appeal procedure within 30 business days after the enforcement of the law. In order to this, you must clarify why the tax system revision is unconstitutional in the complaint .

-

Money Laundering Laws

In Mexico's law against the informal economy, there was what is called a cash deposit tax (IDE) before the reform of the tax system in 2014. The IDE was to impose tax (withholding tax) when depositing more than a certain amount in a bank, and to crack down unidentified cash of origin route at the source. However, due to the reform of the tax system in 2014, IDE was abolished and the law against the informal economy was integrated into Money Laundering Laws.

■ Application of money laundering laws

The following four points are important in thinking about money laundering laws.

· Targeted transaction

· Type of business

·Transaction amount

· Vulnerability assessment

We will confirm each item as below.

[Targeted transaction]

Transactions subjected to the money laundering laws are not limited to transactions by cash, but all financial transactions including interbank transaction, check shipment, etc. are eligible.

[Type of business]

In Article 17 of Money Laundering Law, all targeted industries are enlisted. In Japan, Common companies such as a manufacture, distribution, and sales business of automobiles are listed the subject industry of the money laundering related law.

[Transaction amount]

According to Article 17 of Money Laundering Law, the transaction amount is enlisted in the same way as the kind of industry. The calculation of the amount is based on the minimum wage. It is described how many times of rate it shall be multiplied in the same article. In the manufacturing logistic business of automobiles., if the transaction amount exceeds the following amount, you are subject to money laundering law.

64.76 pesos (minimum wage, in 2013) × 6, 420 times (magnification of marketing business) = 415, 759 pesos

Therefore, transactions exceeding 415,759 pesos must be under money laundering law.

[Judgment of Vulnerability]

Since the possibility of money laundering depending on company is different, Money Laundering Law stipulated that SAT will verify and conclude the vulnerability indicating the different possibility. For that reason, the content of materials required from SAT is also considered differently for each company.

Procedure provision

According to the Money Laundering Law, in order to prove that your company is not involved in the informal economy, you are required to submit a material of your own registration ; the document that someone else can confirm your identity , one of the opponent’s registration ; document that you can confirm their identity as well, information of activities, and information of those who obtain economic benefits. However, nowadays , we just preserve the corresponded materials. Just in case that there is a request from the SAT, you have to submit the materials without delay. These materials are required to be stored for five years after submit. Besides, to establish a new incorporation in Mexico including a representative office and a branch from April 2014, you are required to submit the following documents caused by money laundering law and the content of guidance will more specific little by little.

① A certified copy of the registry of the parent company

② Nationwide tax notice of the parent company ·identification user number of the tax payment system

③ User ID number of the individual tax return of the shareholder of new company in Mexico or the recipient number in the withholding sheet of the salary income for the corresponding year

④ ID card attached with photo of the shareholder of new company in Mexico : a copy of passport

⑤ A resident document and a certified copy of official family registry of the shareholder of new company in Mexico

With the submit of (1), you can certify that the registered address of the parent company and the representative director are representative on registration.

With the submit of (2) you can prove that the parent company who will become the shareholder in new company in Mexico is the one that pays tax overseas.

With the submit of (3) you can prove that the shareholders of new company in Mexico are the individuals who are paying tax overseas.

※ (2) and (3) only certify TAX-ID of so-called taxpayer number of corporation and individual, but info of income and tax payment amount are not required

※ (4) and (5) is the material to identify the individual

-

Federal and local tax

Federal tax

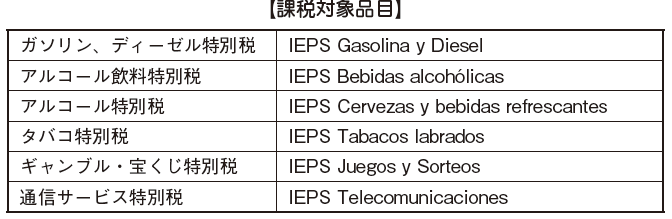

[Special tax of production service]

Special tax of production service , IEPS: Impuesto Especialde Productosy Servicei, is the tax of added value levied on specific items subjected to taxation as follow.

When importing / selling the above items, the transaction price is multiplied by the tax rate of each item and tax amount is calculated. Also, when importing only, Added the customs duty and customs fee to the price of the targeted item, then you will multiply the tax rate of each item by the tax rate to calculate the tax amount. The tax amount calculated in this way must be paid monthly.

■ Local tax

[Payroll tax]

Payroll tax is the tax imposed on the total salary of employees, and the tax rate of 2% is confirmed in a lot of federal states ; only rate of Mexico City was risen to 3% due to the reform of the tax system in 2014. However, depending on the state, you can be accepted of tax exemptions for a certain period after the start of business..

[Tax of real estate acquisition]

Real estate acquisition tax is imposed on those who acquired real estate regardless of methods such as acquisition, donation and inheritance Calculation of taxation standards and tax rates slightly different depends on the state, but a tax value of around 2% is a standard to the highest cost among the transaction price. the price of land register, and the assessment market price, In some states, there may be privileged treatment as investment incentive to exempt taxes in whole or in part.

[Tax of real estate possession]

Real estate tax for possession is imposed on the real estate you have. Since the method of calculating the evaluation value of the real estate is subject to taxation and the tax rate varies from municipality to town, village, individual confirmation you have to note this.

[Bed tax]

The tax of staying is the tax imposed on the accommodation fee when staying at a hotel. The tax rate is set to 2% in many states., Since there are different tax items ,we need to confirm it locally. -

Other

■ Other tax reform items

8% tax is imposed on fast food, and soft drinks containing sugars are subjected to the taxation that it costs you one peso per liter. Also food with high calorie more than 275 kcal per 100 grams for example chocolate, cacao, pudding and like this, it costs you 8% tax.. In addition, a new range and limit of taxation will be determined as to transaction such as a import and sale of fossil fuels and pesticide insecticides.

■ Mailbox settings

A mailbox of new taxpayer was set up due to the revision of the tax system, and all interactions with SAT are now performed through this mailbox. Please refer to the details in Chapter VI "Accounting" and later).

-

Latest News & Updates

* Summary of changes due to package of economic stimulus measures in 2016

The annual revenue was announced in the Official Telegram of November 18, 2015. As a result, some provisions of income tax law, Federal law of annual revenue, special tax law of production service will be revised, supplemented or abolished in 2016. The main changes are as follows.

1. Interest rate applied to extension of annual revenue and tax exemption will be maintained.

1.1 Tax rate for withholding tax on interest in 2016, withholding tax on interest is changed to 0.50% per annum (0.60% per year in the previous year).

1.2 Incentives

There are incentives for companies obliged to withhold income tax and added value tax from individuals providing specialized services. There is also an incentive to donate fundamental goods related to survival of human being’s life, such as food or health to the organizations accredited for donation tax deductions, which means they can additionally deduct the equivalent amount to 5% of sales assumed as the donation for the purpose of consumption.

2. Federal tax law

2.1 Execution of Electronic Audit

The tax authority's electronic reviewing launched by the revision of 2014, came into force. If the tax authority finds fraud and error, the documents will be sent to the taxpayer through tax mailbox.

2.2 Introduction of Tax Payment with lottery

Article 33-B as to tax payment with lottery was added to tax law as a method used in other countries to promote the responsibility of tax authorities in difficult taxation sectors. Tax payment with lottery is the content that gives prize money or prizes to taxpayers who made purchase subject to consumption by using electronic data.

2.3 Notice of transfer pricing information

Based on the provisions of Article 32-D of Section 4 by the revision of the same law the Federal administrative authorities: central government and national institute) and the federal prosecutor have agreements that you are prohibited to entry transactions lease contracts, and service contracts or public works contract with taxpayers submitting annual information and notice in regard with the transaction of parties concerned.

2.4 Information Exchange

32- Paragraph B of Article 32 was added to law in response to the international commitment of information exchange as countermeasures against tax evasion and tax avoidance such as agreement of common standards for report globally and automatically exchanging financial information,

* Amendment contents of Cabinet Order of IMMEX

On 6th January 2016, the Ministry of Economy announced the revised Cabinet Order on Official Journal of the Federal by Cabinet Order of IMMEX ; Cabinet Order for the Promotion of Maquiladora Service Industry for Export. The contents are as follows.

* Since 1st January, 2015, IMMEX companies can’t be accepted to take the custom bonds of IMMEX and now the bonded companies are accepted by SAT. Please take a look at the following sentences with this pre condition.

● About temporary import for sensitive items

Normally, many products can be bonded up to 18 months when they are temporarily imported by the IMMEX program, but the sensitive items were different in terms of their bonded periods. However, as a result of this amendment, the following items attached in files were abolished and the period of preservation and stock in the country of temporary imports was changed to determine as 18 months the same as the other items.

- File I of BIS attached by IMMEX Cabinet Order (sugar, syrup, etc.)

- File I of TER attached by IMMEX Cabinet Order (Steel materials of HS 72 type)

- File II attached by IMMEX Cabinet Order (Used Pneumatic Tire etc.)

- File III attached by INMEX Cabinet Order (textiles, fiber, threads and clothing etc.)

● Added sensitive items

In addition, all of the sensitive items separated from above Attachment I and II are all listed under the attached file II of IMMEX Cabinet Order. At the same time, the following products have been added to sensitive items. The term of preservation and stock is 18 month as well.

- Steel pipe of HS73 type

- Aluminum and its products

- Scrap and waste

- Tobacco products

● Term of temporary import during virtual operation

As a trade regulation and standard refers that you should not temporarily import stuffs with yourself but use a virtual operations of the IMMEX companies, a trade will be regarded as just export on a document procedure but as indirect exporter, you can temporarily transfer the processed products to the last exporter or other indirect exporters. The term of preservation and stock would be six months.

We mentioned above the period of preservation and stock is 18 months: if your company is approved one, 36 months are given , but you can only stock the partial materials of transported product by virtual operation for six months.

● Start for Verification of Execution of Guarantee Money System

It was stated that the Ministry of Finance would consider to introduce the guarantee money system. This system has the content that guarantees the dutiful performance for temporary import of sensitive items. Also, this has not been announced yet in details but in the future it’s considerable that the revision of relevant bylaws will be advanced for introducing the system.

● Addition of Cancellation

It was added to the matter of cancelation to IMMEX Cabinet Order if you export the temporal imported item to another IMMEX companies with virtual export, conduct sub maquialla operation; subcontracting manufacture to non IMMEX companies, or the temporary imported item is not accepted to transport physically.

● Deletion of the paragraph about exemption of obligation to register importers of each department

Currently, it is described that according to Trade regulations and standards of SAT, in the field such as textile products and footwear importers must be registered by their department depending on the partial material, however this obligation is going to be abolished. Likewise IMMEX company also doesn’t have to do, thus the paragraph corresponding to this matter of IMMEX Cabinet Order was deleted.

● Deadline for the period of IVA refund

With regard to the regulations concerning the benefits of speeding up IVA (Value Added Tax) application process for enterprises registered in IMMEX program, it had been described that IVA refund will be done within 20 business days or within 5 business days if they become a certified company, this paragraph has been deleted for now.

This is applied to companies with certification as “IVA” and “IEPS” meaning Special Tax for Production and Service in English approved by SAT called as Certificación en materia de IVA e IEPS in Spanish by the determined rule. Even during IVA return the companies concerned must comply with each provisions of “Ley del Impuesto al Valor Agregado”, “Ley del Impuesto Especial sobre Producción y Servicios” executed since 2014, and Reglas Generales de Comercio Exterior announced by SAT by the modality of the registered company registration like "A", "AA" or "AAA" Granted 20 business days as a duration of deadline to the company certificated as A, 15 business days to AA, and 10 business days for AAA, they have to be subject this regulation.

-

-

-

International tax

Each country in the world, has established a tax system by international transactions. This tax system is established by each country to protect the taxation right of their own country and international double taxation arise international transactions are operated in according to the tax system of each country. For this reason, tax treaties have been executed between the two countries in order to avoid this double taxation and international taxation problems. Taxes related to such international transactions are collectively referred to as "international taxes".

The necessary reasons of "international tax" are generously as the following two sentences.

① Elimination of double taxation between international

② Guarantee of taxation right in each country (prevention of tax avoidance act)

Below we will show you the individual tax provisions in the international tax.

-

Foreign tax credit

Tax is imposed on mobility or consumption (hereinafter referred to as "mobility" etc.) of the management resources of human, goods and money. Likewise, for transactions between international organizations, if you transfer management resources between international companies, taxes will also arise internationally, which will result in the relationship of international taxation.

The problem here is that the tax imposed on the transfer of management resources among the international transaction is levied based on each country's own idea (tax law). In other words, there is the possibility that taxes are imposed on two countries each others, in the same transaction, due to differences in their views on taxes of each country. In order to avoid such double taxation, the provision of "foreign tax credit" is stipulated in each country's tax law. Foreign tax credit is a system established to adjust the double taxation of international income by deducting the amount of tax paid for income incurred overseas from the tax amount of the residential country. Foreign tax amounts levied in this case are, for example, foreign corporation taxes paid by representative offices, royalties with interested parties, interest income received, income tax withheld at the time of payment such as dividends and so on. Since these are double taxation between the country of residence and the country of tax withholding at the source of income, it is necessary that you need to fix the tax amount incurred in the country of tax withholding at the source by the tax declaration of the country of residence. If Mexico is double-taxed in the country of residence, we will have to update the tax amount of the double items as the corporate income tax amount that you shall pay to Mexico, according to the provision of foreign tax credit. -

Insufficient taxation system

In 2005 Mexico also uses an insufficient taxation system into her country. This objective is to reduce tax burden by taking interests incurred from the liability as expense including in the amount of deductibility by summing the among of capital as debt. The tax system to restrict the act is the insuffIcient taxation system.

For example, if the total debt to overseas clients exceeds three times as much as the net asset value, you can regard the interest expense corresponding to the amount exceeding the amount concerned as the non-deductible amount. However, in the following cases, the insufficient capital tax system will not be applied.

· In case you bear debt relating to construction, operation and maintenance of strategic development of infrastructure

· In case of financial institution

· In case there was agreement of the tax amount with SAT in advance

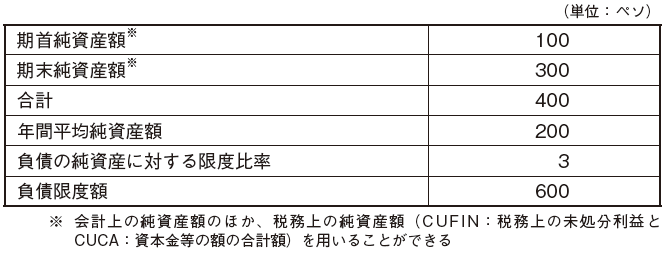

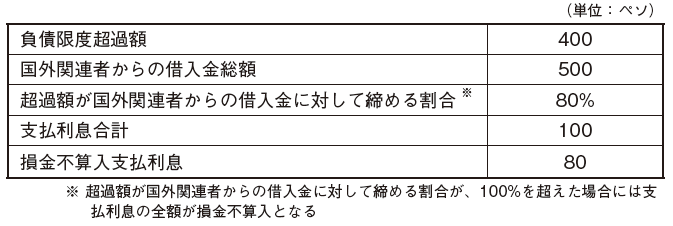

■ Calculation example of non-deductible amount due to insufficient capital tax system

The calculation method of the deductible amount is as follows in the case a total debt toward the company concerned outside Japan applied under insufficient capital taxation system exceeds three times as much as the net asset amount

[Determination of liability column]

you can use not only the net asset of accounting but also CUFIN and CUCA of the taxation)

[Calculation of non-deductible amount]

Debt amount 1,000 pesos, borrowed amount from the companies concerned overseas 500 pesos, and total interest expense is 100 pesos

-

PE Taxation

Normally, when conducting business activities by establishing permanent establishment (PE: Permanent Establishment) abroad, taxation obligation will arise in the local country. In other words, it is the principle of international taxation that tax obligation in local country does not arise unless there is PE in the local country. Regarding the range of this PE, it is generally exampled by domestic laws. tax treaties and others in each country. However, even if you do not have PE legally and it is deemed that income arises in a local country as a matter of fact, the local country also imposes taxation right onto nonresidents. Without absence of tax payers, tax incurred on income of the local country is called “PE taxation”. However, because taxpayers file tax returns in the situation of no income, if PE tax is imposed, you will face a problem of double taxation. The range of this PE is not concrete and clearly stipulated, based on the judgment of each country’s tax authority. Therefore, in the worst case, despite your local company is levied as PE tax , in Japan this tax is not accredited as PE and it’s considerable that you can’t adjust this for the double taxation.

■ Examples of PE taxation

[case 1]

In the performance of a dispatching personnel from Japan to the local country based on business contracts between Japan and the local country with exceeding over the certain period, it is certified in the presence of PE from the tax authorities It is subject to taxation. Tax authority certificate that there is PE tax obligation in your company and you are subject to pay it.

[Case 2]

In the case of activity in the established representative office with certification of PE (branch of a foreign corporation) that conducts business activities although forbidden in the ordinary situation, taxation deemed as a profit must be executed

[Case 3]

In cases where a Japanese corporation has such companies concerned as a subsidiary abroad and also the task of subsidiary.should be performed by the parent company (e.g. an approval of contract under the parent company name), Taxation will be done locally as the company under Japanese parent company (ie, the company possessing a branch office) rather than an independent entity.

Regarding the definition of PE is determined by not only domestic tax laws of each country but also tax treaties concluded between Japan and Mexico and regards management office, branches, and others and furthermore the following facilities

· Factory and Field

· Farm, plantation, mine, well of petroleum or natural gas, quarry and etc.

· In the case that a construction term to build site, architecture or installation will exceed over six months.

However, if these bases mentioned above are operated by agreement between the governments of the two countries concerning with economic or technical assistance, they are not treated as "PE; permanent establishment".

-

Tax Treaty

Tax treaty is agreement (treaty) between different nations by means of statements that are entered with the aim of eliminating double taxation and prevention of tax evasion. As this treaty becomes an agreement between two nations, it will be applied by proceeding the domestic law established each country. In other words, while tax is levied rightly in your domestic law, it can be "tax free" in the case it is said to be "tax free" by the tax treaty. However, by applying tax treaty, if taxation is disadvantageous for you, reflecting on your domestic law, you can apply the provision of domestic law . This is called "Preservation Close"

.png)

The tax treaty between Mexico and Japan was promulgated in 1996. Even in various other treaties except tax treaty, we may separately considerate the treatment of specific tax items the nation concerned toward Japan that your Japanese clients live..

Nations entering in tax treaty with Mexico

Nations entering in tax treaty with Mexico -

Transfer Pricing Taxation

Transfer pricing taxation is a taxation system established to prevent the transfer of profits from overseas through transaction prices in transactions between the corporations concerned. A company sets a transaction price (transfer price) such as a trade of assets, a providing services, and others. toward your companies concerned overseas by offering service with a different price from the companies of the third party , you can freely conduct the mobility of interests in other nations.

.png)

■ The corporation concerned out of Mexico applied for transfer pricing taxation

overseas corporations related to which transfer pricing taxation is applied in Mexico, are as follows.

· Companies with managing and administrating directly or indirectly (or being managed and administrated)

· Companies with having share relationships each others directly or indirectly

In Mexico, due to provisions about overseas corporations concerned, there is no description in regard with the shareholding rate, therefore even though the shareholding rate is low you have to be aware that it may be focused on corporation for transfer pricing taxation.

■ How to calculate price between independent corporations

In Mexico the calculation method of ALP (Arm'sLengthPrice) is based on the guidelines of transfer price by OECD, however it is different from the way of OECD and Japan because it is adopted by its own original system. The specific calculation method is as follow. Also, although it follows OECD’s guidelines, it is not adopted with the best method rule, thus so-called traditional three methods(Independent Price Comparable Resale Price, and Cost Price Method) are applied as priority at present.

[Comparable Uncontrolled Price Method]

Comparable Uncontrolled Price Method (CUP: Comparable Uncontrolled Price Method) is a method to make the equivalent amount of consideration for transactions conducted between non-related parties under similar conditions of the foreign transactions concerned as ALP of connecting foreign transaction. If the transaction to be compared is an item or the like, the transaction condition may change due to the influence of business strategy, market conditions, etc., and it may be difficult to guarantee comparability. In addition, higher identity is required as compared with other ALP calculations. For this reason, this method is often used for interest rate transactions with low fluctuations in terms of transactions and for products with quotes, and it is not widely adopted for ordinary goods transactions.

[Resale Price Price Standard Method]

The resale price method (RP method: ResalePriceMethod) is a method of making the amount obtained by deducting the amount of profits that would normally be obtained from the transaction from the resale price to a third party as ALP of overseas related transactions.

This method is often used when overseas related transactions are import transactions (in the case of import transactions, data to be compared can often be obtained from public data). Also, for comparative purposes, strict similarity is not required as much as the stand-alone price quasi method.

[Cost Plus Method]

CP method: Cost Plus method is a calculation method as ALP to add the amount obtained normally obtained from the transaction to the amount of costs incurred by the foreign connecting transaction.

.png)